Key takeaways:

-

Rate cuts look difficult this year: The committee is becoming more restless about above-target inflation, while higher energy prices could push core PCE (Personal Consumption Expenditures) even higher by year-end. Warsh may prefer to focus on median and trimmed mean PCE, but many FOMC (Federal Open Market Committee) members are likely to judge that demand and labour-market conditions remain too firm to justify cuts.

- FOMC may limit other Warsh intentions: Warsh appears likely to push for changes to the Fed’s communication regime and for a smaller Fed balance sheet. On the former, he will be able to reduce the frequency and information given at press conferences, but he will be unable to unilaterally halt the publication of the dot plot or FOMC member speeches. On the later, changes to balance sheet strategy would also require broader committee support, meaning reforms are more likely than significant changes.

- Markets should prepare for a less predictable Fed: A lighter communication regime may reduce false precision, but it is unlikely to produce cleaner price discovery. With fewer explicit rate-path signals, more visible dissents and greater reliance on speeches and incoming data, investors may need to demand a higher premium for policy uncertainty, particularly around turning points.

Warsh’s dovish instincts likely to be blunted by Fed Committee

The rise of Kevin Warsh to the chair of the FOMC has been long in the making. His association with the Fed goes back to 2006, when he was made a Federal Reserve governor, a role he kept until he resigned in 2011 in protest against the extension of quantitative easing. He was also widely tipped to be in the running to replace Janet Yellen in 2017, with President Trump ultimately opting for Jerome Powell. Since then, he has been a notable Fed watcher, penning critical articles against further rate hikes in 2018 and arguing the Fed was too slow to react to Covid-19 in 2020.

