After this week’s fall through parity with the US dollar, policymakers in the eurozone will not easily recover market confidence in the single currency.

At a difficult moment for so many globally, spare a thought this week for European Central Bank (ECB) policymakers facing an almost impossible dilemma on behalf of the eurozone’s consumers.

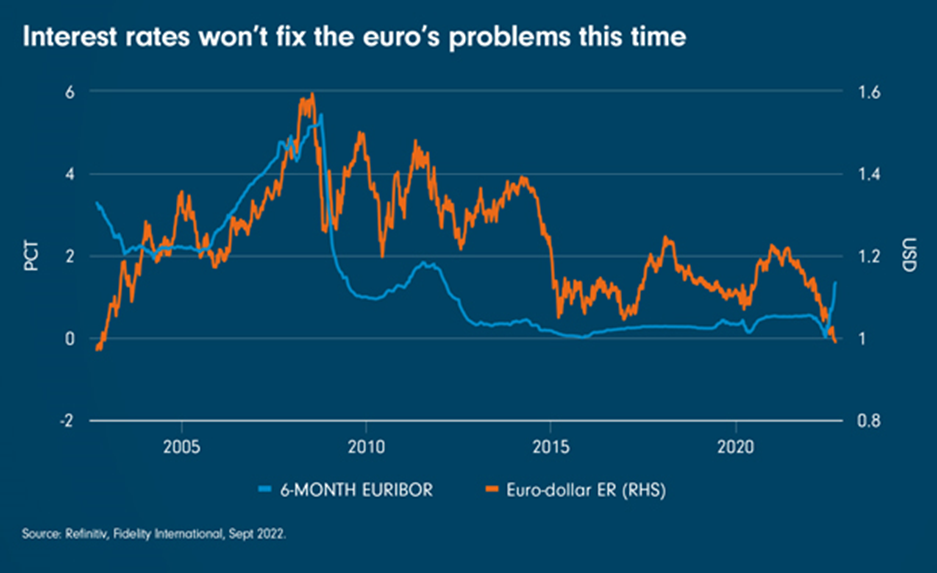

Our chart this week shows the euro sinking below parity with the US dollar to fall to its lowest level since the early days of the single currency, while also emphasising that, so far, rises in market interest rates have done nothing to halt the slide. Falls in the currency of course only add to the eurozone’s inflation problems and for some in the market only make the case for the bank moving ahead aggressively with more hikes.

Yet as the Euribor pricing in the chart also shows, expectations for more tightening are now heavily priced in - and the currency is still no stronger. As a bond investor watching currency markets from the side-lines, the risk may be that the more the ECB hikes, the deeper the eurozone will fall into recession, and the more that will weaken the euro and worsen the position of those buying goods in dollars.

In the past Germany’s export gains from a weaker euro might have been the solution to this vicious circle, but the gas and power dynamics at play make a weaker exchange rate just as painful this time for Berlin. As so often, it may come down to centralised action to be backed or funded by the eurozone’s more solvent governments.

The ECB has in the past held fire in the face of supply side spikes in inflation. This may suggest that they want to pull interest rates out of negative territory after a decade of emergencies, but once they have done this, they may face a situation that is really out of their hands. The Federal Reserve’s own rises in rates are neutering any impact on the euro.

A big miss on inflation numbers in the US could change this calculus somewhat, spurring the market to start to price in the end of the US tightening cycle. However, European policymakers may well spend the next few days watching the first steps taken by new UK Prime Minister Liz Truss to see what impact her opening gambits have. Her plan to cap energy prices though has been costed at more than £100 billion, and similar steps may be out of reach for the eurozone’s more heavily indebted governments. Yet solving the gas problem now looks more crucial to saving the economy, and to halting the fall of the euro, than any rate hike.