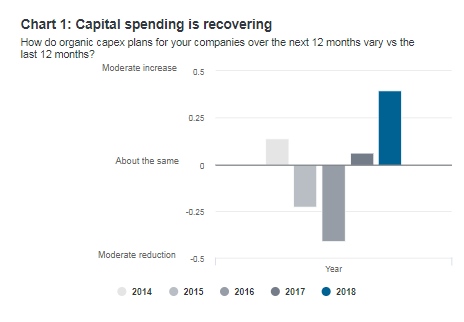

For the first time in five years, our analysts expect capital spending to grow in every region and across all sectors, indicating that companies are finally confident about the strength of demand. One of our key findings last year was that the long down-cycle in capex appeared to be bottoming out. The actual data for 2017 bore this out.

With corporate fundamentals including capital returns seen to be improving everywhere in 2018, our analysts expect CEOs to be more disposed to spend on adding capacity, deepening digitisation or embarking on the much-delayed renovation of plant and machinery. Could this herald the long awaited recovery in productivity?

Source: Fidelity Analyst Survey 2018

Source: Fidelity Analyst Survey 2018

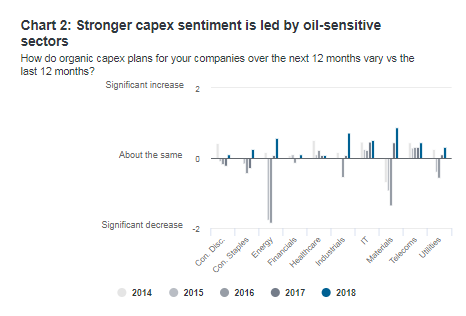

Leading the recovery in capex sentiment are energy, industrials, and materials, indicating that some of it may be cyclical and related to oil and other commodity prices. These sectors are still catching up on investment axed during the plunge in the oil price from late 2014 to early 2016, when profit margins collapsed for many companies.

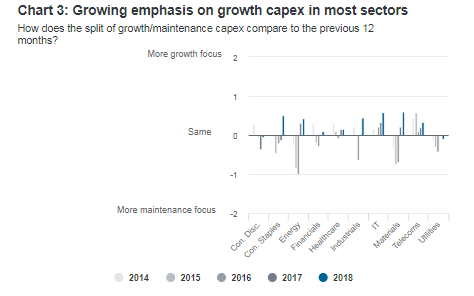

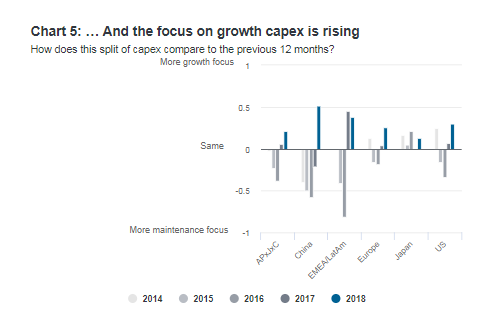

The survey findings indicate capital spending will be roughly evenly split between investment in growth and in spending on maintenance and replacement of worn-out equipment. This equal split implies a noticeably larger emphasis on growth capex than last year– an encouraging sign for the recovery of productivity and the growth potential of many economies, following years of under-investment and low productivity growth.

Almost all sectors show this increasing tilt towards growth spending compared to last year. Only in utilities and consumer discretionary is the emphasis on maintenance spending still rising.

Source: Fidelity Analyst Survey 2018

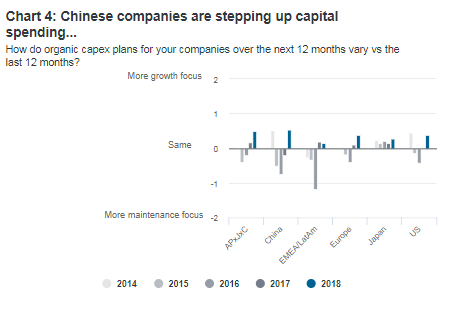

Strong expectations of increased capex in China

While our analysts anticipate a moderate increase globally in capex in 2018, the swing from 2017 is particularly striking in China and in the US, where expectations for capital spending last year were flat or slightly negative. European companies are catching up with their US counterparts and now also looking to step up investment as demand finally firms.

In China, capex sentiment is at its strongest since 2014, and our analysts say companies are investing more or earlier than expected in certain industries, including IT.

