At the turn of the year, we ask our analysts how companies see the year ahead, and how they are positioning their businesses for what they think is coming. Our sector insights provide a deeper dive into the views of our global analyst team on: healthcare, materials, industrials, information technology, utilities, financials, energy, telecoms, consumer discretionary and consumer staples.

Chapters as follows:

- Healthcare

- Materials

- Industrials

- Information Technology

- Utilities

- Financials

- Energy

- Telecoms

- Consumer Discretionary

- Consumer Staples

All sectors

Confidence is strikingly uniform across sectors and regions, and stronger than last year everywhere except in technology (where confidence levels were already extraordinarily high).

Source: Fidelity Analyst Survey 2018

Healthcare

Sentiment indicator 6.1 vs 5.8 last year

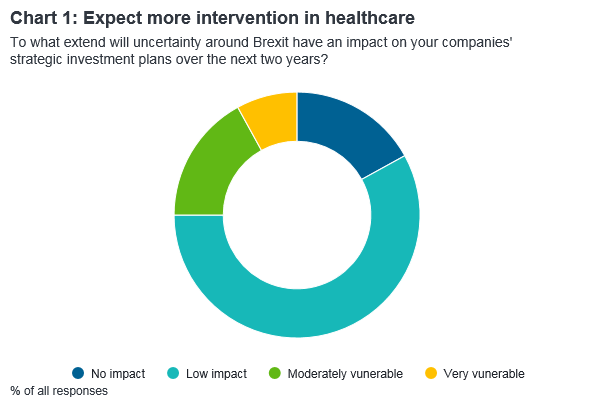

While the overall economic environment has improved, our healthcare analysts’ mood hasn’t lifted as much as some of the other sectors. Despite the sentiment indicator marginally improving to 6.1, healthcare has slipped into the bottom three sectors. One reason is that sentiment in previous years had been strong so the potential for further improvement was smaller. But there are others factors at play, too: regulation and pricing.

Continuing pressure from regulatory intervention and drug price controls is showing up in the survey with 75 per cent of our healthcare analysts expecting more regulation in some form. A full 83 per cent believe their companies’ profits are vulnerable to EU political uncertainty, in particular, and 42 per cent think geopolitics could have a moderately negative impact on strategic investment plans (more than in other sectors except energy). Inflation is also a concern, with 83 per cent of healthcare analysts thinking higher inflation will depress margins, pointing to less pricing power than elsewhere.

Source: Fidelity Analyst Survey 2018

Overheard in Healthcare

- "The drug supply chain is under threat from more regulation. Any changes would act to reduce profits."

- "The risks and opportunities vary from company to company - some benefits from US tax reform, some don't - but the overriding concern is over drug prices."

- "The US is the biggest end-market for medical devices. Most of my companies sell globally and do significant FX hedging so FX changes don't really alter business decisions."

- "This is greater government spending in social and health care programmes in Europe."

Materials

Sentiment indicator 6.7 vs 6.4 last year

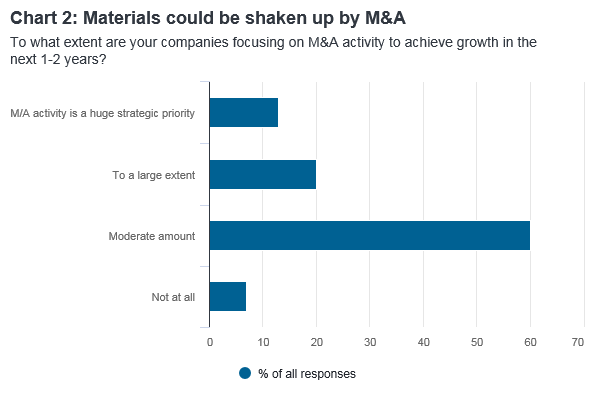

Materials have sprung into life. It’s got the fourth-highest sentiment indicator and analysts are expecting more activity in the form of M&A. A third of our materials analysts believe M&A is a focus to ‘a large extent’ or a ‘huge strategic priority’. This activity is more likely to be in the form of a major strategic move and/or into new markets, rather than bolt-on acquisitions – the opposite of the picture across the board. Although a quarter say balance sheets are stretched, this year fewer say they’re excessively stretched than last year, and more analysts see leverage falling than rising.

Materials analysts naturally focus on China given its role in demand and steel, aluminium and coal production. So when 40 per cent expect a China deceleration, and 27 per cent a China hard landing, it’s worth taking note - this could be one of the biggest risks in.