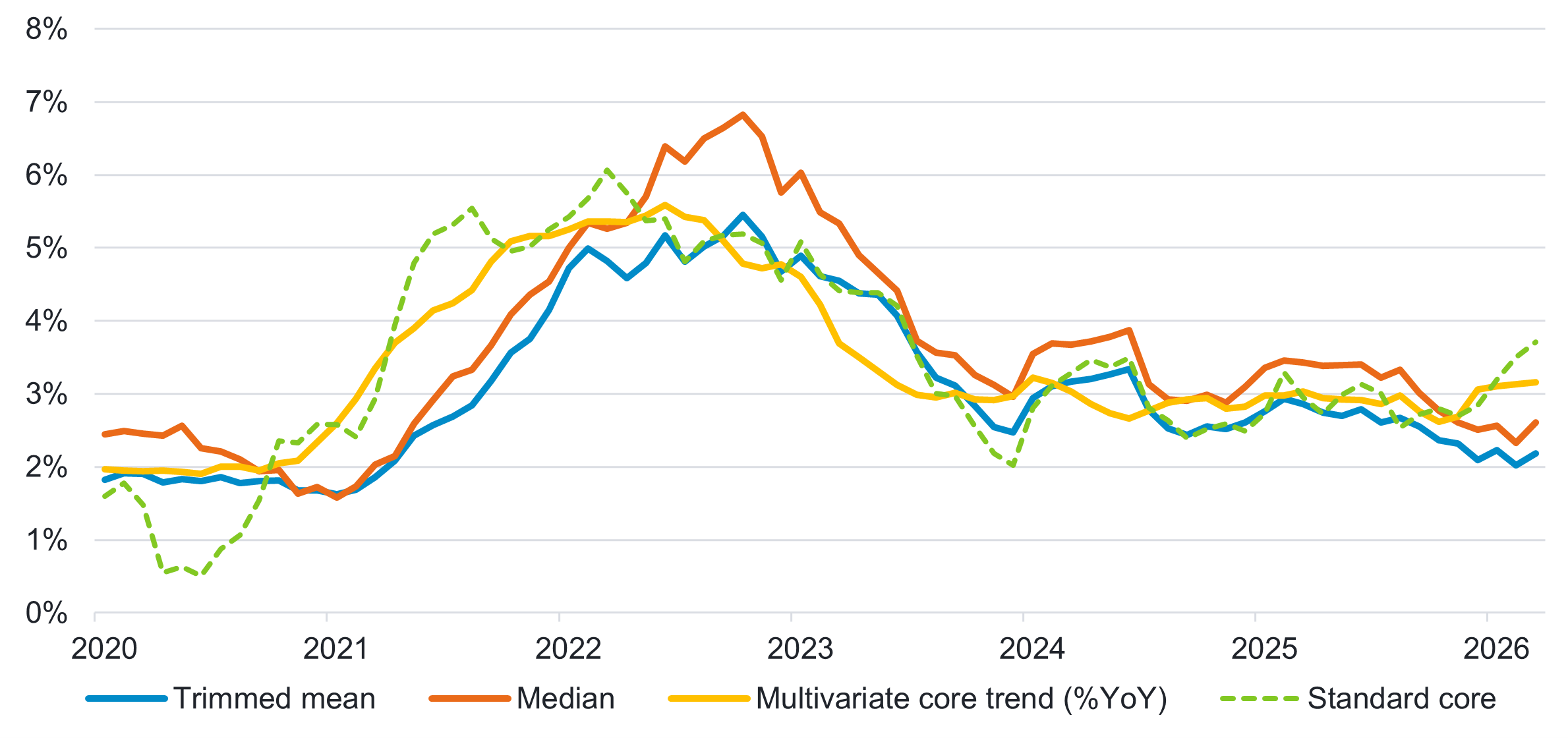

Kevin Warsh arrives at the Fed with a dovish inflation story to tell. His preferred measures of underlying inflation, median and trimmed mean PCE, are disinflating quickly on a six-month annualised basis and are now at or near the Fed’s inflation target, tracking at 2.6% and 2.2% respectively (Figure 1). By way of contrast, standard core PCE has been accelerating over the last 4 months and is now close to 3.7% (nearly double the Fed’s inflation target), largely as a result of much higher than normal goods inflation driven by President Trump’s Liberation Day tariffs last year.

Figure 1: Different inflation measures tell different stories

Source: Fidelity International, Macrobond, May 2026.

As Kevin Warsh argued in his confirmation hearing, these alternate measures of inflation give the Fed more space to ease than standard core PCE would suggest.

