Fidelity’s fourth Annual Applied AI Workshop in London was another reminder of the rapid pace of innovation in this technology, and the importance of staying close to entrants in this space. It reinforced our existing preference for investing in AI infrastructure and hardware providers over end applications at this stage of the technology life cycle. We think investors continue to underestimate the scale and duration of required infrastructure spending, meaning risk-reward on these stocks continues to look enticing.

Ongoing challenges to software

The event was another great opportunity to assess the state of enterprise AI development, this time among private companies who are looking to disrupt incumbents. The pace of change we have seen in AI over the last four years means it is more important than ever to be meeting companies, getting a firsthand account of how they are using this technology. We met five companies from different countries, all catering to different end markets, with different disruptive effects on areas such as software, gaming, traditional automotive Original Equipment Manufacturers (OEM), and legal services. All were end application providers, as opposed to AI infrastructure / hardware.

The key takeaways for us from these meetings, particularly the one with Poolside AI, a company building advanced foundation models and agents designed to help enterprises write, understand, and maintain software at scale, is the challenges posed to existing software models and the rapid pace of evolution among agentic AI. Systems which can pursue goals autonomously rather than relying on single prompts and human approval. Can existing software providers adapt fast enough? They face a tricky balancing act between protecting their existing ecosystems, versus allowing greater outside access. The latter may lead to faster ecosystem growth and adoption, but mean a greater risk of disintermediation and weaker customer lock-in.

Less disruption risk in back-office software

We remain cautious of ‘front office’ areas of software to do with things like client interaction, sales, trading, etc, where the pace of AI innovation is making it hard to find defensive businesses. Companies may not have an alternative to this software now but may well do in a year’s time which also shows the danger in linear thinking around AI technology, something many investors are prone to. We do think there are opportunities among more back office, system-of-record, type software, where we see less disruption risk. While it is relatively easy to replace front office applications with new AI systems, it is much harder to do this with business support data. In our view, the difficulty in switching to new AI solutions in this area still outweighs the benefits gained from switching for most businesses.

It is also worth pointing out that the AI disrupters themselves can be at risk of disruption, as seemed to be the case with one of the companies we met who provide an LLM for use by law firms. It was not clear that its data moat or product is differentiated enough to provide a base for long term success.

‘3D AI’ – not there yet

Over time, we expect to see more evidence of a move to ‘physical AI’ embedded in things like driverless cars. We met with a UK autonomous driving systems business, who train the model and build the software which is licensed to end auto OEM customers. This is a highly competitive arena with different technical approaches from the likes of Waymo in the US and a handful of Chinese players operating in Asia. The race is on for what will be an expanding opportunity set as we move from 2D to 3D AI.

Our preference for hardware

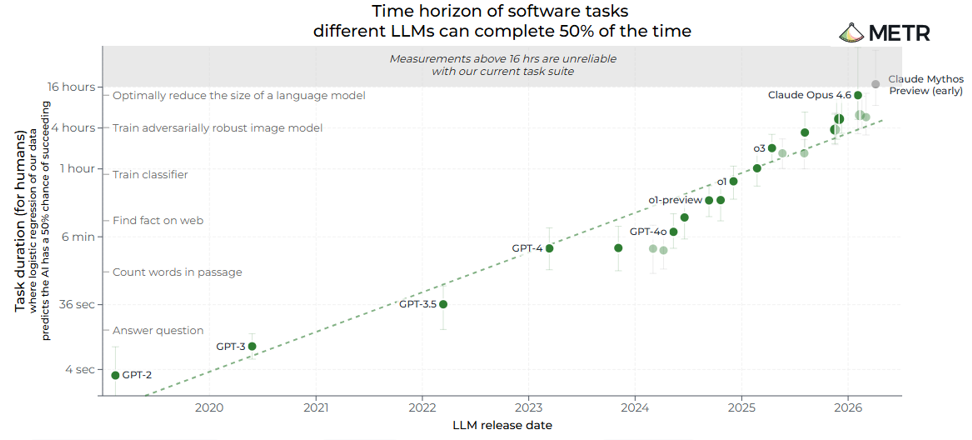

We continue to prefer ‘AI enabler’ plays in hardware and semiconductors to end applications / innovators in areas like software, media and entertainment. Models undertaking more complex tasks and exploding token usage means demand for computer, networking, memory, storage and power also increases dramatically. Again, this growth is not linear (see chart below). A simple chatbot may use a relatively small number of tokens, but as you move to more sophisticated Agentic AI workflows usage per task multiplies. Proliferation and widespread adoption of AI models should mean compute remains constrained for years to come, meaning a very bullish setup for AI semiconductor providers. While in the longer term we will see more AI innovators cropping up, this layer of the investment opportunity set is still immature and needs more infrastructure to keep evolving.

Source: METR, May 2026

Picks and shovels over applications

New AI disruptor applications are proliferating, and some of these could turn into long term winners. Maintaining a close eye on emerging private market businesses is thus more important than ever. But the day reinforced for us why we prefer to focus on the infrastructure layer or the ‘picks and shovels’ of the AI boom. While visibility around winners in the application or innovator layer remains unclear, we are confident that the growth in token consumption is going to keep increasing rapidly, meaning the bullish set up continues for many AI hardware and semiconductor stocks.