Source: Fidelity Analyst Survey 2018

Overheard in Materials

- "There is a focus on M&A as organic growth opportunities decrease. And there is a focus on cost cutting to achieve margin improvements as opportunities to raise prices or operating leverage fall."

- "Increased environmental regulations and capacity reduction are both positive for margins."

- "US President Donald Trump initially raised the potential for a US infrastructure boom, but in the end hasn't proposed anything that would materially benefit materials demand on a global scale."

- "The production process (mining technology) is changing completely and will involve more automation."

Hear from Nitesh Kathuria, director of research for equities on how balance sheets have improved in the metals and mining sector and how this may change their spending plans.

Industrials

Sentiment indicator 6.6 vs 6.2 last year

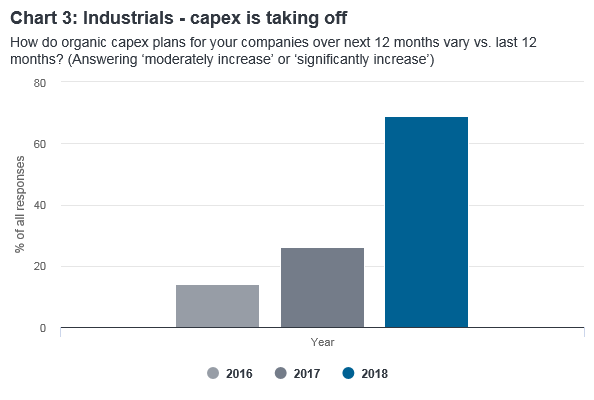

Industrials are a wide and diverse group of companies but most analysts agree that automation will be a major influence on the sector. This is showing up in capital expenditures with 69 per cent of sector analysts expecting capex moderately or significantly to increase in the next 12 months. About half of our analysts think there will be a growing focus on growth capex compared to last year.

Automation is having a transformative impact and demand growth remains supportive. Last year materials analysts told us CEOs saw earnings growth coming from market expansion and end-demand growth, and this year almost three quarters say increasing returns will be caused by higher/faster end demand growth.

Source: Fidelity Analyst Survey 2018

Overheard in Industrials

- "Auto companies are trying to launch new models to ensure they suffer less volume decline as the global auto cycle rolls over. They are investing aggressively in capex to ready themselves for an electric vehicle/ autonomous world."

- "Chinese fiscal stimulus in the form of subsidies (R&D subsidies, cheap financing, etc.) as well as more incentives for localisation etc. is what drives the industrial automation sector in China."

- "More capex will be needed to invest in electric vehicles as regulators are pushing markets towards EV adoption".

- "NAFTA negotiations are delaying investment decisions in Mexico. And presidential elections in Mexico, Brazil and South Africa are all delaying important long-term decisions."

Information Technology

Sentiment indicator 7.1 vs 7.3 last year

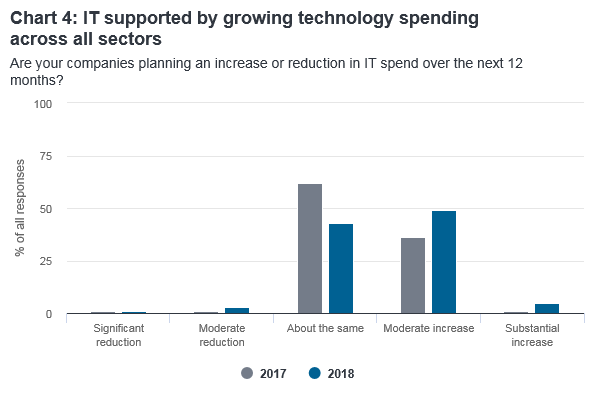

After soaring last year, the sentiment indicator for information technology more or less stabilised this year at a high 7.1 - firmly into territory where corporate conditions are improving. None expect returns on capital to deteriorate over 2018 compared to 2017, and 84 per cent say management teams are considered ‘more’ or ‘a lot more confident’ than last year. Headcount is expected to rise by at least 60 per cent in the next year according to two thirds of analysts. With other sectors growing in confidence, technology spending is forecast to rise across the board, providing a strong boost to the IT sector this year.

So why is the sentiment indicator slightly down on last year? The dividend score is the main contributor. Last year 60 per cent of analysts in the sector predicted dividends to rise further while this year that has fallen to 42 per cent. Also, half of IT analysts said balance sheets were ‘very safe and cautious ‘in 2017, which dropped to a quarter this year. However, overly safe balance sheets might imply excessive cash holdings; the increase in hiring, technology spending, and capex that analysts expect for this year, along with the strong tilt towards growth capex, bode well for future growth.