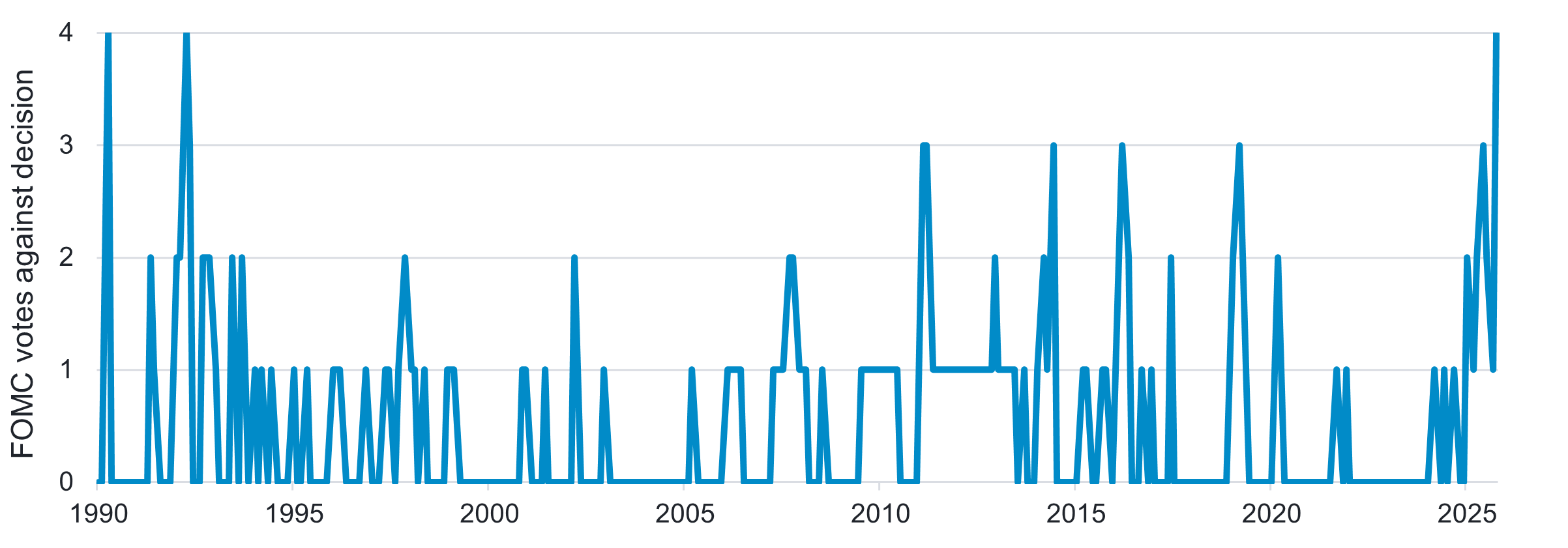

However, the current committee looks in no mood to agree with Warsh. As can be seen in Figure 2, dissents against recent FOMC decisions are running at levels rarely seen since the early 1990s. We believe this is indicative of a committee becoming restless with the persistence of above-target inflation, a problem that will only get worse. Our calculations suggest higher global energy prices as a result of the Iran conflict will drag core PCE from around 3.2% on a year-on-year basis today, towards 3.5% by the end of the year - 1.5 percentage points above target.

Figure 2: The current FOMC is becoming restless

Source: Fidelity International, Macrobond, Bloomberg, May 2026.

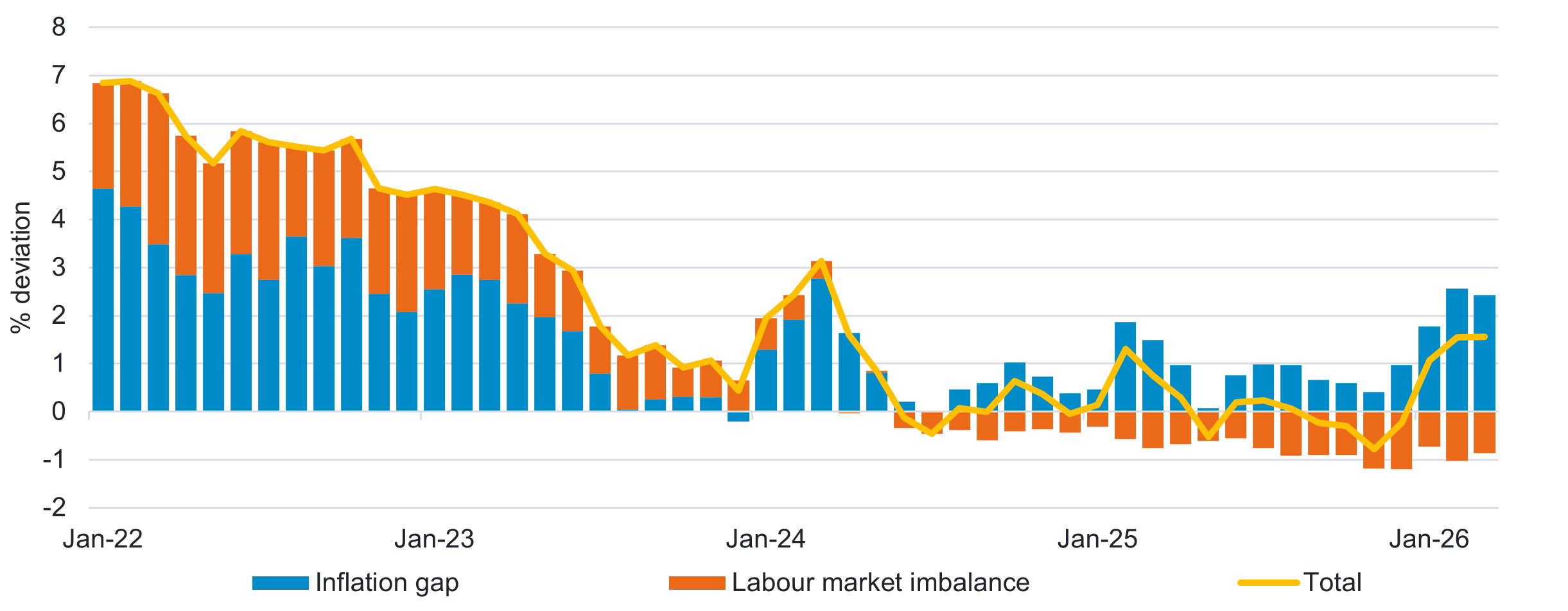

The result is that Warsh’s first year as chair is likely to be defined by a struggle between what he wants to do versus what the committee will allow him to do. He may prefer a broader inflation dashboard, and he may be able to argue that median and trimmed mean inflation justify a more dovish stance. But for many committee members, standard core inflation is still too high - demand continues to look resilient enough to absorb the oil shock, and the labour market is not showing enough weakness for it to meaningfully lower inflation (Figure 3).

