The overwhelming majority of Fidelity International analysts report a growing emphasis on environmental, social and governance (ESG) issues among the companies they cover. But as they focus more on ESG, companies are starting to realise the scale of the challenge ahead.

Key takeaways

- Nearly three-quarters of analysts report a growing emphasis on ESG at most of the companies they cover

- China has seen a notable improvement in climate risk disclosure, albeit from a low base

- Slightly fewer companies are now expected to reach net zero by 2030, while biodiversity and oceans appear to be neglected areas

Virtually everyone has got the memo now.

“ESG is now mentioned in almost every single company communication, ranging from quarterly earnings to capital market days,” says one Fidelity analyst covering European industrials.

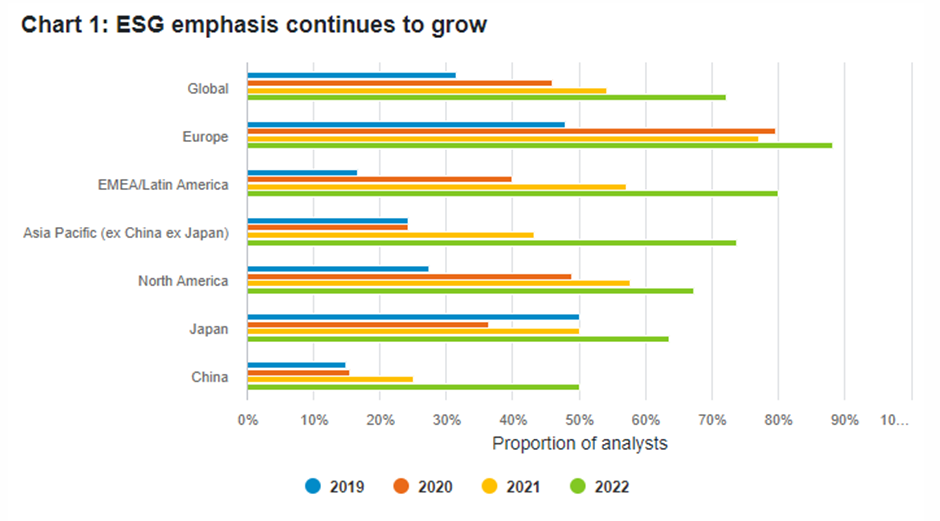

Indeed, 72 per cent of analysts now report a growing ESG emphasis at a majority of the companies they speak to.

“Have you seen a growing emphasis among your companies to implement and communicate ESG policies in the last year?” Chart shows the proportion of analysts who believe ESG awareness is growing at a majority of companies. Source: Fidelity International Analyst Survey 2022.

The biggest improvements have come in Asia. Following Beijing’s September 2020 announcement that China will aim to be carbon neutral by 2060, half of the analysts covering China now say most of their companies increased their focus on ESG over the past year, up from a quarter at the start of 2021. There have also been big jumps in Asia Pacific (ex-China and Japan) and EMEA/Latin America.

“Companies are certainly aware of the zeitgeist and have been making attempts to meet investor demand for increased disclosures and action,” says an IT sector analyst covering China. “There have been more companies engaging with us to ask our opinion on what to disclose.”

At a sector level, healthcare and financial companies have seen notable increases in ESG emphasis over the past 12 months. For financials, the proportion of analysts reporting growing ESG emphasis at a majority of companies has jumped to 77 per cent, up from less than half last year. As one European banking analyst puts it: “ESG is getting more investor attention and that is being passed on to companies.”