Source: Fidelity Analyst Survey 2018

Overheard in Information Technology

- "Enterprise software companies benefit from more regulation, which helps them sell more compliance/ security software, e.g. the EU's General Data Protection Regulation."

- "US tax and repatriation policy changes are positive but regulation would be negative. On balance these factors may cancel each other out."

- "China is being more active in investing in IT assets - particularly trying to buy up expertise in semiconductors. This is a strategic initiative for them."

- "Protectionism remains a risk, although there are limited tangible signs of it so far."

Utilities

Sentiment indicator 5.8 vs 5.5 last year

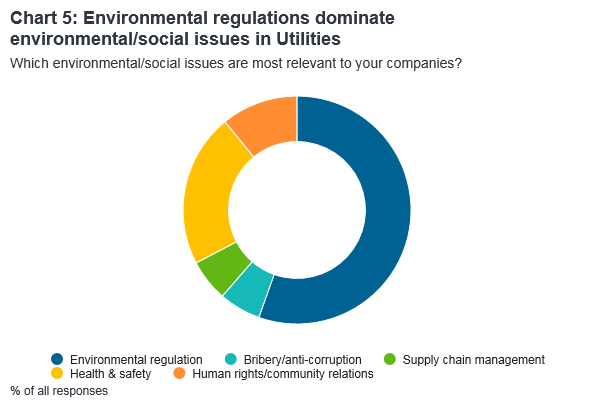

Utilities are undergoing major change and it’s going to cost them. Environmental regulations are a key feature; more than half of our utilities analysts point to it as the most relevant environmental or social issue. And that has implications for investment. Significantly more analysts (four in ten) than elsewhere think the majority of companies in their sector will need to raise capital, and that leverage will increase this year, partly due to rising capital spending .

This could hurt returns. Thirty per cent of analysts think return on capital could decline over the next year - joint highest of all sectors along with consumer discretionary. Unsurprisingly, they mostly ascribe this to higher costs. If inflation picks up, it could heap more pressure on utilities given 70 per cent of analysts think it will mostly depress margins. On the plus side, fiscal stimulus could have a moderately positive effect on the sector according to half of utilities analysts.

Source: Fidelity Analyst Survey 2018

Overheard in Utilities

- "I expect stricter environmental regulations which could require more capex and investment. On the downside, more environmental regulations can lead to more stranded assets, particularly coal and nuclear power plants."

- "I expect more investment in growth areas such as renewables, retail and e-services, network expansion and upgrades, electric vehicle infrastructure."

- "US utilities will benefit from greater infrastructure spending and corporate tax cuts, particularly for unregulated power companies."

- "US Presidential Donald Trump's stand on renewable energy makes European companies more competitive and attractive as renewable investments."

Financials

Sentiment indicator 6.5 vs 5.8 last year

Banks are largely rehabilitated from the over-leveraged and overly exposed days of the credit crisis. The sentiment indicator has jumped by an impressive 0.7 since last year on the back of expectations of higher dividends and better returns. Three fifths of our analysts expect dividend payouts to increase, and almost as many say that returns on capital will improve, mostly driven by cost reductions.

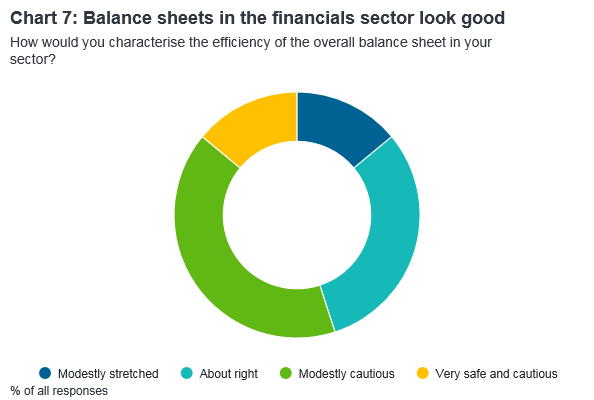

Balance sheets are looking healthy as well with over half the respondents reporting that they are modestly or very cautiously placed. But companies will need this buffer to adapt to a rapidly digitalising world; a whopping 82 per cent of financials analysts say IT spending will increase further this year in an attempt to keep up with innovation and bolster data security and cyber protection.

