After a decade dominated by monetary largesse, 2022 marks a clear turning point. Central banks, most notably the Federal Reserve (Fed), are winding in the billions of dollars in extraordinary support they pushed through the economy. And they are doing so in a volatile atmosphere of war, environmental crisis, and inflation running at levels not seen for a generation. Taken together this threatens serious downturns in Europe and the developing world and quite possibly a slide into recession in the United States.

Stock, bond, and emerging markets have all weakened sharply this year and 2023 promises more volatility. We now view the road ahead in terms of three interconnected themes.

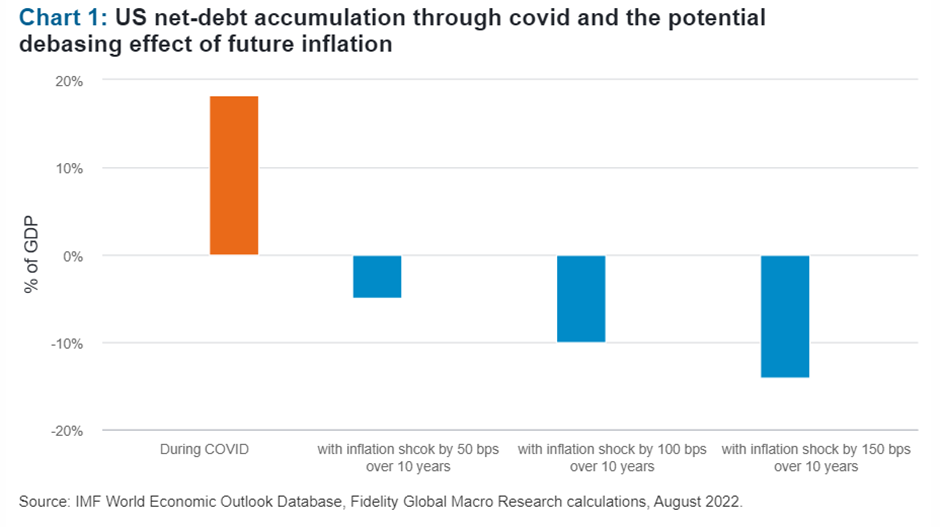

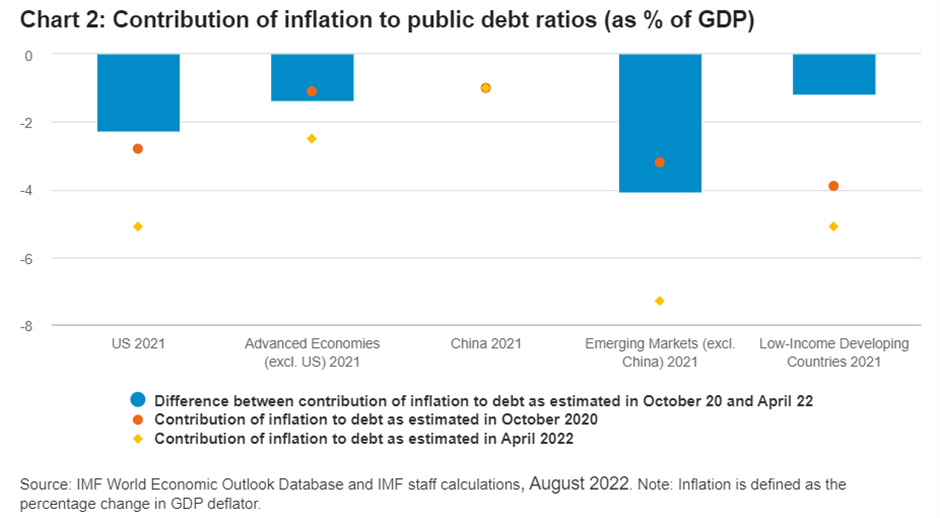

Debt and inflation

In the long run the plan, post-2008, was always to inflate away the huge debts built up as a result of the Global Financial Crisis. The past year’s combination of supply- and demand-side driven surges in inflation offers big, developed economies the opportunity to press ahead with that course: to reduce the real value over the coming years of the mountain of debt on national and central bank balance sheets, at a cost to consumers’ spending power at home and abroad.