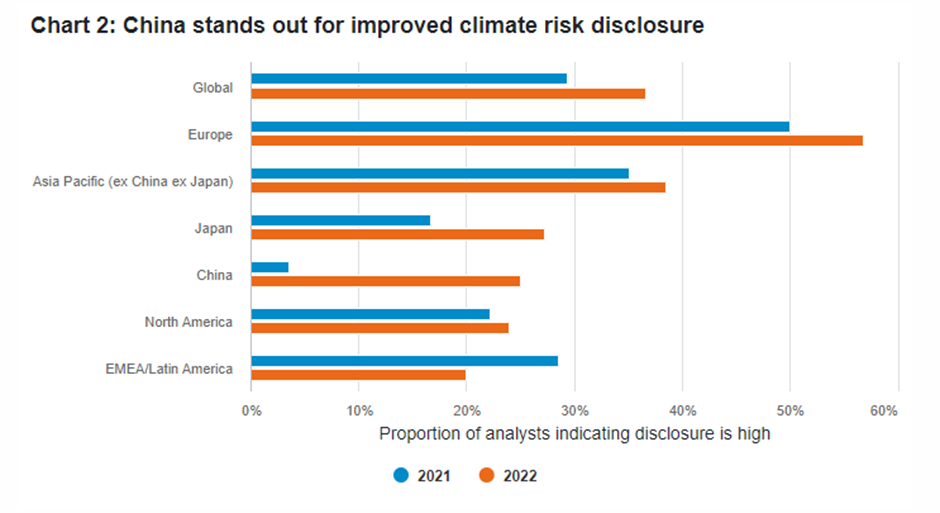

One impact of this is the increased number of analysts reporting high disclosure of climate-related risks among their companies.

“How would you rate your companies’ disclosure regarding their approach to climate-related risks relevant to their businesses?” Chart shows proportion answering 5-7 on a scale from 1-7 where 1 is very poor and 7 is excellent. Source: Fidelity International Analyst Survey 2022.

China again shows the biggest improvement, while the story from North America and EMEA/LatAm is more disappointing. Europe remains out in front, but Japan shows a notable uptick in disclosure, as the recommendations of the Task Force for Climate-related Financial Disclosures continue to gain traction there.

Reality bites

However, the survey also contains more sobering responses.

“Many companies still don’t have ambitious quantitative targets,” says a European telecoms analyst.

This sentiment is echoed in other regions and sectors. Referring to North America, one materials analyst says that while companies there have in the main established broad commitments to address their environmental impact, “most lack near-term targets that could have a significant impact on the next 12 months.”

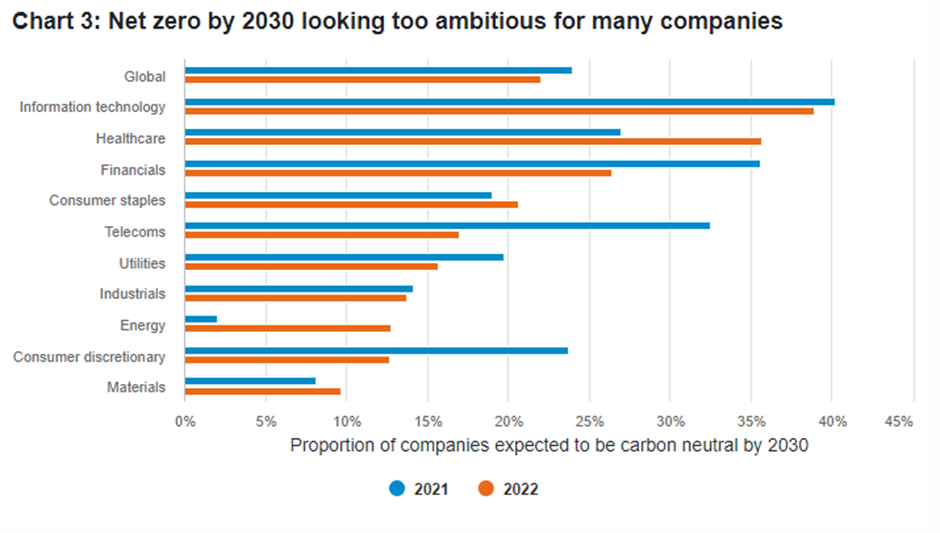

The lack of urgency is reflected in one of the survey’s more disappointing ESG findings. On a global basis, Fidelity analysts now expect a slightly lower proportion of their companies to reach net zero by 2030 than was the case last year. This may be partly due to more accurate assessments of what is required to reach net zero, and because some industries will need to increase emissions in the short term as they replace more carbon intensive processes.

“What percentage of your companies do you estimate will be carbon neutral (scope 1, 2 and 3) by 2030?” Source: Fidelity International Analyst Survey 2022.

