The latest resumption of hostilities in the Persian Gulf, amid what is supposed to be a ceasefire, is yet another reminder of how uncertain the situation in the Middle East remains. But while nobody can say when or how the conflict will end, we can predict with some confidence where its inflationary impacts will land hardest over the next few months.

That’s because we are yet to see the full effects of the first four months of war, which are still working their way through the global economy.

“There is likely a negative delayed impact from increased energy costs and fertilisers that is yet to impact my sector,” says Europe-focused retail sector analyst Michael Gaynor, providing one example of the lagged inflationary impulse. “Many companies have hedged almost all their energy exposure for this year as they learned from the last inflationary episode in 2022, but some are still exposed more than others. Supply chains similarly have been stretched, with many having to pay more for air freight rather that to travel on sea.”

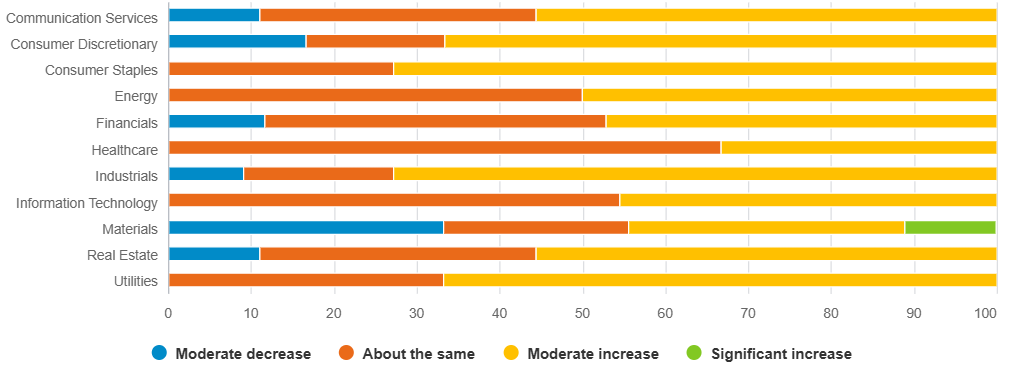

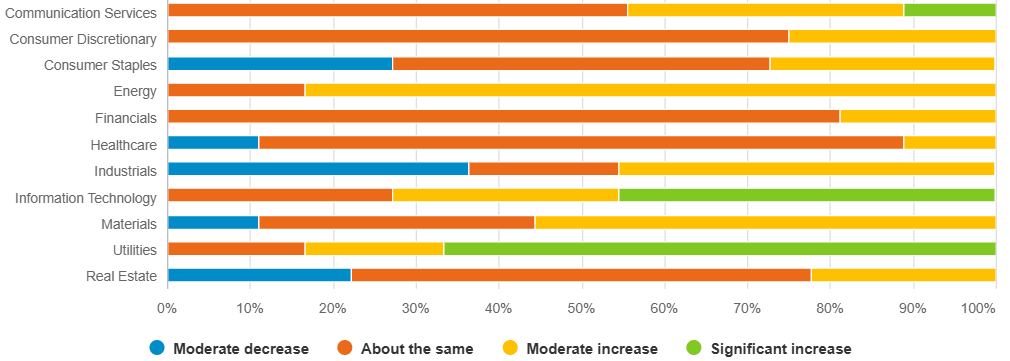

Just over half (55 per cent) of respondents to Fidelity’s latest Analyst Survey say they expect inflationary pressures in the cost bases of the companies they cover will increase over the next 12 months due to the Middle East conflict. Consumer sector, industrials, and utilities appear especially exposed, although there are expectations for increased input costs in every sector and region.

Chart 1: Iran conflict cost impacts are widespread

Percentage of analysts

Source: Fidelity International Analyst Survey, June 2026.

Question: ‘How, if at all, do you expect inflationary pressures within your companies’ cost bases to change over the next 12 months due to the Middle East conflict?’ Chart shows percentage of analysts covering each sector.

“Clothing retailers and Coke bottlers in Brazil are pointing to higher raw material costs from commodities linked to oil prices, as well as a broader increase in freight costs,” says Addington Jerahuni, a consumer staples analyst, illustrating the global nature of the impact.

“Clothing retailers have inventory cover for a few months,” Jerahuni adds, “which means the effect will be felt as they cycle into newer inventories. Coke bottlers and beer brewers are hedged for 2026, so they have not seen an immediate impact from higher aluminium and PET [plastic] costs. However, 2027 hedges are starting from a higher price level, which will affect next year.”