Source: Fidelity Analyst Survey 2018

Overheard in Financials

- "Financials companies are strengthening of balance sheets, selling assets and returning cash, focussing more on generating growth internally."

- "Higher spending through income tax cuts for subprime lenders, corporate tax cuts and repatriation should help investment banks via M&A."

- "No significant changes in regulation expected but refinement of existing capital rules likely."

- "Cryptocurrencies, cyber-crime, greater move towards doing business online are all going to affect the way that financials can do their business."

Energy

Sentiment indicator 7.1 vs 6.4 last year

The turnaround in confidence in energy over the last two years is dramatic. Higher oil prices have helped but they’re still a long way off their peak; the sector’s fortunes owe just as much to its strict discipline in cost management and oil production (both in US shale and OPEC).

Our analysts think average 2018 oil prices will only be a little higher than in 2017 but expect that discipline to continue, while oil demand will remain firm unless the global economy unexpectedly tips into recession. Cash flows are strong and management incentives are less geared towards boosting production than in the past five years, so analysts expect companies to continue buying back shares, raising dividends, paying down debt and cutting leverage in 2018.

.png)

Source: Fidelity Analyst Survey 2018

Overheard in Energy

- "Geopolitical risks don't matter so much when the market is oversupplied, but they do now. We are keeping a close eye on what's happening in Venezuela, Libya, Nigeria and the Middle East, for example."

- "My companies are looking to reduce costs to maintain growth late in the cycle."

- "Energy companies are highly capital intensive, and require regulatory stability to make longer-term investments in future production. Geopolitical risk inhibits this."

- "The risks? Shorter term, a global recession. Medium term, greater penetration of electric vehicles in transport sector destroying oil demand."

Hear from Randy Cutler, credit analyst for energy on how these companies are becoming more disciplined in how the plan for their spending and use their cashflows.

Telecoms

Sentiment indicator 6.4 vs 5.7 last year

Telecommunications companies are benefiting from easing regulatory headwinds in Europe and have taken advantage of cheap funding to bring down debt servicing costs. Although a third of analysts - more than in any other sector except energy - still see them as moderately stretched, balance sheets are now in a better state than in the past four or five years.

Dividend payouts, which act as a good barometer for the health of the sector, are expected to increase this year. Cost cutting opportunities in the form of ‘digitisation’ remain significant and make more major M&A deals likely, which our analysts regard as welcome because of the market’s highly competitive nature with fixed-cost businesses.

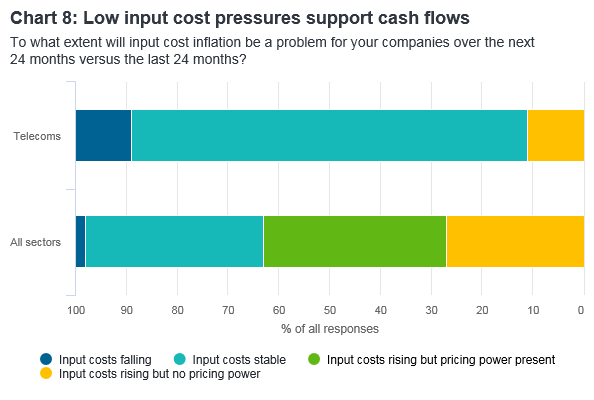

They also see some signs of price repair as companies are tentatively raising prices, but pricing power remains lower than elsewhere and the sector is the only one where a (significant) majority of analysts expect output prices to increase by less than inflation. Lower input cost and wage inflation than elsewhere, however, should help.

Source: Fidelity Analyst Survey 2018

Overheard in Telecoms

- "Major US telecoms companies have very high capital expenditures (AT&T spends the most capex in the US) and high cash rates with relatively low leverage (below the 30% hurdles being talked about)."

- "What could be very disruptive is the convergence of wireless and wireline technologies enabled by 5G wireless broadband - a singular broadband market could emerge (constituting mobile + traditional fixed-line services) over the next 5-10 years."

- "We'll see some differentiation in 'go to market' (paid prioritisation) but the impact from the repeal of net neutrality is likely to be limited."

Hear from Mike Ashford and Alex Grant, equity analysts, on how telecommunications companies are becoming more efficient; and why market structure is key.

Consumer Discretionary

Sentiment indicator 5.8 vs 5.1 last year

Sentiment in consumer discretionary has recovered from its precarious score last year, when positive responses barely outweighed negative ones, but this sector is one of extremes. The consumer isn’t necessarily suffering overall yet conditions remain tough in parts of the sector and leverage is high among US companies.

