At the turn of the year, we ask our analysts how companies see the year ahead, and how they are positioning their businesses for what they think is coming. Our Analyst Survey is a barometer of executives’ plans and their fears; of companies’ resilience and their growth ambitions; and of trends that position certain sectors at an advantage over others. How do our analysts report CEOs are feeling this time around?

Analyst sentiment rises to new highs

With contributions from Michael Sayers, director of research, equity and Marty Dropkin, head of research, fixed income.

Company executives are optimistic about the future. According to Fidelity’s 2018 analyst survey, they are, in fact, even more optimistic than they were at the start of last year.

Source: Fidelity Analyst Survey 2018

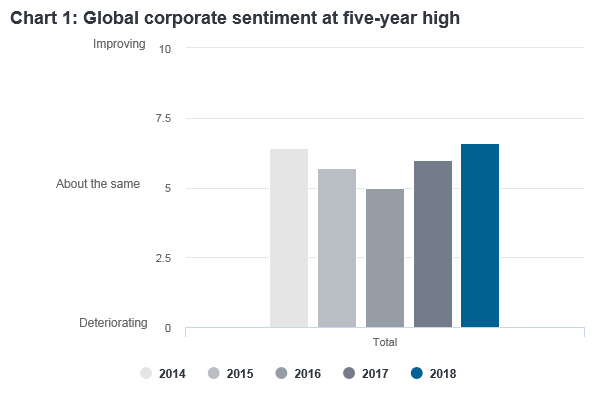

Our global sentiment indicator, an aggregate measure of corporate confidence through the eyes of our analysts, has risen to the highest level in five years. It is now well into ‘warming’ territory, where more analysts are positive than negative about expected conditions for the next 12 months.

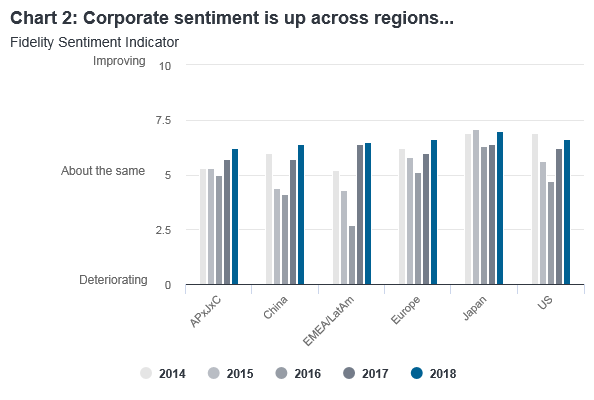

This confidence is strikingly uniform across sectors and regions, and stronger than last year everywhere except in technology (where confidence levels were already extraordinarily high).

Fidelity Analyst Survey, February 2018

Source: Fidelity Analyst Survey 2018.

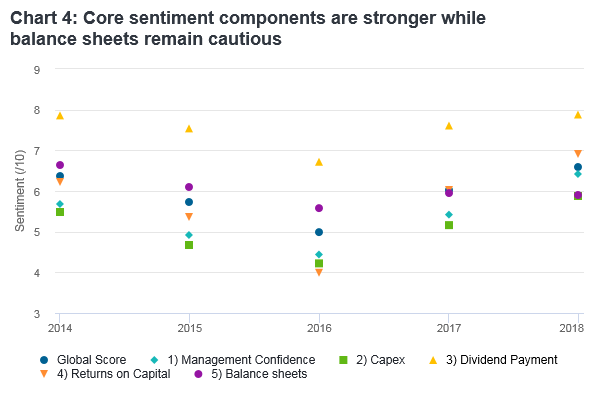

Executives see benign conditions ahead, and are planning accordingly. More than in previous years, they have faith in growing demand, while maintaining their focus on cost-cutting. In a major turnaround from previous years, they are investing in their own productive capital again. They are spending on technology to innovate and compete, and tentatively raising wages.

They are keen to use rising returns on capital to reward shareholders with larger dividends and more share buy-backs, and are keeping an eye out for more M&A opportunities. They are confident their balance sheets are sound not just because of cost savings and careful spending, but because many took advantage of the bond market’s bull run to refinance debt at lower rates and extended maturities.

Source: Fidelity Analyst Survey 2018

A newfound moral compass

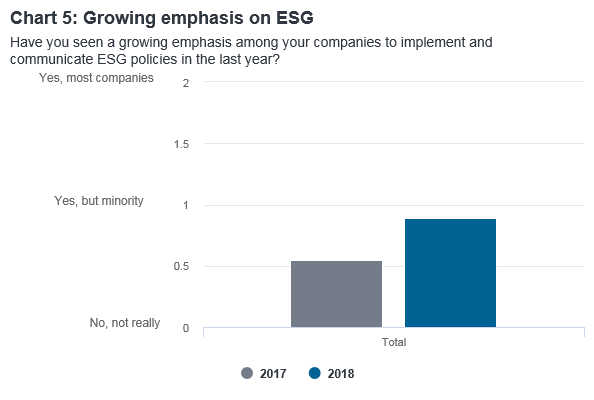

And they are listening. Whether or not this is peak-cycle behaviour in the relative comfort of low financial stress is impossible to judge at this stage, but it is clear companies are no longer ignoring investor concerns about social, environmental and governance standards.