Figure 3: Fed’s mandate now being challenged on the inflation side

Source: Fidelity International, Macrobond, May 2026. Inflation gap = difference between core PCE 3M SAAR rate and Fed’s target; labour market imbalance = excess/shortage of labour divided by total labour force; labour excess shortage is defined as the difference between cumulative labour demand and labour supply since 2019.

We believe the policy implication is therefore straightforward: Warsh is unlikely to be able to push through cuts this year.

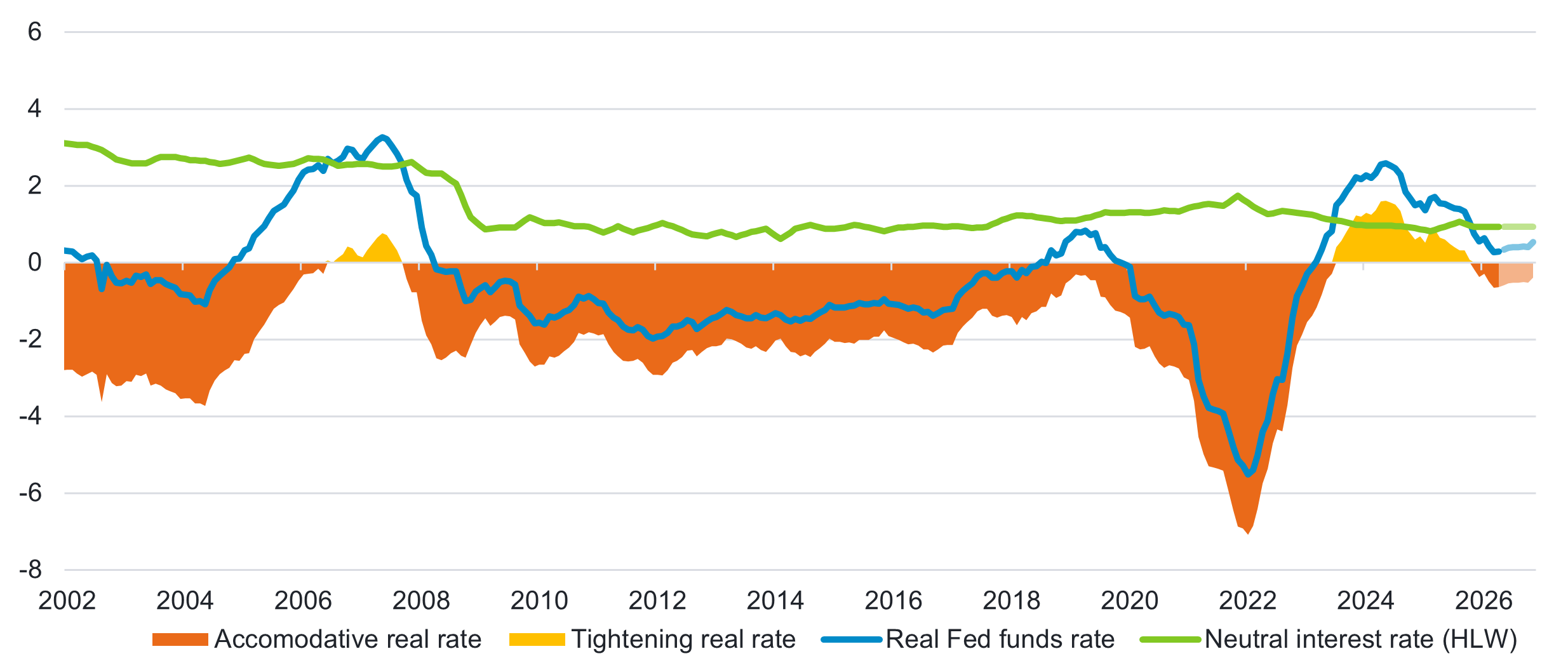

This does not mean, however, that policy will stay genuinely tight. In a world of higher and rising inflation, holding rates where they are is effectively a form of easing, as leaving nominal rates unchanged allows real policy rates to fall (Figure 4). We expect Warsh to embrace this argument publicly, with Trump the intended audience, after he fails to force a rate cut through the committee.

