The economists’ verdict is in: 2023 will be a tough year as higher prices and higher interest rates drive many economies into recession. But are they too gloomy? Fidelity’s annual Analyst Survey, polling 152 experts who cover real businesses on the ground, paints a more hopeful picture.

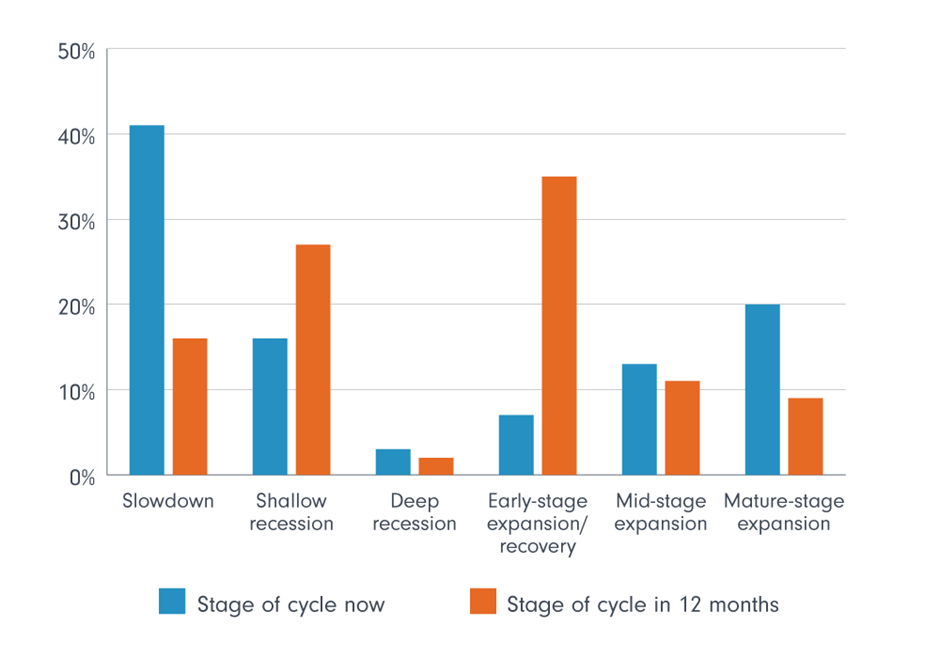

The survey, which we have been running for over a decade, consults a range of fixed income, equity, private credit, and cross asset experts who cover dozens of sub-sectors of the economy. It shows 60 per cent of analysts believe their sectors are already in a slowdown, a shallow recession or worse. Look slightly further out, however, and just over half of those analysts expect the business cycle will have turned positive again by the end of 2023. Only a handful expect to be deep in recession.

That may run contrary to the prevailing mood after a year in which the shocks delivered by Russia’s invasion of Ukraine have run parallel to the deflating of a decade of booming stock markets and cheap money. But from a wider perspective, it is in line with economic logic: as companies reach the bottom of the business cycle, they begin to think about the opportunities to come.

“As long as there isn't a Black Swan event and this is a ‘normal’ recession, I expect we will start to recover out of it in the second half of the year,” says one US consumer analyst.

Chart 1: This too shall pass

Questions: “What stage of the cycle is your sector currently in?” and “What stage of the cycle will your sector be in in 12 months’ time?” Chart shows percentage of analysts. Source: Fidelity International Analyst Survey 2023.

Hope in China’s reopening

On the ground, how is this likely to this unfold? For one thing, cost pressures, the results suggest, will peak for most sectors and regions in the first half of the year. China - assuming its reopening gamble works - will reboot, and materials, utilities and technology companies will shift back into investment mode, in part driven by the environmental transition.

Beyond the main annual survey, we also ask our analysts a smaller set of questions every month. The most recent monthly responses are a further source of optimism. The management sentiment reading, while still negative, appears to have broken a two-year downward trend, posting four straight months of improvement to January, with those analysts who cover China reporting positive sentiment among managers in both December and January.

