The soaring cost of living has pushed US consumer sentiment to an all-time low. Slumping sentiment is being mirrored in increasingly reserved spending habits, though inflation continues to climb.

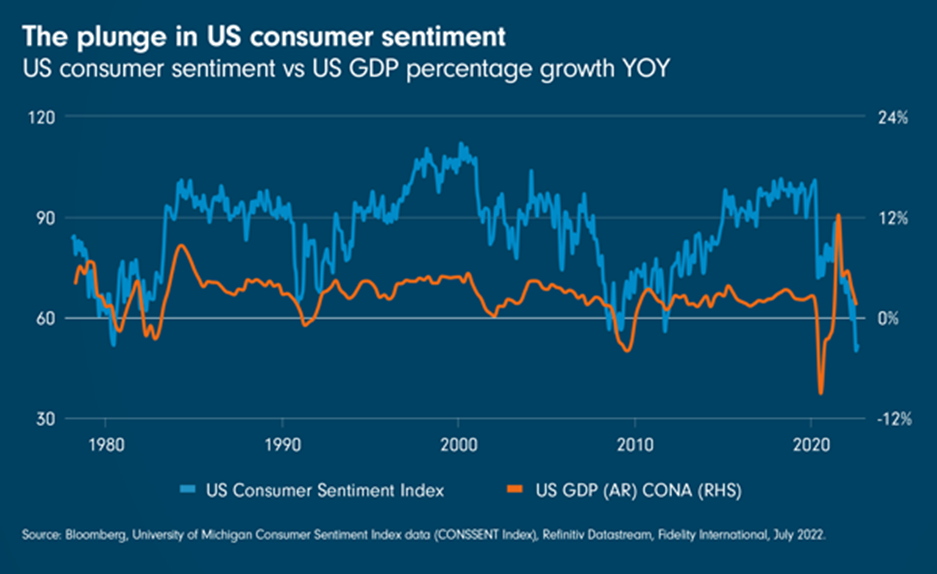

In recent months, consumer demand and spending dynamics have started to shift because of high inflation. As this week’s Chart Room shows, US consumer sentiment readings are at the lowest level since records began and indicate softer future spending patterns.

Weakening sentiment is affecting consumer behaviour. Shoppers have begun switching from more expensive brands to cheaper ones, or from branded goods to private-labelled ones. They have also been delaying large purchases such as houses, vehicles, and large durable goods.

Moreover, many consumers are digging into their savings [1] to manage higher costs of living, as seen in aggregate household savings, which have retreated to pre-pandemic levels. Housing affordability is deteriorating and there is also evidence of increased sub-prime defaults in autos.

The consumer pullback isn’t just a response to broad inflation increases, but also to the type of components in the index have seen their prices rise. As we discussed in another recent Chart Room, US Consumer Price Index (CPI) inflation is broadening out over a wider basket of goods. Twelve months ago, inflation had been characterised by one-off shocks (port closures, for example) pushing the price of certain goods, like used cars and trucks, very high. Now, even as shelter and healthcare prices may be reaching their peaks, a broader range of goods are seeing their prices rise. This will increase the pressure on households, and could contribute to a stickier kind of inflation.

This stickier price inflation, coupled with these recent bearish consumer signals, suggest that there is likely to be further risks ahead for US growth.

Source: [1] Pantheon Macroeconomics, The Weekly U.S. Economic Monitor, July 18, 2022