Figure 4: With inflation now rising, holding rates already implies monetary policy easing

Source: Fidelity International, Fidelity Global Macro Team forecasts, Macrobond, May 2026. Fed funds rate deflated by Core PCE. Lighter colours indicate forecasts.

A lighter-touch Fed in the long run, but tempered by committee-based decision making

In addition to his desire to pivot to broader inflation metrics, we see two other long-term implications of Kevin Warsh’s tenure in charge of the Fed, impacting the communication regime and balance sheet policy.

Warsh intends to implement a materially different approach to Fed communications. He believes forward guidance, rate and economic projections, and model-consistent narratives can force policymakers into a corner, pressuring them to be consistent with previous guidance even when conditions change. That implies fewer press conferences, less narrative management, and a push to reform or remove the interest-rate dots in the quarterly published Summary of Economic Projections. Instead, investors will be left to infer FOMC intentions from speeches, dissents, data, and market functioning. If implemented, this would be a communication regime much more akin to the pre-financial crisis era.

Table 1: Long-term implications of Kevin Warsh in charge of the Fed

| Policy | Warsh's view | Ability to make unilateral change | Broader FOMC views |

|---|---|---|---|

| Measuring inflation | Places greater weight on ‘underlying’ inflation, especially trimmed mean and median measures, rather than relying on core inflation | Limited | Fed already monitors these measures in the Teal book. Resistance likely if framed as a pivot during an inflation upswing. |

| Communication policy | Strongly critical of current Fed communication, especially forward guidance, the dot plot, and the frequency of press conferences | High on press conference, limited for dots and speeches by other FOMC members | Some sympathy exists with Warsh’s view, as members dislike media fixation on individual dots. Full abolition of dots would require committee agreement, so reform is more likely than removal. |

| Balance sheet policy | Prefers a smaller Fed balance sheet and a higher bar for using it in macro-financial emergencies | Limited | Balance sheet strategy is decided by the full FOMC. His influences may be greater in setting the reaction threshold than in dictating the steady-state size. |

Source: Fidelity International, Fidelity Global Macro Team assessments, May 2026.

In addition, Warsh’s preference is for a narrower Fed footprint, including a smaller balance sheet, less involvement with fiscal and debt management choices, and a higher bar for macro-financial emergencies to trigger Fed liquidity/asset purchases.

On the face of it, this points to a policy mix of lower rates, balance sheet run-off, and initially more synchronisation with the Treasury, with the likely outcome being a steeper real yield curve. This would need to be co-ordinated with the Trump administration’s broader bank deregulation and credit creation agenda, where lower rates, smaller reserves, and looser regulatory constraints are intended to push credit towards households and SMEs.

However, once again, what Warsh can achieve is more constrained than he might like. In our view, Warsh will have clear discretion over the cadence and tone of press conferences, but much less authority over the quarterly dot plot and balance sheet strategy, both of which will require broader FOMC buy-in. Powell is now highly likely to remain on the board beyond his term as chair, which adds a further constraint. Firstly, it is one less Trump appointed governor who can vote for Warsh’s “regime change” agenda, and secondly, given Powell’s high standing on the committee, Powell could slow institutional decision making if he views the changes as undermining Fed independence.

