The global investment backdrop is undergoing a structural shift. Geoeconomic fragmentation characterised by intensifying strategic rivalry and more interventionist fiscal policy is reshaping capital flows and market dynamics.

In this environment, macroeconomic outcomes are less predictable and market regimes can change more abruptly. Fiscal expansion, higher inflation, and evolving central bank reaction functions complicate the outlook for both equities and bonds. At the same time, global equity benchmarks have become increasingly concentrated in a narrow group of US mega-cap companies, leaving portfolios exposed to concentration and thematic risks.

After several years where it felt like US equities were the only game in town, the benefits of geographic diversification are back in fashion as a way of embedding resilience through differentiated regional exposures with idiosyncratic economic drivers. In this context, Japan stands out as a market offering both the diversification benefits of having increasingly distinct drivers from the US cycle and the return potential of powerful structural tailwinds that are reshaping its equity story.

We believe there are three factors driving the positive outlook for Japanese equities: an improving macro backdrop, a supportive policy environment, and changing corporate attitudes.

Improving macro backdrop

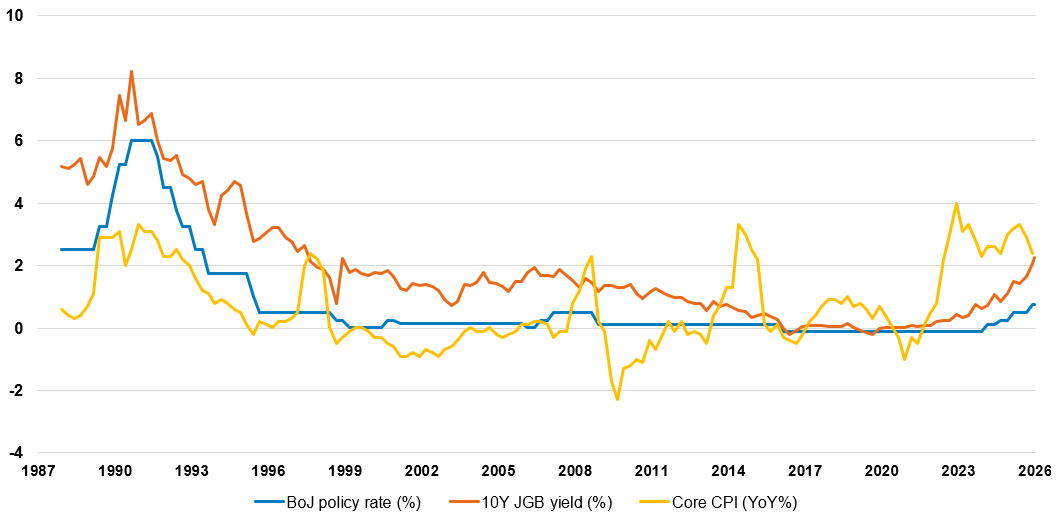

For decades, Japan was synonymous with stagnation and corporate conservatism. Now, Japan has moved decisively into a period of mild, durable inflation. Companies are regaining pricing power and raising wages, and inflation is increasingly embedded in expectations rather than driven purely by external cost pressures. This marks a fundamental break from the deflationary psychology that defined the past thirty years.

Source: Fidelity international, Bloomberg, February 2026.

The Bank of Japan has begun a cautious process of policy normalisation, gradually lifting rates while maintaining an overall accommodative stance. This measured approach supports financial stability while reinforcing confidence that reflation is durable rather than transitory.

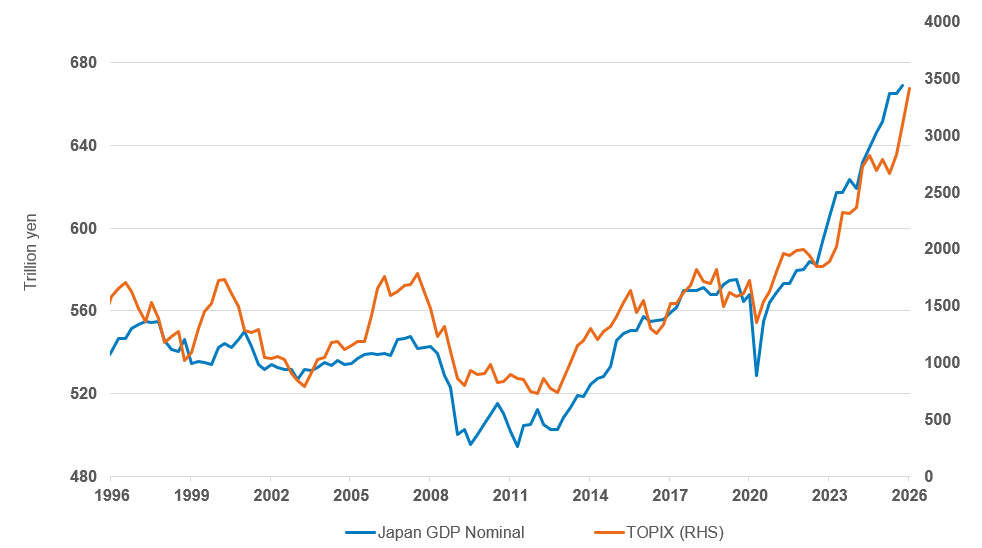

The shift from deflation to reflation has important implications for equities. Nominal GDP growth is improving, earnings quality is strengthening and balance sheets are being deployed more productively. Instead of hoarding cash, companies are increasingly investing in capex, research and development, strategic acquisitions and returning excess to shareholders. In a global context where inflation volatility remains elevated, Japan’s controlled reflation offers a relatively stable nominal growth backdrop.