Businesses that are exposed to the growing taste for gaming, leisure and ‘experience’ spending are seeing growth, but traditional retailers in food and clothing are struggling under a combination of thin margins, fierce competition, excess store capacity and structural channel shifts to various forms of online shopping. With little market volume growth they have to eat into each other’s shares to survive - a brutal environment.

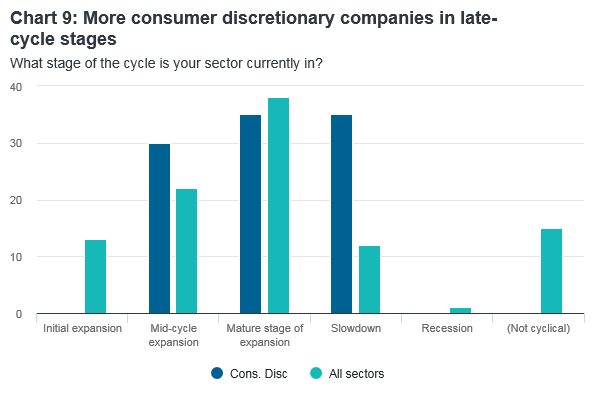

Analysts also say consumer discretionary companies are in more mature stages of their industry cycle than other companies and half say companies are now preparing for the end of the cycle. Almost a third - matched only by utilities - see declining capital returns and blame this on disruption, new entrants and slowing demand.

Source: Fidelity Analyst Survey 2018

Overheard in Consumer Discretionary

- "There are a whole lot of people in tech who are eating consumer discretionary firms' lunch."

- "Lot's of companies in the US are struggling with rising wage and freight cost inflation, and dollar weaknesses is a headwind for Asian companies."

- "Dollar sourcing costs will continue to hit margins for UK retail as hedges have mostly rolled off now; euro retailers are less impacted."

- "Tensions in the Middle East, Korea, Turkey and Europe (particularly terrorism) are a geopolitical risk."

Hear from Crispin Royle-Davies on how consumer discretionary companies are changing where they invest as customer behaviour changes.

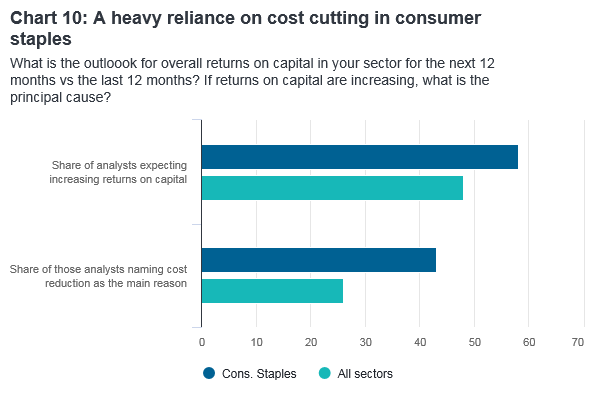

Consumer Staples

Sentiment indicator 7.1 vs 5.8 last year

Confidence among consumer staples analysts is firmer than among their discretionary counterparts, partly because of higher profit margins, razor-sharp cost control and better pricing power, particularly among the big brands. Staples companies also benefit from structural growth in demand in emerging markets; this gives European companies an advantage over US ones, which have less exposure to newer markets.

But their singular focus on cost control and ‘zero-based budgeting’, which now pervades the industry, may damage brands’ perception in the longer term; this is the trade-off between growth and margin. And analysts add that especially in developed markets, staples companies are experiencing real volume challenges; younger consumers prefer local, authentic, or organic products over big brands. This is putting pressure on margins but so far, companies have been able to raise pricing, leaving sales relatively stable.

Leverage is high but half of analysts see it falling over 2018, as it is mostly M&A-driven and fewer large deals are expected. Debt servicing costs are also significantly lower than even a few years ago and many firms have refinanced at long maturities.

Source: Fidelity Analyst Survey 2018

Overheard in Consumer Staples

- "The expansion of E-commerce triggers the emergence of smaller brands."

- "There are lots of risks that could change the outlook - weakening end-demand and particularly a slowdown in China, deflation, a raw materials price surge, regulation..."

- "Higher inflation would be a bonus - every retailer could profit from that."

- "Changes in local currencies are crucial for EM companies because costs or debt are often USD denominated, so currency volatility can impact margin and/or debt loads."

Hear from Gita Bal , director of research for credit, on why zero based budgeting may be a double edged sword for consumer staples companies.