Quality and momentum sectors have really been on a tear for the last 6-7 months, particularly global cyclicals and technology stocks. This has been fantastic for performance of the Fidelity Future Leaders Fund however it’s important to stay valuation sensitive.

High valuations, bullish sentiment, rising expectations and cyclically high earnings which can be beneficial on the way up, can endure a painful adjustment phase on the way down. Some high quality growth stocks have risen over 100% in the last 12 months and some moderation of enthusiasm is warranted.

I have been trimming some of these very high performing stocks given valuations are becoming stretched in a number of cases. History has shown that a 10% earnings miss which drives a shift in sentiment from ‘love’ to ‘unsure’ in a high quality or momentum name usually results in a 50% price fall over the next few months. Some examples of fallen angels and fading momentum stocks over the last few years include TPG Telecom; Navitas, Mayne Pharma and, iSentia.

A strong signal to be more valuation conscious is that quality stocks and momentum stocks are currently exhibiting high correlation. Structural and cyclical themes can be very powerful as sentiment drivers and ‘Mr Market’ tends to buy the basket, and not distinguish too much between stocks fundamentals and idiosyncratic risk in this environment. As one of Fidelity’s greatest investors once told me “Sentiment can be more powerful than fundamentals” - Anthony Bolton. One always needs to consider if earnings and fundamentals are driving their valuations at the moment, or if they’re being lifted by unsustainable low interest rates, momentum or extreme sentiment.

Transition stocks and value stocks in sectors such as utilities, infrastructure and telecommunications have not kept up with the strong market and become under-owned consensus sells. Investors need to be vigilant after a 9 year bull market as the price of risk is low, the cost of debt is low, liquidity is high, valuations are high and complacency is rising.

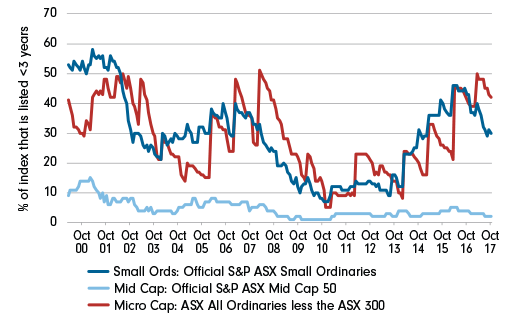

As a reminder to be cautious, I look at the ‘Toddler index’ below which signifies the proportion of each index where companies have been listed less than 3 years. Once again the index is at its highest levels (around 50% in micro cap and small cap) which is similar to other periods of high valuations, liquid debt and high liquidity such as 2000, 2007 and 2016. These young companies have not yet been tested through an entire business cycle and may be enjoying some sector valuation momentum. They also lack management and business maturity and can be temperamental as any parent who has lived through those toddler years well knows!

The toddler index

Source: Macquarie Research, Fidelity International

From a style perspective, the pattern of divergence between growth and value is rapidly repeating itself. Value stocks dramatically underperformed growth stocks in 2015, which was followed in 2016 by an aggressive value market for the unloved sectors of materials and resources. 2017 has been a reversal of this trend with growth, momentum and quality dominating performance tables.

The list of anecdotal absurdities continues to grow prompting many market commentators to speculate ‘somethings gotta give’. Record stock markets continue to run. A depiction of Christ by Renaissance master Leonardo da Vinci recently sold for US$450 million (AUD$591 million) smashing the previous record of US$179 million for the sale of a painting. Paul Newman’s Rolex Daytona was picked up for a cool US$17.8 million - the highest price ever paid for a watch at auction. And let’s not even mention property prices… If something does give in 2018, it will be that the price of risk rises and liquidity falls.

Finally, I’d like to thank you all for your support over the last 12 months and wish you a very happy Christmas and a wonderful New Year!