Reflating economy is a tailwind for Japanese equities

Past performance is not a reliable indicator of future returns. Source: Fidelity international, LSEG Workspace, February 2026.

Supportive policy environment

Japan’s policy environment has also become clearer. A strong electoral mandate has reduced near-term political uncertainty and increased the likelihood of targeted fiscal support. The government’s focus includes bolstering strategic industries such as advanced manufacturing, digitalisation, energy security, defence and infrastructure.

These priorities align with broader global themes associated with geoeconomic fragmentation, including supply chain resilience, reindustrialisation, and technological sovereignty. As countries compete for leadership in critical industries, Japanese companies positioned within these strategic areas stand to benefit from sustained public and private investment.

Changing corporate attitudes

Perhaps the most powerful driver of Japan’s equity re-rating is the sustained momentum behind corporate governance reform.

The Tokyo Stock Exchange has pushed companies trading below book value to improve capital efficiency and shareholder alignment. Cross-shareholdings are being unwound, parent–subsidiary listings are being rationalised, and management teams are increasingly focused on return on equity. Shareholder distributions have risen sharply. Dividend payout ratios are increasing and share buybacks have become a more prominent and flexible tool for balance sheet optimisation.

As reforms deepen, average return on equity is projected to rise meaningfully over the coming years, narrowing Japan’s long-standing valuation discount relative to global peers. This represents a structural improvement in capital discipline and corporate accountability, reinforcing the case for a sustained market re-rating.

How we are positioning in this environment

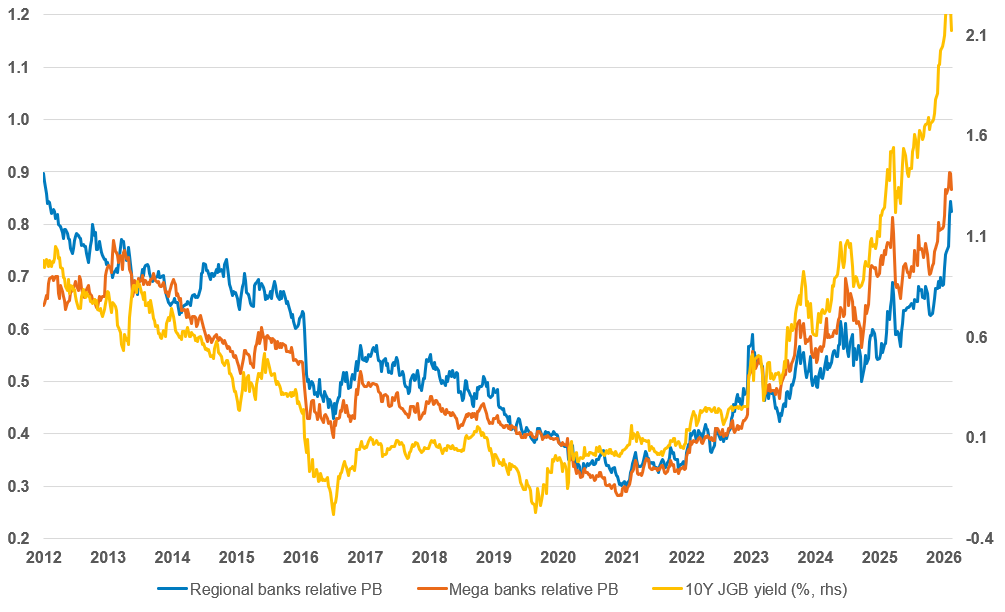

Against this backdrop, our focus is on investment opportunities aligned with Japan’s structural and cyclical transition at attractive valuations. We favour companies benefiting from domestic structural drivers, alongside selective exposure to global cyclicals where the risk-reward profile is attractive. Core exposures for us are currently concentrated in financials, construction, and industrials.

Financials are emerging as clear beneficiaries of reflation and gradual rate normalisation. Corporate demand for investment is driving loan growth, while improving net interest margins support profitability. In addition, governance reform is reinforcing more disciplined capital allocation, enhancing dividends and buybacks. For example, regional lender Yokohama Financial Group is well placed to benefit from higher interest rates, rising corporate activity in Japan and management’s focus on improving shareholder returns. With strong expected earnings growth and an attractive total shareholder return yield, the shares offer compelling value.

Financials are clear beneficiaries of policy normalisation

Past performance is not a reliable indicator of future returns. Source: Fidelity international, Bloomberg, February 2026.

Construction and infrastructure-related companies are experiencing expanding margins as pricing power returns. Demand for new factories, energy infrastructure, datacentres and offices is rising, supported by both private capital expenditure and government stimulus. EXEO is a leading Japanese engineering contractor. Earnings momentum is strengthening as higher-margin mobile network upgrades, fibre replacement and complex data-centre build-outs expand, improving the project mix. A solid balance sheet supports attractive shareholder returns through progressive dividends and potential buy-backs.

Industrials are benefiting from digitalisation, automation and rising demand for secure and stable energy. Demographic pressures are accelerating investment in productivity-enhancing technologies, including AI and factory automation.

Japanese equities’ place in a fragmenting world

Today’s Japan is very different from that of the past. Supported by credible policy coordination, improving capital discipline and sector-specific tailwinds, the market provides both diversification benefits and the potential for attractive long-term returns.

Even with Japan’s improving backdrop, investors should remain aware of potential policy shifts, external or geopolitical factors that could still introduce volatility. In an era defined by fragmentation and higher market uncertainty, geographic diversification can spread risk and access differentiated structural drivers. For investors looking to boost the resilience of their equity exposures in a more uncertain, multipolar world, we believe that Japanese equities offer a compelling opportunity.