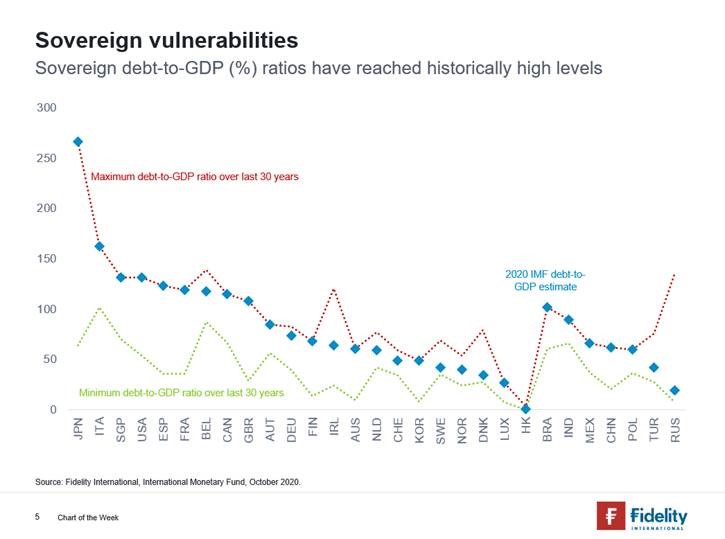

Arguably, what is more important for governments is their ability to repay the debt that is being accumulated due to the current crisis. Unconventional monetary policies, like yield curve control and quantitative easing, is assisting governments by keeping bond yields low. The hope is that these policies will assist in reducing the debt-to-GDP ratio over time, as nominal interest rates are kept constantly below nominal rates of growth in GDP. Whilst this appears the most likely scenario in the immediate future, the key question for central bankers will come should inflation begin to materially rise, testing the willingness of central banks to maintain ultra-easy monetary policy. If central banks around the world fail to act in while inflation moves higher - which would also assist in alleviating debt loads - it may be the formal end of the central bank independence era.