Many analysts still say it’s only a minority of companies which are focusing on this, but the trend is undeniable. Once the preserve of wealthy markets in Northern Europe, ESG considerations are finding their way onto boardroom agendas in all regions.

Source: Fidelity Analyst Survey 2018

Few warning signals

Overall, the survey gives little reason to expect an imminent end to these near-perfect conditions, and certainly does not appear to raise any immediate red flags.

Company executives are not all that worried about geopolitical risks, do not expect a ‘hard landing’ in Chinese economic growth, and expect a modest boost from US President Donald Trump’s economic policies. Beyond technological disruption there is little that appears to keep them awake at night (and they are increasing technology budgets to keep up with the competition and position for such threats).

Neither is inflation a cause for concern. Excessive cost, wage or output price inflation alongside rising funding costs could trigger tighter monetary policy conditions, limiting real demand growth and forcing companies to cut their investment and spending plans. But while our analysts report moderate increases in input cost and wage inflation and a little more pricing power among their companies, they firmly expect output price inflation to remain at, or below, consumer price inflation.

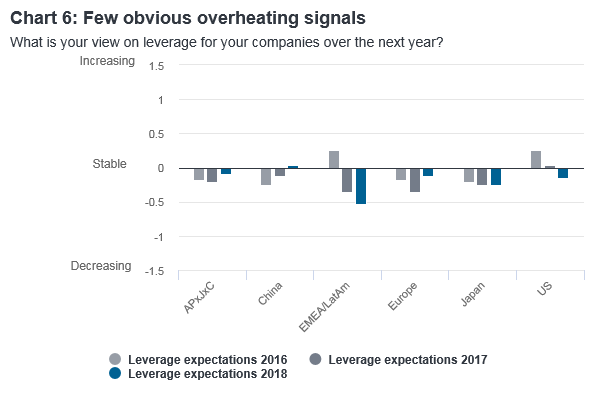

Confidence with caution

At this stage of the cycle, leverage typically starts to rise as confidence turns to hubris. Moreover, total global debt (including private and government debt) has soared to record highs well above pre-crisis levels, leaving all major economies more vulnerable to increasing interest rates than ever before.

It wouldn’t have been surprising, therefore, to see leverage and default expectations creeping up, and balance sheets weakening. Yet our data do not show this. On the contrary, our survey points to well-funded balance sheets across sectors; stable financing needs, funding costs, and default rates; and slightly falling leverage over the next 12 months - a reflection of cautious capital use despite years of economic growth.

There may be some froth in shareholder-friendly activity, which tends to rise late in the cycle despite best-value deals being more likely when share prices are cheap. Cash repatriated to the US under new legislation is mostly expected to go towards share buy-backs. Where leverage is seen to be rising (only among 20% of analysts), it is attributed to share buybacks, M&A, and dividend payments, as well as higher capital spending. Almost no one ascribes growing leverage to expected cash flow deterioration.

Source: Fidelity Analyst Survey 2018

Can it last?

The combination of record-high corporate margins, ultra-cheap funding, strong wage constraint, supportive commodity prices, and synchronised global economic growth is unusual, to say the least. Can this balmy corporate climate continue?

Extending debt maturities further will be harder, interest rates and yields are now rising from their lows, and corporate margins can almost only go down. Funding costs in China are expected to rise, but growth is not seen slowing significantly; whether China manages to walk this tightrope remains to be seen. Few companies anywhere are planning for geopolitical risk, despite rising tensions across the world, from Venezuela to the Middle East and the Korean peninsula.

Next year, our survey may no longer look so rosy. But for the results of the latest survey, companies remain highly confident, and they’re proceeding accordingly. This may be as good as it gets.

About the Fidelity Analyst Survey

At the turn of the year, we ask our analysts how companies see the year ahead, and how they are positioning their businesses for what they think is coming. This year, we received 162 responses from our 143 analysts (some cover more than one sector). Such granular information is rare and valuable; our analysts conduct more than 16,000 individual company meetings per year and can detect shifting perspectives long before they emerge in official data.

Do CEOs, CFOs and COOs have a spring in their step? Are they excited about new investments, new markets, new products, or new technologies? Can they find the people they need? Can they obtain the funding to grow? Can they reward shareholders and please their creditors? Or are they struggling to meet payments, invest in innovation, and maintain dividends, or diverting budgets to deal with macro-economic risks and geopolitical threats? Do they fret over rising costs, or do they have enough pricing power to pass them on and protect their margins?

Our analyst survey is a barometer of executives’ plans and their fears; of companies’ resilience and their growth ambitions; and of trends that position certain sectors at an advantage over others.

Its track record seems to prove its worth. Two years ago, our survey revealed a precarious outlook following the rapid decline in the oil price. We noted that the data did not point to a global recession, but that threats and opportunities were finely balanced. Indeed, the global economy only returned to a firmer growth track in the second half of the year, when the oil price had recovered convincingly and the pressure on energy and materials firms started to ease.

By last year, corporate confidence had rebounded, buoyed by the energy sector’s improved fortunes, China’s fiscal stimulus and tech’s rapid conquests. The media’s frenzied reporting notwithstanding, executives appeared little perturbed by political shifts, quietly positioning for recovering demand and new opportunities. Corporate earnings duly surprised on the upside, stock markets repeatedly made new highs and credit spreads contracted globally as investors scrambled to adjust their outlook.