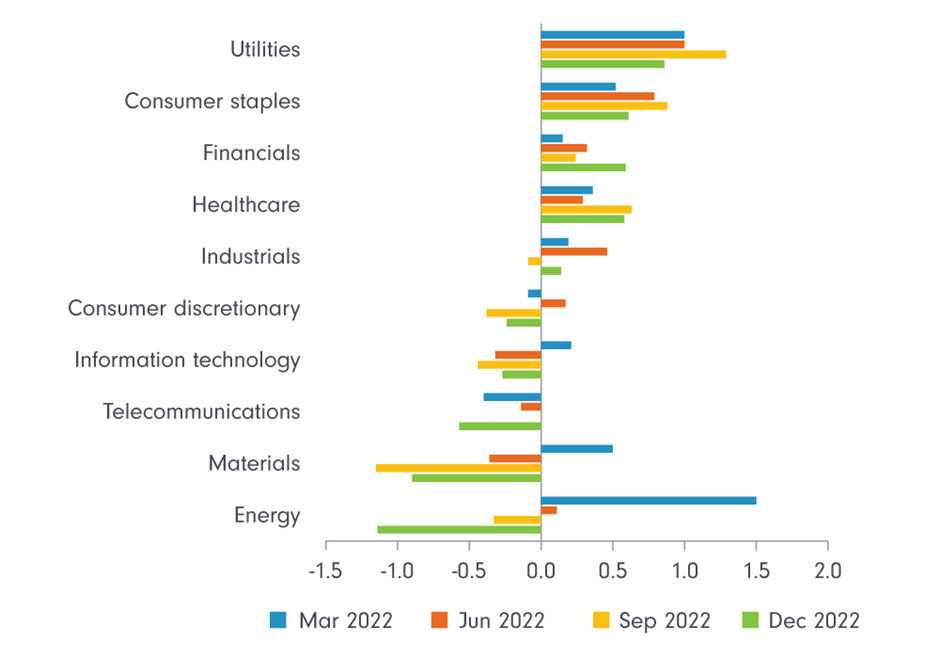

Chart 2 below suggests that half of the 10 business sectors the survey covers will see revenue grow in the next 12 months, although much of that is forecast to stem from the easing of China’s Covid controls - something that is still being closely watched.

Chart 2: Revenue growth heavily sector dependent

Question: “What are your expectations for revenue growth over the next 12 months?” Chart shows proportion of analysts expecting revenue will increase minus proportion expecting revenue will decrease. Strong positive and strong negative responses receive a double weighting. Higher values show analysts on balance expect revenue will rise. Source: Fidelity International Analyst Survey 2023.

Be prepared

Although funding costs are a worry, balance sheets look less stretched than previously. Debt is expected to grow only in two sectors: utilities, where companies are investing heavily in renewable power, and in consumer sectors already struggling with the aftermath of two years of Covid restrictions. Banks should see revenues boosted by the rise in interest rates, and others in the financial sector expect 2023 to deliver - at a minimum - an improvement on the stock and bond market slides of last year.

“While the near-term outlook is challenging, most companies in my coverage are in a much better balance sheet position than they've been historically,” says another US consumer sector analyst.

Turning to the bottom line, 74 per cent of analysts say their companies’ CEOs expect earnings to grow over the next 12 months. Anecdotally, we know inflation is playing a role, as one consumer staples analyst explains: “Food retailers benefit from inflation as they pass on supplier price increases."

