Signs are emerging that European real estate may have reached a bottom and is about to embark on a period of growth. But the next cycle is likely to be very different. Here’s why.

The European real estate market may have the turning circle of an oil tanker, focused as it is on long-term investments. But while the movement might be unwieldy and slow, you can still spot the shift in direction.

The latest data reinforces our view that we are close to - if not already at - the bottom of the market, with prices stabilising and potentially on the cusp of turning positive.

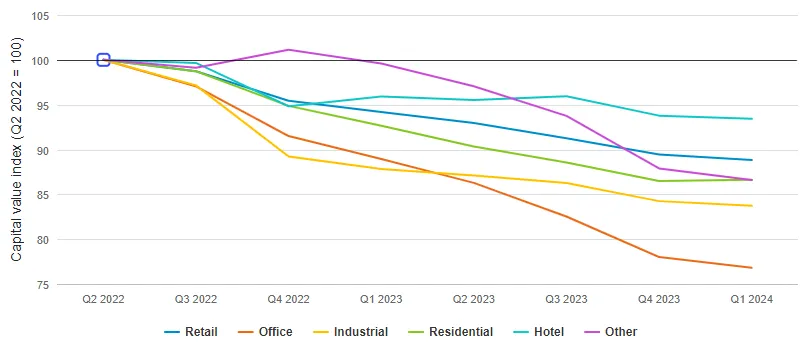

Pan-European Capital Value Growth Index - all assets

Source: MSCI Pan-European Property Funds Index - All balanced funds; Fidelity International, June 2024

Valuations across European industrial, retail, and office properties all experienced their shallowest quarter-on-quarter declines since April 2022.

The value of residential buildings returned to positive growth. It might only have been an increase of 0.2 per cent, but it comes after a fall of more than 13 per cent in two years.

Looking at the overall performance of the European real estate market, positive incomes exceeded the negative capital growth, meaning that returns at the asset level were positive for the first time since 2022.1

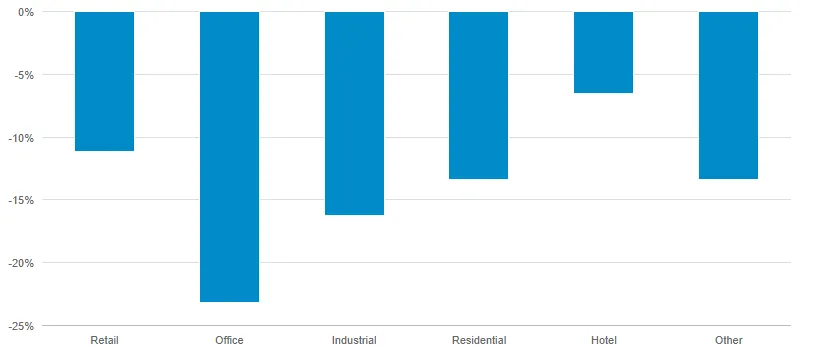

Total change in value since Q2 202 - Pan-European core real estate

Source: MSCI Pan-European Property Funds Index - All balanced funds; Fidelity International, June 2024

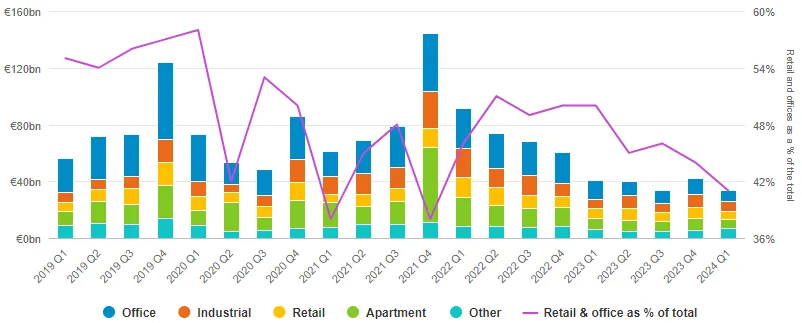

The latest figures cover deals completed in the first few months of the year, most of which will have been negotiated in the second half of 2023. So while dealmaking in the first quarter of 2024 was at one of the lowest levels of the last decade,2 the lag in the data means soft signals are even more important for monitoring current market sentiment. The good news is we’re already seeing signs of increasing activity.

Pan-European investment volumes by asset

Includes property or portfolio sales $10 million or greater. CPPI at $2.5 million or greater. Price floor selections do not apply to Hedonic data. Source: MSCI Pan-European Property Funds Index - All balanced funds; Fidelity International, June 2024

One broker report suggests the number of UK offices on the market actually grew in the first half of the year.3 The UK is typically a bellwether for the rest of Europe, and we believe the lag between the two markets is shortening, meaning the uplift in office space sales could be repeated across the continent relatively soon.

Anecdotes support the view that this uptick is already underway. Agents and lawyers are telling us that sellers are now approaching investors with off-market deals. Although it’s impossible to verify the volume of these private transactions, such a resurgence would illustrate sellers’ belief that appetite for their assets is improving. A pick-up in investment activity should soon follow.