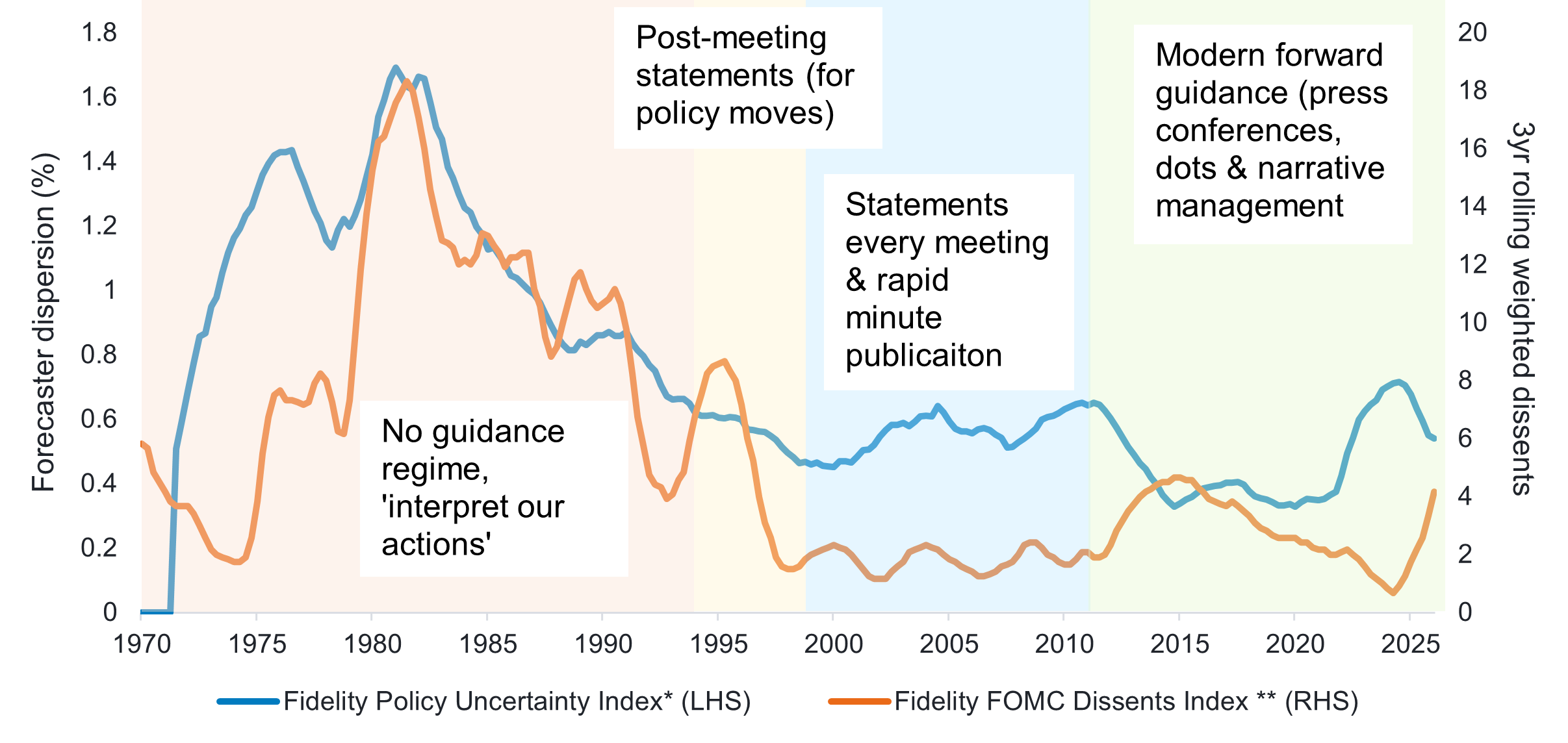

The larger issue for financial markets is that a lighter communication regime may also raise macro policy uncertainty. As Figure 5 shows, a lower level of Fed communication has tended to coincide with higher forecast dispersion and more visible FOMC disagreement. Warsh may be right that the current regime creates false precision, but investors should not assume the alternative is cleaner price discovery. A Fed that speaks less, publishes fewer rate-path signals, and tolerates more dissent would likely mean higher rates volatility, especially around turning points.

Figure 5: Less communication from the Fed tends to be associated with higher macro uncertainty and more FOMC disagreements

Source: Fidelity International, Macrobond, Fidelity Global Macro Team calculations, May 2026. *Average NTM forecaster dispersion of inflation and interest rates from the Philadelphia Fed Survey of Professional Forecasters; inflation only before 1985 – 3-year moving average. **Rolling 1-year sum of dissenting votes against FOMC policy moves. Dissents from governors weighted higher – 3-year moving average.

In summary, a Warsh chairmanship is unlikely to deliver an immediate shift in Fed policy, but it does introduce a more subtle and potentially consequential change in how policy is framed, communicated, and interpreted. The tension between Warsh’s preferences and a more cautious, and at times resistant, committee will shape both the path of rates and the clarity of the Fed’s reaction function. Investors will need to prepare for less explicit guidance and a greater focus on underlying data and dissent, and demand a higher premium for navigating higher policy uncertainty.