We believe, therefore, that practical adherence to 2 per cent inflation targets may be done for now, and price growth may run - and be allowed to run - well above recent historical averages. Our experiences of the taper tantrum of 2013 and the Fed’s short-lived balance sheet run-off policy of 2018 tell us that investors simply do not believe that economies can function under the weight of high positive real interest rates for an extended period, something which is even truer today given the huge additional debts that were accumulated throughout the pandemic. So central banks, despite the rhetoric, will allow inflation to run high.

As the United Kingdom’s recent experience has shown, markets will be quick to punish overly loose monetary or fiscal policy. But the fundamental point remains: the Bank of England will be happy for inflation to prove slightly stickier than it has throughout the past decade.

We also see strong evidence that structural effects are taking hold: a steady and long-term march higher of housing costs in the United States will add to the pressure; the post-Covid “Great Resignation” may fade but is just the first hint of how aging populations will tighten labour markets and lead to higher wages; and the transition to net zero must bring with it a higher cost of carbon.

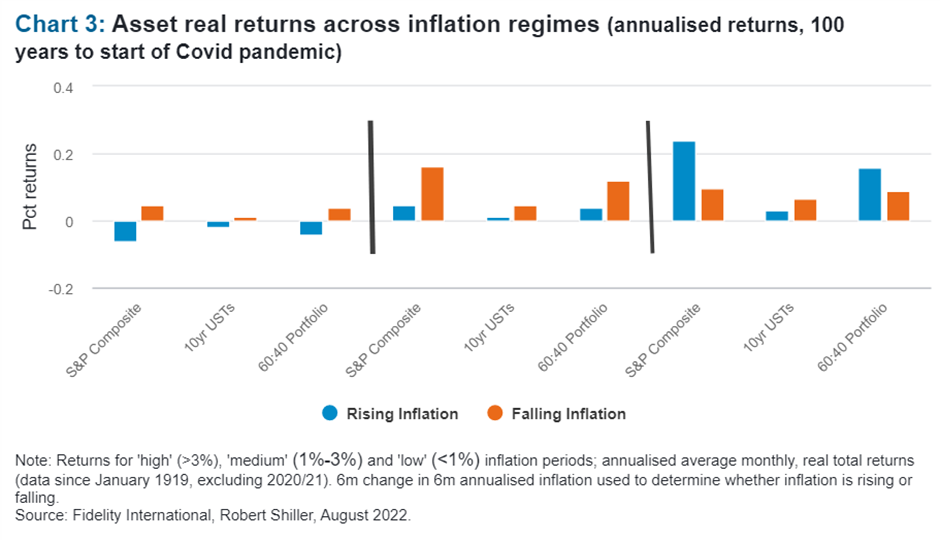

As Chart 3 shows, over the past 100 years most asset markets have performed very differently during periods of higher consumer price growth than during the sort of stable, low-inflation conditions that have dominated the past 20 years. Equities (as long as price growth does start to retreat) and direct lending tend to offer more protection from inflation, while picking the right sectoral plays is also likely to prove important.

Emerging forces

A second theme is closely linked to the first and speaks to a powerful new set of trends emerging to shape the world economy.

