After one of the toughest periods for quality investing in decades, many are questioning whether discipline still pays. In his latest Market Musings, Maroun Younes, Co-Portfolio Manager of the Fidelity Global Future Leaders Strategy, looks through 40 years of data to show why quality has delivered stronger returns, smoother drawdowns, and why abandoning it now may be the wrong call.

Key takeaways:

- Quality has delivered over the long term (and more smoothly): It has historically outperformed global equities by ~3% p.a., with lower volatility and better downside protection through cycles.

- Underperformance is part of the journey: Quality lags around one-third of the time, typically during early-cycle recoveries and speculative, risk-on markets.

- Discipline matters most now: The current drawdown is unusually deep and prolonged, but history suggests this is not the time to abandon quality as staying the course has been consistently rewarded.

As investors, we’ve all heard Warren Buffett advocate for buying high-quality businesses with durable competitive advantages, what he calls “economic moats.” The long-term data backs it up convincingly.

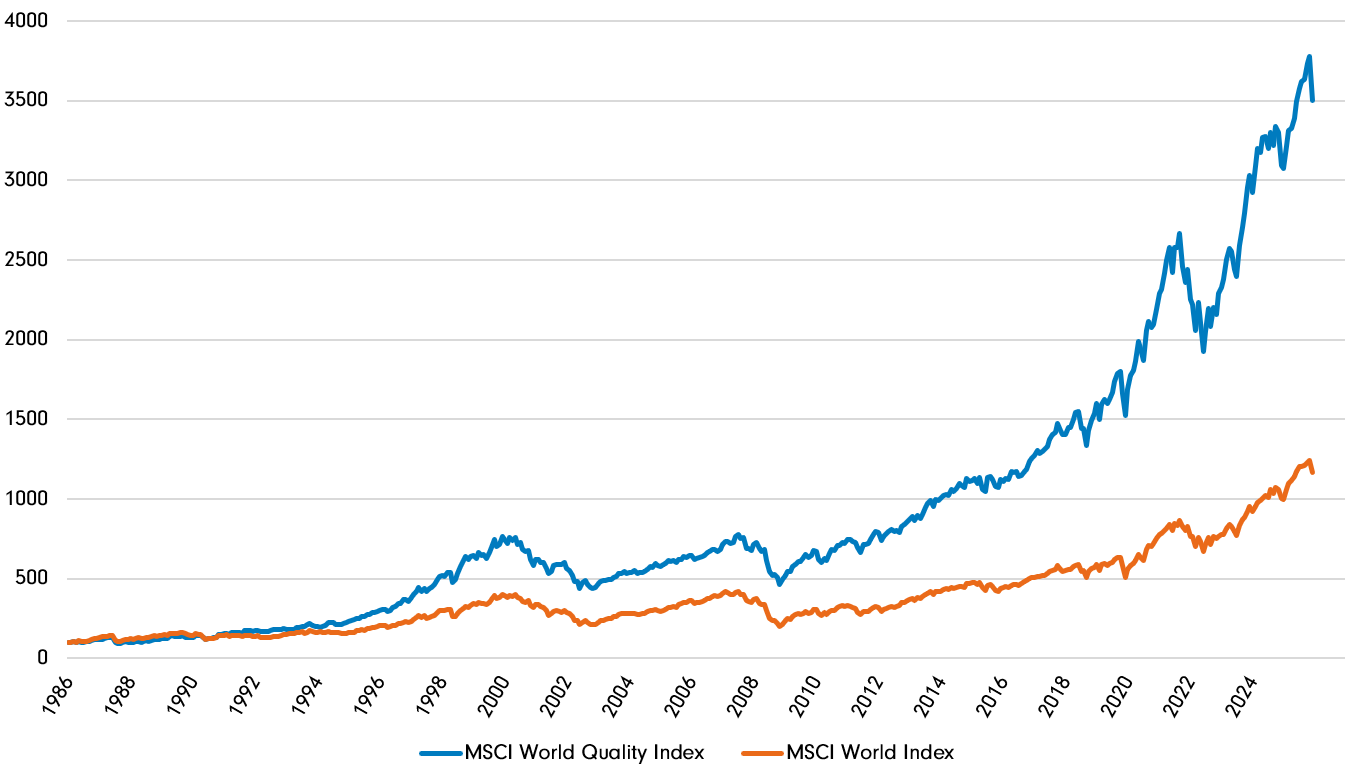

The chart below shows the MSCI World Quality Index over the past four decades. Quality, as an investment style, has outperformed the broader global equity market (MSCI World Index) by around 3% per annum (both are indexed to a base value of 100 at the start date). Compounded over time, that’s not incremental; it’s transformational. It has resulted in roughly three times the total return of the broader index.