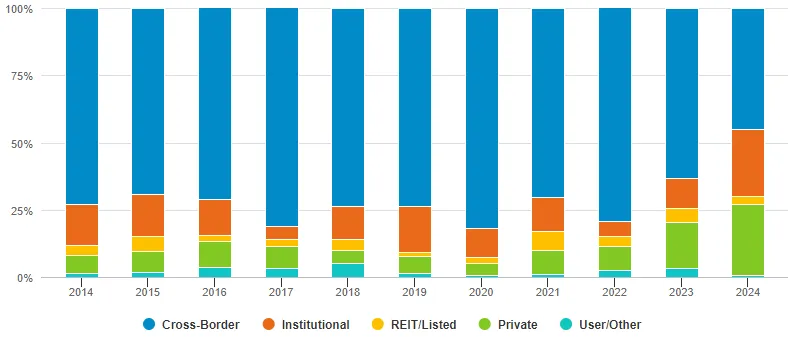

The buyer profile seems to be becoming more local too. The London market is traditionally dominated by overseas investors, and while one or two deals can skew the data of a thinly traded market, the numbers show domestic players are taking a larger role.

Buyer composition London market

2024 data to June 26. Source: MSCI Real Capital Analytics; Fidelity International, June 2024

The biggest factor supporting our expectation of a rebound is the rate move announced by the European Central Bank (ECB) in early June. While a cut of 25 basis points is unlikely to significantly reduce borrowers’ debt costs, the change in policy is more about signalling a direction of travel by the central bank, which in turn will boost investors’ confidence to make new deals. We expect to start seeing a change in investor momentum in the third and fourth quarter as a result of the ECB’s cut.

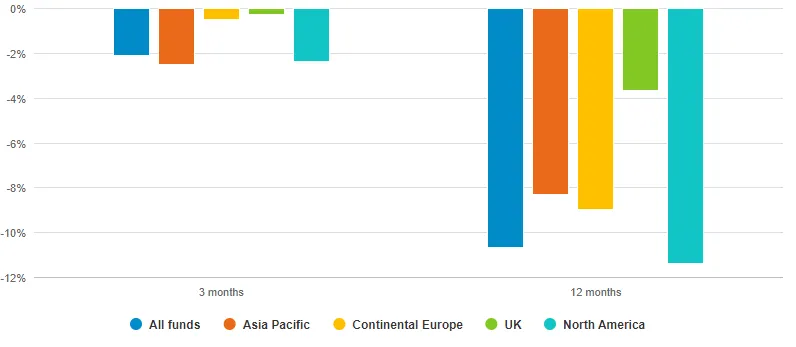

A global divergence

While the outlook in Europe is strengthening, there are fewer reasons to be so optimistic about the US market. Although we anticipate the Fed will soon track the ECB more closely, the differences between the two markets run deeper. The recovery of US real estate remains far behind its European peer despite the strong macroeconomic environment across the Atlantic.

Global net total returns

To March 2024. Source: MSCI Real Estate Index; Fidelity International, June 2024

US repricing is slower than in Europe, with capital values continuing to fall, driven by poor sentiment around office buildings. We expect this to be a theme for much of the rest of the year as headlines about the sluggish return to the workplace dominate. The perception could drag the European office sector down too, suppressing values in a lower-for-longer scenario, although we believe that the underlying structures of these two regional markets are fundamentally distinct.

Asia, on the other hand, offers a different challenge to investors. Here, sentiment has been far more robust, boosting valuations, but it means fewer opportunities to find nuggets of value as with the mispriced assets of Europe and the US. However, mature markets such as Australia, Japan, South Korea, and Singapore continue to offer a low volatility option and a varied pricing dynamic for buyers.

Rents will drive this cycle

One great benefit of real estate’s tanker-like reaction speeds is that it’s almost impervious to short-term volatility. Long-term trends are the thing to watch. While the European market should start to benefit from an edging down in interest rates, the extraordinary period of zero interest rate policy that followed the Global Financial Crisis is unlikely to be repeated. So while performance in the last cycle was driven by yield compression in that low rate environment, we believe returns in the next will be driven by rental growth.

From a core investment perspective, this means gauging where there’s likely to be long-term interest from tenants. For example, while the residential market still looks fairly expensive in yield terms, we anticipate strong rental growth in Europe because of the demographic shift taking place across the region. The population on the continent may be falling, but as it ages the number of households grows to accommodate more elderly, single-person residences. This should support residential rental demand in the long term. It also suggests benefits for sectors such as life-sciences real estate.

A less encouraging sector is retail, which has been through its own dramatic evolution over the past ten years as shoppers moved online. In many markets - Northern Europe in particular - there is just too much vacant retail space to prompt investors’ interest. Bucking this trend are assets in specific locations with compelling stories where buyers are themselves willing to manage tenants and the shorter leases they’re now after.

But the greatest shift witnessed in the European market over the last cycle has been the increased focus on sustainability. With deadlines for emissions targets rapidly approaching, the green credentials of all types of buildings have become the number one consideration for both tenants and investors. Green premiums are now prevalent and are likely to be the single most important trait of the new investment era.

Sources:

1. According to data from the MSCI Global Quarterly Property Fund Index for Q1 2024.

2. At €33.47 billion, the quarterly volume for European investment activity across all sectors was the eleventh lowest since Q 2007.

3. “UK Owners Hoist ‘For Sale’ Signs Over Office Buildings: Volume of Office Buildings Up for Sale Jumps to a Six-Year High”, CoStar, June 2024