China is developing a new ‘third pillar’ superannuation scheme to support its ageing population, one that could reshape both ordinary people’s retirement plans and the country’s asset management industry.

“Making the world more suitable for the elderly to live in” hardly seems like an online discussion topic that would set the Chinese internet aflame.

But at Douban, a social media platform popular among young mainland Chinese fans of music, books and movies, a small but rising number of posts are starting to focus on issues related to retirement. In groups like “Making the world more suitable for the elderly to live in”, which was set up in January and has more than 34,000 members, people trade tips on caring for elderly family members, where to find senior-friendly mobile apps, or how to prepare financially for retirement.

China is the world’s most populous country, but, as a result of lower birth rates over the years, it is also aging rapidly; social media trends reflect a shift that is playing out more broadly as awareness of retirement-related issues rises across the country. One of the most important areas is in financial planning. In April, the government launched China’s long-awaited superannuation scheme, helping to ease pressure on the main state plan. The new so-called third pillar private retirement savings scheme sits alongside state (first pillar) and corporate (second pillar) superannuation plans. It provides supplementary retirement funding options and savings incentives in the form of tax breaks for Chinese people.

It’s a development being closely watched by global asset managers, including Fidelity, which hope to leverage their experience in the US or European markets with a new generation of Chinese who are saving for retirement.

Comparisons with other big markets are telling. America’s individual retirement accounts (IRAs) are roughly comparable to the new and nascent superannuation scheme in China, and they play an important role in the US retirement system. Assets in US IRAs totalled US$13.9 trillion at year-end 2021, accounting for 35 per cent of the country’s retirement assets, according to figures from the Investment Company Institute. About 45 per cent of IRA assets, or a total of US$6.2 trillion, were invested in mutual funds.

Three pillars to stand on

So far, it’s a very different story in China. The traditional first pillar state scheme dominates China’s retirement system. The compulsory program, with a total size of more than 6 trillion renminbi (US$837 billion as of Nov. 29) at the end of March 2022, according to official statistics, provides basic benefits for 73 per cent of the 1.4 billion population. Despite the rapid increase in its total size, people can’t rely only on the first pillar to maintain living standards after retirement. The superannuation people will receive upon retirement accounts for less than 50 per cent of their pre-retirement income, according to one 2019 estimate from McKinsey & Company.

The second pillar, with a total size of 4.5 trillion renminbi (US$628 billion as of Nov. 29), offers annuities to employees of state-owned enterprises and government employees. However, so far it covers only about 72 million people.

As Chinese life expectancy has increased from 68 years in 1981 to 78 years in 2021, the population of retirees continue to swell, creating tremendous burden on the two existing schemes. The situation has led to some calls to increase the retirement age, which is currently set at 60 for men, 55 for female civil servants and 50 for blue-collar women.

This context is what has led to the third pillar, which includes two important parts: the private scheme launched this year and other individual commercial superannuation products.

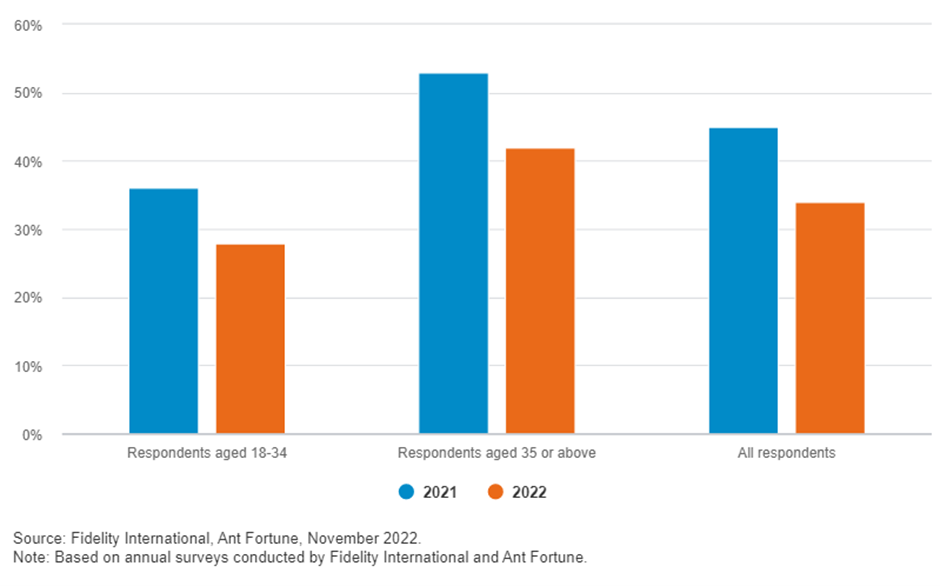

Chart 1: Proportion of respondents seeing government superannuation as their key source of retirement income

Not your grandparents’ superannuation plan

A generational shift is taking place when it comes to views on retirement savings in China. Fidelity International and Ant Fortune, the wealth management platform under Ant Group, have conducted a China Retirement Readiness Survey every year since 2018. The 2022 survey, published in November, showed that young people in China are expecting to rely less on the state super program than older generations, as more retirement funding options become available. Only 28 per cent of respondents aged between 18 and 34 plan to count on the first-pillar savings as their main source of retirement income. In contrast, the ratio is 42 per cent for respondents aged 35 or above.