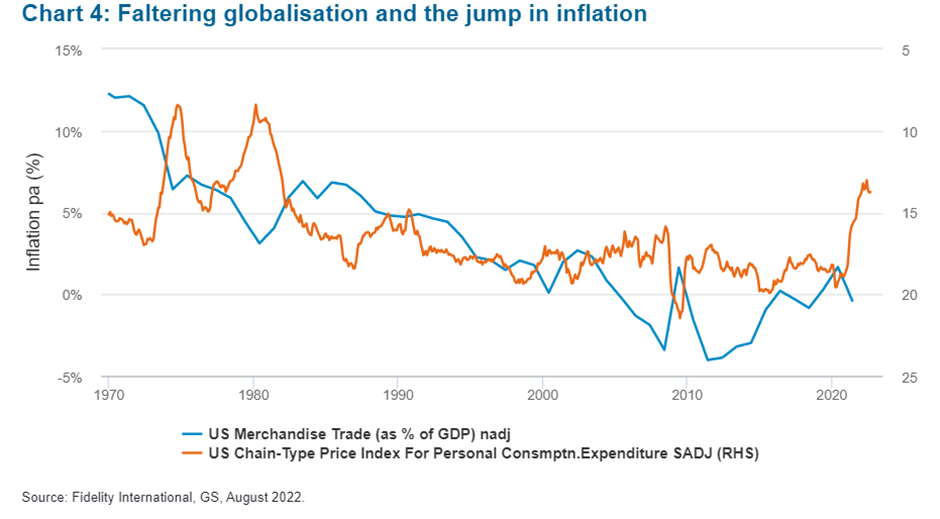

Russia’s invasion of Ukraine, added to the Covid-19 pandemic, tensions between the United States and China, and a rising populist tide of economic nationalism, is unwinding what had seemed like the unstoppable progress of globalisation over recent decades.

Europe’s move away from Russian supplies of energy and other commodities is a notable indication of this shift and is both a part and a parallel of the moves being made by many companies to make their supply chains more resilient. A new emphasis on energy security with more localised renewable sources as well as alternative fossil fuel supplies will require steep capital expenditure, technological development, and an acceptance that costs will be high through the transition.

The relationship between the United States and China is also likely to prove pivotal. After two decades of export-driven growth, Beijing is regulating harder and looking inward rather than outward for demand, while its global trading partners are seeking to produce closer to home. China is hoping that spending on infrastructure can continue to spur growth as it has in the past, with the focus now likely to be on sustainable infrastructure projects to support the rebalancing of the economy. For its foreign partners, however, alternative sources of cheap labour, goods and demand growth will be hard to source, and prices will rise as a result of the weakening ties with China.

The demographics of the world are also changing profoundly. The developed markets and China are now moving into the latter stages of transition, characterised by slowing, shrinking, and ageing populations, and we expect the impact on economies and markets to be material. Trend growth in China, Europe, and the United States will slow. As China’s population declines, the world’s will continue to expand, driven primarily over the next 50 years by South Asia, Latin America, and sub-Saharan Africa. India will be the world’s third largest economy by 2030 and commodity producers like Brazil and Chile should benefit if the supercycle in prices of vital raw materials continues, highlighting new sources of both demand and supply and, as the transition takes hold, creating investing opportunities.