Transmission channels: interest rates and consumer sentiment

Alongside the first-order effects of higher raw materials prices is their potential knock-on effects, which spread the impact across sectors.

Interest rates are one channel through which inflationary pressures might affect business activity.

Eric Zhu, who covers China’s auto market, notes that while the country’s temporary oil shortage accelerates the penetration of ‘new energy vehicles’ like electric cars and hybrids, “higher interest rates are harmful for overall consumption.”

Zhu is far from alone among Fidelity’s analysts in contemplating the prospect of inflation pressures leading to higher interest rates.

“The Middle East conflict is primarily affecting Australian real estate through higher inflation and interest rates,” says equity analyst James van de Graaff. “The sectors bearing the brunt are the residential developers, which are now grappling with higher interest rates undermining demand, and construction cost inflation impacting build costs.”

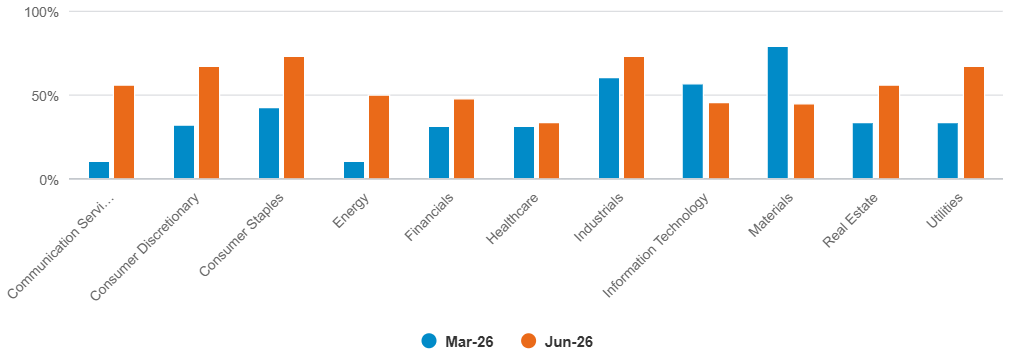

Another potential transmission channel is consumer sentiment. As Chart 2 shows, consumer-facing sectors have seen a notable jump in the proportion of analysts expecting higher cost inflation, compared to our previous Analyst Survey three months earlier.

Fidelity International’s analysts reveal which sectors are most exposed to rising costs caused by the ongoing Middle East conflict.

Chart 2: Inflation surprises

Percentage of analysts who expect increased inflationary pressures in the next 12 months

Source: Fidelity International Analyst Survey, June 2026. Question: (June) ‘How, if at all, do you expect inflationary pressures within your companies’ cost bases to change over the next 12 months due to the Middle East conflict?’/Question: (March) ‘How, if at all, do you expect inflationary pressures within your companies’ cost bases to change over the next 12 months?’

However, several analysts covering those sectors still appear relaxed about the longer-term prospects.

“Early in the conflict I was afraid of a more meaningful increase in costs, and while there was a bump in costs during the initial months of the war, I’m no longer expecting to see a material impact across my coverage over a 12-month horizon,” says consumer discretionary analyst Robbie Glatt, citing the fall in the oil price since the early weeks of the war.

Chase Bethel, who covers consumer staples businesses in North America, notes the potential for the Middle East conflict to weigh on US consumers: “Rising gas prices are a headwind to disposable income, stretching low-income consumers’ ability to spend, while also having a negative impact on consumer sentiment.”

But it seems businesses have so far been able to insulate their customers: “Companies have indicated that cost inflation to date has been manageable. Grocers and food retailers are generally pushing back on attempts by suppliers to pass on fuel surcharges,” he says.

Andrew Hall, another North America-focused analyst covering food retail, adds that the Middle East conflict has had “no impact on the major costs in my sector beyond food prices, where the industry has a strong track record of passing on inflation to consumers.”