It is likely this chart also reflects the impact of other pressures such as supply chain issues and cost inflation, highlighted elsewhere in this survey, that are absorbing capital that might otherwise be put towards climate goals. It also aligns with what the science is telling us, that we are currently not on track to limit warming in line with the Paris Agreement and doing so will take a great deal of effort.

“It seems 2050 is a more feasible target for now,” says one Asia-Pacific analyst, noting for instance that shipping and airline companies’ climate targets rely on the use of alternative fuels and more efficient fleets that have yet to be developed.

One bright spot comes from the energy sector, where the proportion of companies expected to be carbon neutral by the end of this decade has jumped from just 2 per cent last year to 13 per cent. More encouragingly, our analysts now expect 74 per cent of energy companies to reach net zero by 2050, up from just 29 per cent a year ago.

“The benchmark is fast becoming carbon neutral on a scope 3 basis (indirect carbon emissions) by 2050,” says one European energy analyst, adding that most European companies will probably try to achieve this by reducing oil and gas production and ceding market share to non-European producers.

Biodiversity and oceans still low on the agenda

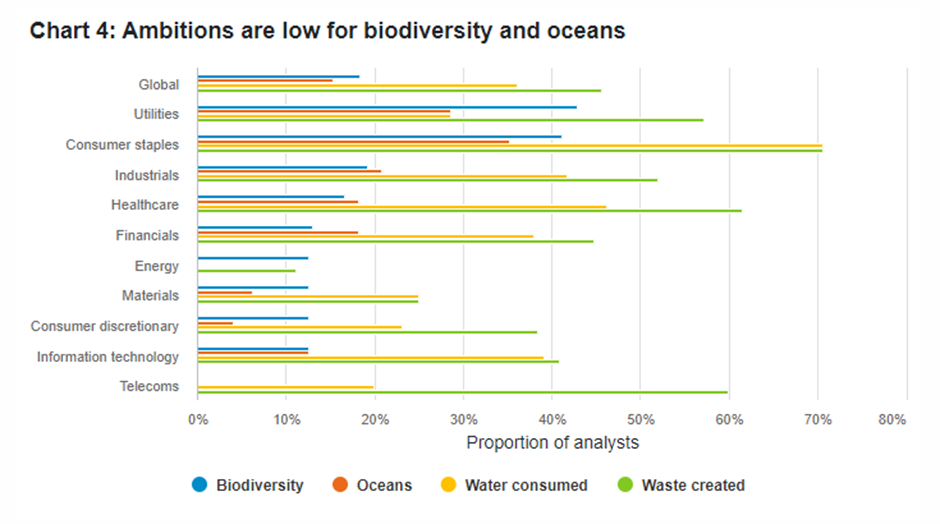

Unfortunately, increased emphasis on climate change and ESG is not yet translating into concerted efforts to tackle other environmental challenges. Although companies are making progress on water and waste, biodiversity and oceans remain much further down the corporate agenda.

“To be honest these issues, particularly biodiversity and oceans, are rarely (if ever) discussed,” reports one analyst covering European healthcare companies, adding that companies are more proactive at reducing water consumption and waste.

“To what extent do you expect your companies to reduce their impact on the following areas over the next 12 months compared to the last 12 months?” Chart shows proportion answering 5-7 where 1 means will not reduce their impact and 7 means will significantly reduce their impact. Excludes analysts who say their companies do not need to reduce their impact. Source: Fidelity International Analyst Survey 2022.

Deeper and broader

While 2021 was another year of progress, companies need to deepen their commitments to tackling climate change, which includes improving climate risk disclosures. There is also a strong case for broadening commitments to incorporate biodiversity, oceans, and other environmental impacts. This will not be easy both in terms of target setting and implementation. However, more and more companies are now rolling up their sleeves and getting to grips with the reality of their ESG responsibilities, not least financial institutions.

Many banks and asset managers have signed up to initiatives such as the Glasgow Financial Alliance for Net Zero designed to help drive investment towards the energy transition and hold companies to account for their role in achieving carbon neutrality. Where capital goes, corporates should follow.