Faster cycles

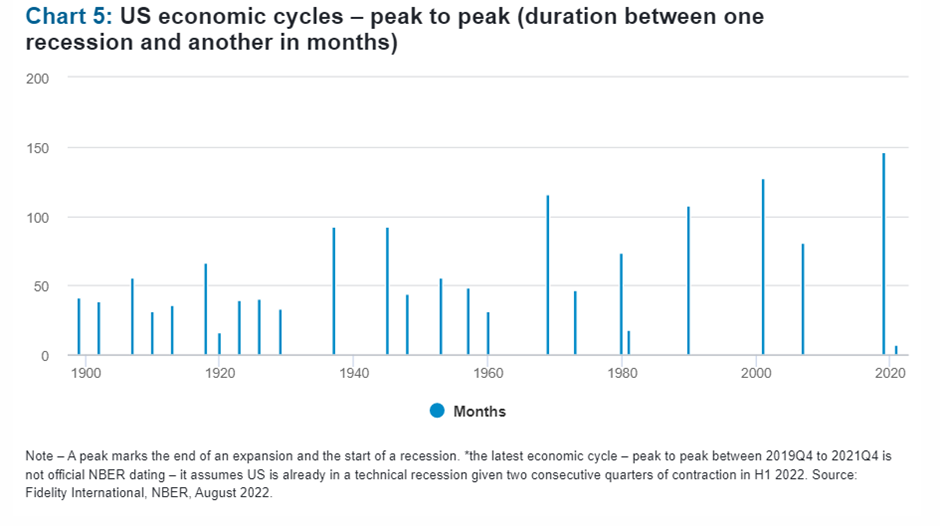

We also believe that inflation and policy tightening may mark a return to the more volatile cycles we saw prior to the 1980s. The 40 years since 1983 have seen only four recessions compared to nine in the previous 40. That may now change and the resulting environment is likely to put a premium on active management and the ability to make quicker adjustments to allocation and portfolio dynamics.

The comparisons with the past have become obvious. Central banks flooded the system with excessive liquidity in the wake of the Covid-19 pandemic, and US money supply growth, for example, now resembles the spikes seen in the first half of the 20th century. All this, of course, before Europe confronts the fiscal and borrowing implications of the current energy crisis.

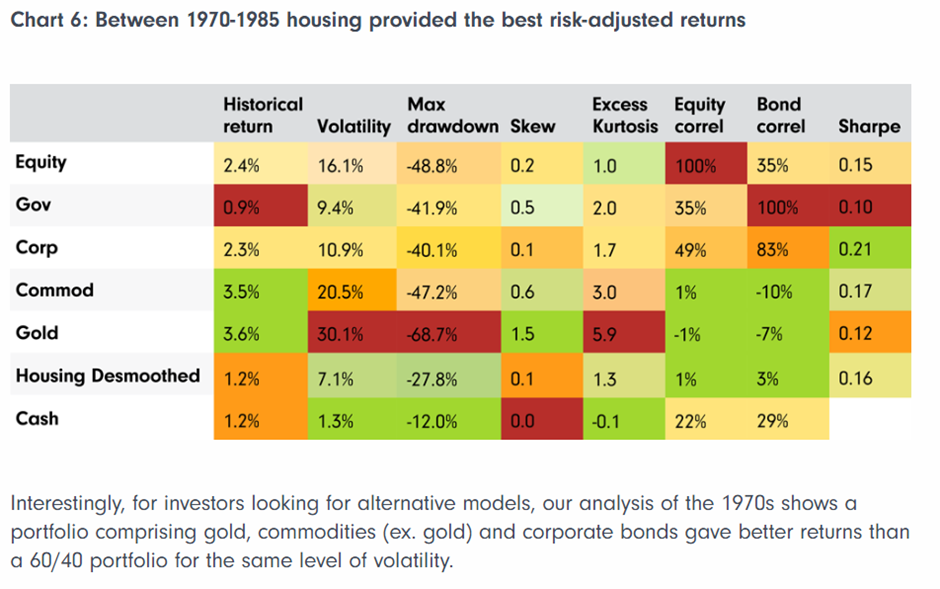

This will have detrimental effects on average asset-class real returns, especially if inflationary pressures prove particularly strong. History suggests that housing can be a strong diversifier through periods of heightened volatility with a similar risk-adjusted return as equity and a negative correlation with debt and equities.

Buckle Up

As we head towards a troubled northern hemisphere winter, a regime change now feels well under way. The era of cheap money is over, central banks are raising nominal interest rates sharply, and two-way volatility has returned.

The past decade was largely a one-way trade on growth, with inflation staying low, but higher rates will create new opportunities for long-term investors, as will a continuing shake out of markets that have grown fat on that diet of easy money.

The cost-of-living crisis may be here to stay for some time as structural inflation beds in, with resulting implications for consumer demand and growth. But investors will also be rewarded for allocating capital toward new themes; be it investment in green transition technologies, the new engines of growth in the developing world, or simply a different and faster-changing mix of assets.