We expect growing demand from China’s younger generations for retirement funding options to support fast development of the third pillar. According to the new policy announced in 2022, the government will trial it in some cities for a year, before rolling it out across the whole country. The scheme allows employees to make voluntary contributions of up to 12,000 renminbi a year to superannuation accounts which will qualify for tax relief. That cap is equivalent to about 11 percent of urban non-private sector workers’ annual wage in 2021.

Funds in the superannuation accounts can be invested in savings deposits, bank wealth management products, mutual funds or insurance products. No tax will be levied on investment income for the time being, until it is realized or withdrawn. The tax payable on withdrawal of superannuation funds has been slashed to 3 per cent – the same as the country’s lowest income tax rate.

Investor education is key

Despite the growth potential of superannuation, it may not be easy to attract new customers as they are required to take a more active role in investment - that includes bearing investment risks over a long time horizon and making tough decisions on how much money to set aside and which investment products to choose. It could be intimidating for people who have little to no investment experience.

About 30 per cent of under 35s and 29 per cent of over 35s who responded in the Fidelity and Ant survey said lack of knowledge about retirement or long-term investment topics is one of the key reasons why they haven’t started saving for retirement. The percentages were 23 percent and 19 percent last year, respectively.

More investor education will be essential to developing the third pillar. Financial institutions can help raise awareness of long-term retirement investment and coach individual investors on how to make appropriate retirement plans, choose the right investment products and focus more on long-term returns.

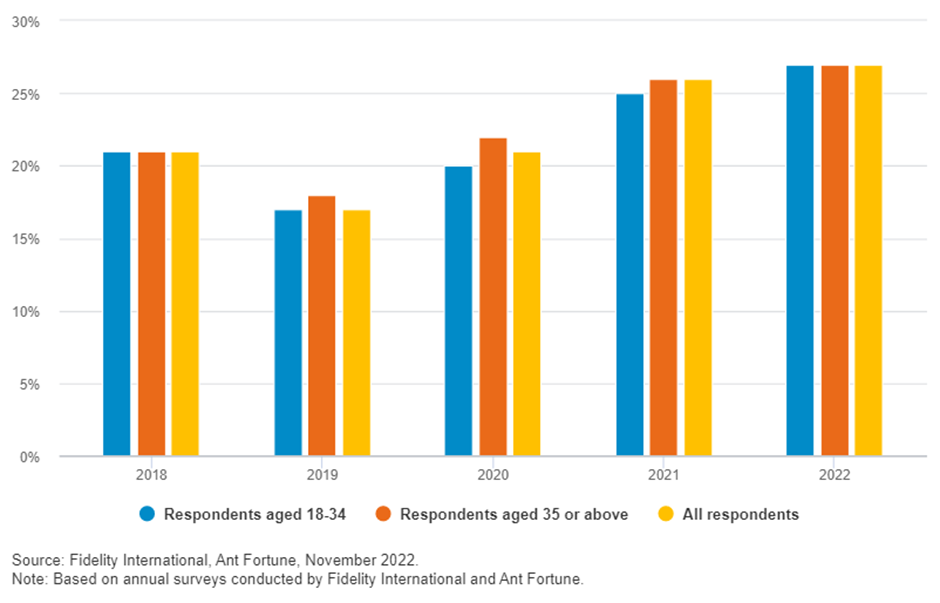

Chart 2: Percentage of monthly income for retirement savings

More to come

While China’s third pillar is still in its infancy, policy support should do much to help it mature quickly. President Xi Jinping said in a speech delivered to the 20th Communist Party Congress in October 2022 that China will develop a multi-pillar superannuation system in the coming years.

And the early indications are encouraging. The survey by Fidelity and Ant showed people across age groups are gradually making more prudent retirement plans. Both under 35s and over 35s allocated about 27 per cent of monthly income for retirement saving this year, compared with 25 per cent and 26 per cent, respectively, for the two age groups in 2021.

The latest development came in November 2022, when Chinese policymakers issued detailed regulations, providing guidance for investment products linked to the third pillar private superannuation scheme. We think it won’t be long before we see the new scheme fully take off. If successful, it could mark the start of a new era of choice and flexibility for Chinese superannuation savers as they seek to plan a comfortable post-retirement life. And “Making the world more suitable for the elderly to live in” will be more than just a snappy name for an online chat group.