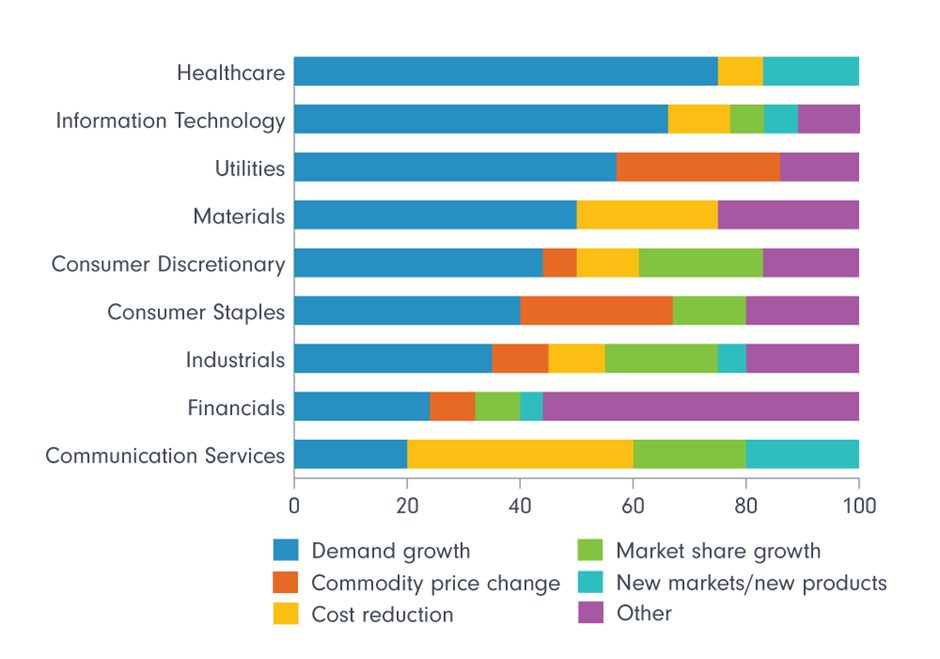

Analysts, however, also highlight other sources of expected earnings growth and the picture is illuminating: the dominant answer from those covering utilities, materials, information technology, and healthcare is that end-demand will improve.

Chart 3: Reasons to be cheerful: the biggest sources of earnings growth

“Question: Do the CEOs in your industry sector expect earnings to grow over the next 12 months?” Chart shows percentage of analysts. Source: Fidelity International Analyst Survey 2023.

The bottom-up view of the polycrisis

But in the near term, the pain to come is evident in the survey’s wide range of data points. Analysts expect a rise in debt defaults over the next 12 months. Recent growth in shareholder pay-outs will fade, while mergers & acquisitions (M&A) activity will slow, with 73 per cent of analysts saying the deals they do expect will be smaller, bolt-on acquisitions. Around three-quarters (74 per cent) say that, for now, the biggest focus for boards is holding down costs and shoring up revenues, rather than investing for growth or delivering shareholder returns.

“Companies feel very hesitant at the moment,” says a communication services sector analyst. “Bold decision making has been replaced by more of a slow build. More focus on cost cutting. Not a lot of M&A rumours.”

Geopolitical concerns, brought sharply into focus by the Russian invasion, are also growing, with the survey’s negative net reading for this topic almost doubling. Companies remain focussed on the environmental, social and governance (ESG) challenges ahead, but there is little improvement in our indicators on net zero, biodiversity and other ecological issues.

Fear for the consumer

By sector, the hardest-pressed businesses over the next year will be those dependent on consumer spending. Many companies may have partially insulated themselves from the immediate effects of rising US and European interest rates but households are already suffering. The survey shows both that businesses targeting the consumer will have the least power to raise prices over the next year and that their balance sheets are the most stretched.

Yet, as so often in the past two decades, some salvation may lie in the pace of growth in China. Answering the survey as Beijing abandoned its zero-Covid policy in December, only 8 per cent of our analysts predicted even a shallow recession in the world’s second largest economy, judging that the reopening, together with the room authorities have to support growth with policy, will succeed in rebooting growth.

It will, of course, not be a smooth ride, and those who expect a challenging year in 2023 will find plenty in our survey to support that view. Overall, however, the picture emerging is not one of perpetual gloom but also of brighter times to come.