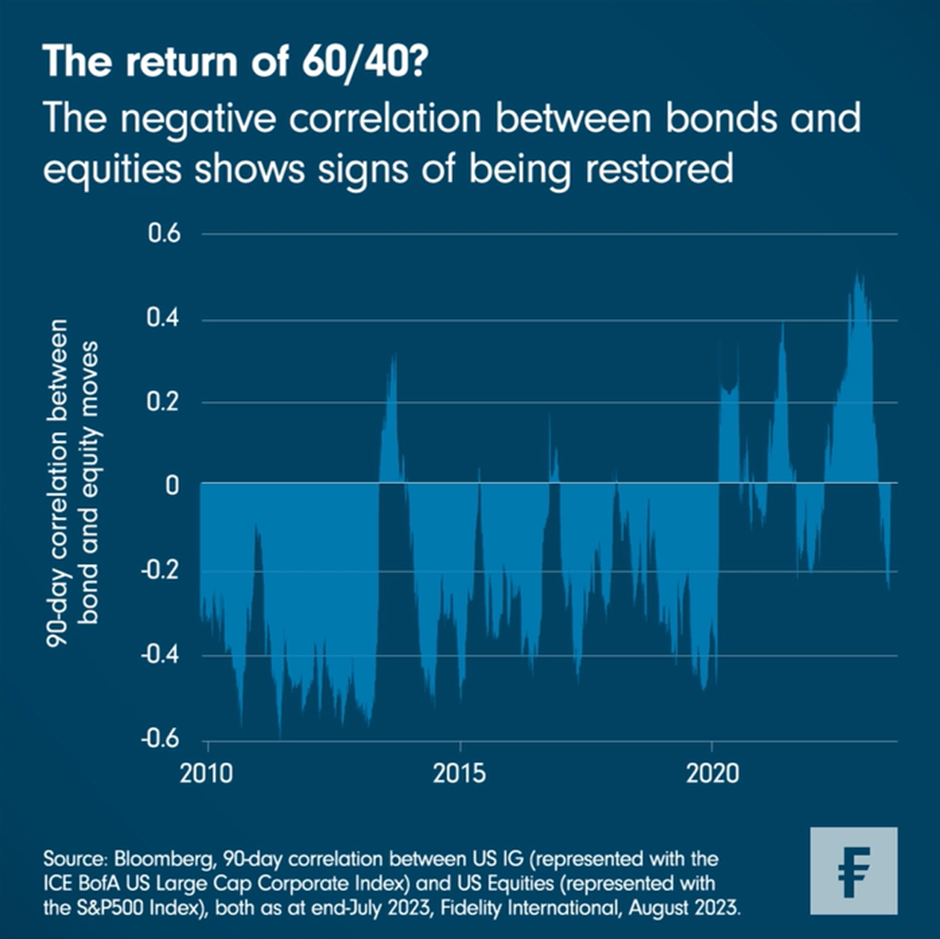

After getting upended for much of Covid era, the historically negative correlation between bonds and equities is showing signs of being restored, reviving notions of the traditional 60/40 portfolio.

This week’s Chart Room may come as a welcome sight to investors who pine for the way things used to be - at least when it comes to traditional notions of portfolio construction. The 90-day correlation between US equities and investment grade bonds, which had turned positive after the outbreak of Covid, is showing signs that it might be heading back towards negative territory. That traditionally negative correlation is a key part of the basis for the fabled 60/40 portfolio rule-of-thumb (60 per cent equities, 40 per cent bonds), which held that investors could reasonably expect positive bond returns to mitigate a bad period for equities.

This isn’t the first time in the post-Covid era when equities and bonds resumed moving in opposite directions, but previous bouts of “normalcy” proved fleeting. Still, there are good grounds for believing the current move could prove stickier. The interest rate hiking cycle, which has been a headwind for fixed income, looks to be drawing to a close. The more it appears we are at or close to terminal rates, the more confident investors are likely to feel about taking advantage of investment grade bond yields, whose average yield-to-maturity, at around 5.5 per cent, is in the 97th percentile when looked at across the last ten years.

Elsewhere, although US stocks have had a good year so far, valuations are beginning to look stretched. Price-to-earnings ratios well north of 20 are pricing in a Goldilocks-like soft-landing scenario, leaving equities vulnerable to any less benign macroeconomic outcome. A large portion of this year’s equity rally can also be attributed to companies that have benefited from the AI hype or from fiscal spending programmes such as the CHIPS Act. The debt of these companies represents a relatively small part of bond indices, and already trades at relatively tight valuations. Credit, unlike equities, has an asymmetric return profile and a ceiling on how high it can rally, while some of the hottest tech stocks have more than doubled this year.

Even if recession has only been postponed and not avoided, we expect equity investors will be on the lookout for portfolio diversifiers. Since bond indices are composed primarily of issuers from more traditional industries, we expect they will have a lower correlation with equity markets in the event of a recession or market turmoil. That means it’s probably not a bad time for bonds to reprise their supporting role as (slightly less than) one half of the famous 60/40 duo.