Source: Fidelity Analyst Survey 2018

Source: Fidelity Analyst Survey 2018

Chinese government policies, including supply side reforms and a certain easing of credit restrictions, are encouraging companies to retool and invest for growth. Another key driver is the clampdown on polluting industries. Stricter environmental controls have forced the closure of small, inefficient or obsolete plants. The new regulations have also required the energy, materials and industrial sectors to invest in cleaner technologies. Many steel plants, for example, are replacing old blast furnaces with electric ones. Our analysts expect the renewal of China’s manufacturing base to last another one to three years.

This big industry clean up, with its attendant dip in production, has led to record prices in China for some basic manufactured goods, including paper, cement and glass, where our analysts report prices are at their second-highest levels in history. And while high prices may last only until new capacity is put in place, they have also provided the necessary liquidity for companies to refurbish and invest in new technologies.

The strong resurgence of capital expenditure in China is also linked to where each sector is in the cycle. China’s heavily-indebted construction groups, for example, had delayed capital expenditure in recent years to get leverage under control. Since late 2016, however, our analysts report that balance sheets and cash flows have recovered sufficiently to persuade builders to replace old equipment, particularly in view of the government’s big infrastructure push in the west.

This has had a knock-on effect on the construction industry’s supply chain. Demand for excavators, for example, began recovering in late 2016. The mining industry has taken a little longer to retool, but once coal prices began rising, companies started to replace mining equipment in 2017, and our analysts expect this trend to continue in 2018.

Not everyone has benefited from higher commodity prices. For mid-stream manufacturers, margins have been squeezed because they have not been able to pass on the cost of higher commodity prices to consumers. Our analysts believe this might be a reason why the authorities are allowing capacity additions to basic industries – to reduce price pressures overall.

Increased US spending linked to capacity constraints

In 2017 capex in the US was in a holding pattern, with about half of analysts reporting no change in capex expectations in their sectors and the remainder evenly split between rising and falling capex expectations. This year our findings indicate a moderate rise in capital spending, equally balanced between growth and maintenance.

The strong economy is showing signs of capacity constraints, which may be one of the factors driving improved sentiment for capital spending in 2018. At the start of the year, for example, orders from trucking companies for new big rigs (large trucks with attached trailers) stood at their highest level in nearly 12 years. Logistics groups were responding to a surge in freight rates as companies fought for shipping space in a tight market.

Recent large cuts in the corporate tax rate, and changes in cash repatriation laws, may also have improved the outlook for capital spending. Our analysts expect companies to repatriate significant funds currently held abroad and spend some of this on retooling and digitising their operations.

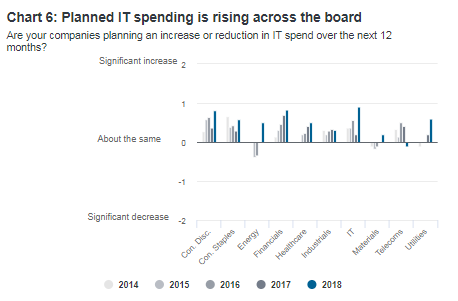

IT capex for growth continues to be vital for the whole economy

Capital spending in the IT sector is in many ways a harbinger of future economic growth all round. IT companies tend to ramp up their capex only when they anticipate greater demand from their customers. And demand remains strong because digitisation continues to make inroads across all industries. Even traditional manufacturing businesses and utilities have had to increase the tech component of their capital spend.

Analysts also say that cybersecurity now tops the list of environmental/social concerns among companies in financials, technology and telecoms following attacks that targeted national health services, telecommunications groups, banks and many other sectors last year. But beefing up cybersecurity does not come cheap, and will require significant investment.

IT companies have increasingly been tilting their capex towards growth, much more so than in other sectors. One reason our analysts believe the trend will continue in 2018 is that the industry – which has disrupted so many sectors of the economy – is itself also the subject of disruption. The shift from data centres to cloud computing; the race to find applications for Artificial Intelligence (AI) and the Internet of Things; and growing corporate demand for data analytics, are keeping the industry on its toes.

These trends are as relevant to China as they are to Silicon Valley. Our analysts expect Chinese IT companies to step up investment in cloud capacity, data centres and AI this year. Even the semiconductor industry in China is in a big drive to close the technology gap with its peers in Europe and the US.

Source: Fidelity Analyst Survey 2018