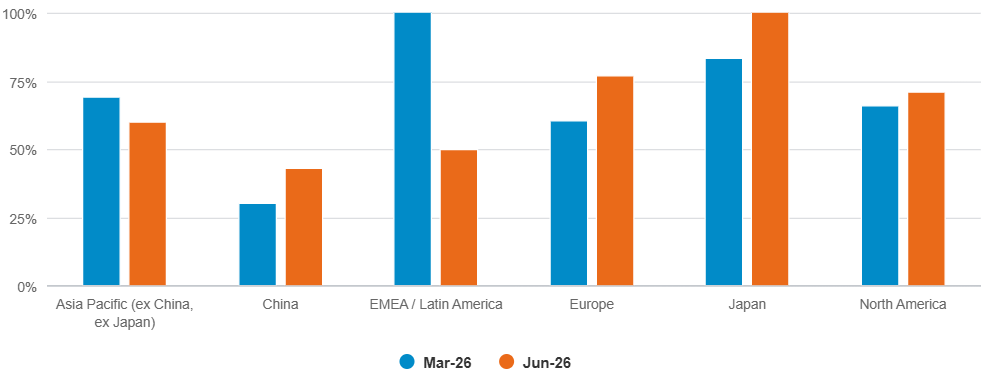

Revenue and earnings expectations are holding up

Elsewhere in the survey, analysts’ responses paint a broadly positive picture for the months ahead. Two-thirds of the research team expect their companies to show revenue growth over the next 12 months, a finding that is perhaps itself reflective of higher inflation expectations.

Chart 3: Revenues resilient

Percentage of analysts expecting an increased revenues over the next 12 months

Source: Fidelity International Analyst Survey, June 2026. Question: ‘What are your expectations for revenue growth over the next 12 months?' Chart shows percentage of analysts expecting an increase.

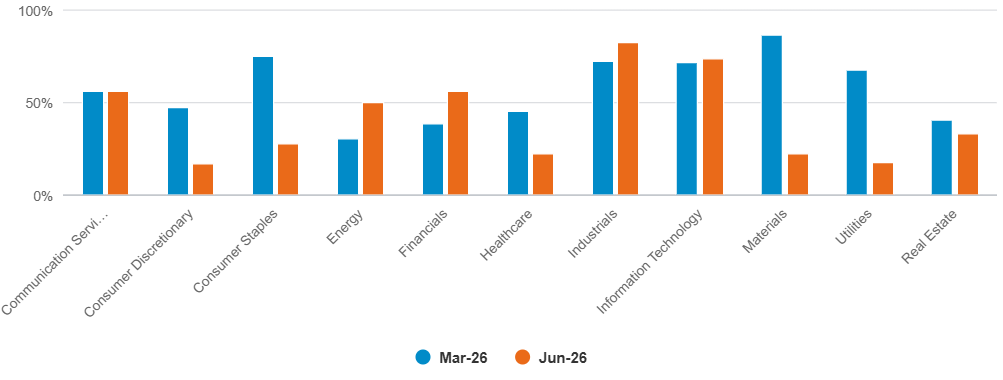

Earnings expectations too appear resilient. Only 25 per cent of analysts expect to see earnings at their companies fall in the next 12 months, compared with 43 per cent who forecast an increase.

The sector-by-sector story is mixed, however, with fewer analysts expecting increased earnings for consumer, materials, and utilities companies than in the previous survey, while industrials, information technology, energy, and financials look more resilient.

Chart 4: Earnings impact

Percentage of analysts expecting increased earnings over the next 12 months

Source: Fidelity International Analyst Survey, June 2026. Question: ‘What are your expectations for EBITDA margins over the next 12 months?' Chart shows percentage of analysts expecting an increase.

Compare that with capital expenditure. Responses to the survey’s regular question on capex expectations show clearly the effects of the AI infrastructure build-out. Information technology and utilities stand out, with analysts pointing to greater investment in datacentres, power generation, grid capacity, and the hardware needed to support new AI workloads.

Chart 5: AI capex is another inflation driver

Percentage of analysts

Source: Fidelity International Analyst Survey, June 2026. Question: ‘What are your expectations for capex over the next 12 months?' Chart shows percentage of analysts covering each sector.

Evan Delaney, a North America communications services analyst, says that for some telecom companies the bigger inflationary driver is not energy, but “the AI/hyperscaler capex boom”, which has increased the price of networking equipment and hardware.

Utilities analyst Srishti Sinha makes a similar point from the power side, noting that higher labour costs are being driven by the “datacentre buildout driving a spike in demand”.

This complicates the inflation story. The Middle East conflict has revived concerns around energy prices, input costs, freight costs, and interest rates that are familiar from the early years of this decade. But a separate investment cycle is still supporting demand for power, grid equipment, commodities, construction labour, and specialist components.

Regardless of what happens in the Gulf, the inflationary impulse from AI capex looks set to persist. For investors, the important question will therefore continue to be which companies have enough pricing power, balance-sheet strength, or structural demand to absorb rising costs.