Quality outperforms broader equity market

Source: MSCI, FactSet, FIL

What’s equally important to me is how those returns are achieved. Quality hasn’t just delivered more (roughly 3x the return). It has done so with less volatility and shallower drawdowns, particularly during periods of stress. Whether it was the early 90s recession, the dotcom collapse, the GFC or the COVID shock, significant geopolitical conflicts (notably the Ukraine and Gulf wars), and everything in between, quality businesses tended to fall less and recover more steadily.

That combination of better outcomes with a smoother path, is a powerful one, particularly for long-term capital.

Defining “quality” is harder than it looks

One of the persistent challenges with quality investing is that there’s no single, universally accepted definition for ‘quality’. Characteristics that define a quality business in the eyes of one may be different to the eyes of another.

Academics and practitioners approach it differently. Novy-Marx focused on gross profits/assets ratio1. Asness, Frazzini and Pedersen defined quality as safe (stable), profitable (margins), growing and well managed businesses (shareholder payout)2. Finally, Fama & French3 updated their famous three-factor model by adding in two new factors, Robust Minus Weak (measuring profitability) and Conservative Minus Aggressive (measuring how much firms invest).

MSCI, in constructing their Quality Index, utilise a combination of return on equity, debt to equity ratio and earnings variability, with quality companies exhibiting high returns on equity, conservative debt levels and consistent earnings profiles.

In practice, I think of quality more holistically: businesses that generate high returns on capital, reinvest sensibly, and exhibit resilience across cycles. The precise definition matters less than the consistency of characteristics.

A smoother ride

We’ve seen how the data shows clearly that quality outperforms the broader market over the long term, however it’s time to delve a bit deeper into this relationship.

In my view, one of the most underappreciated aspects of quality investing is that it comes with less variability.

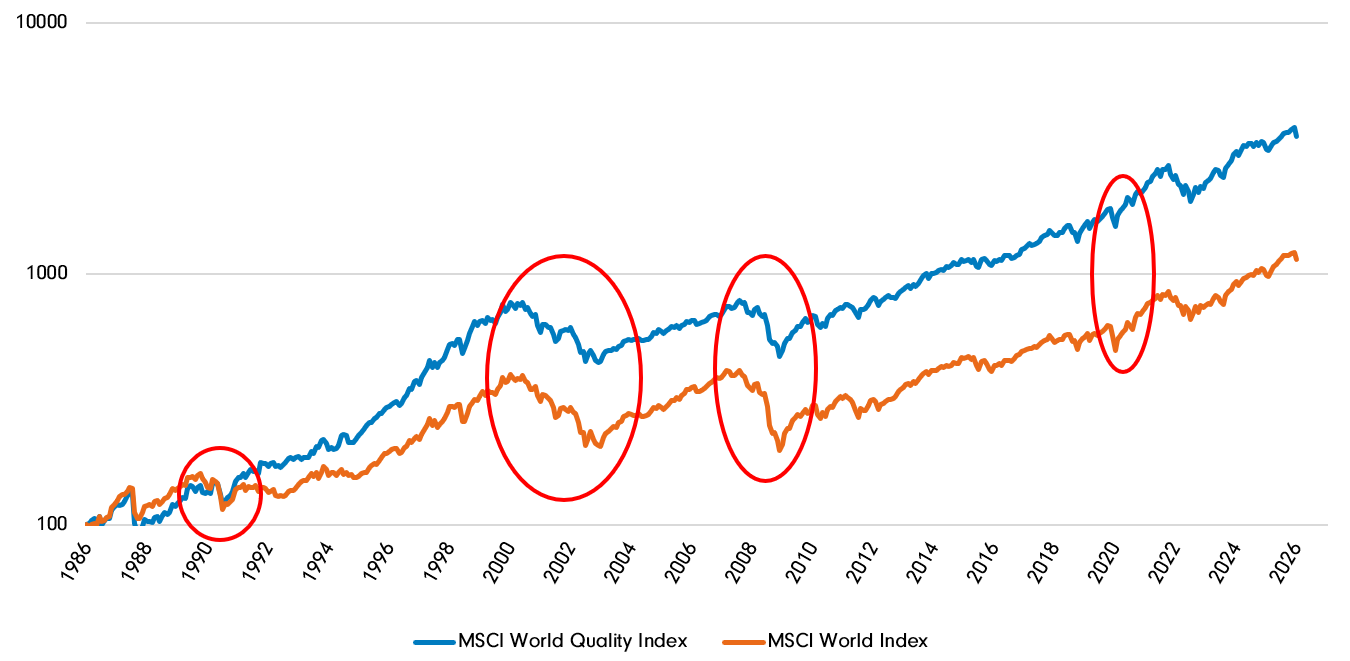

The MSCI World Quality Index has exhibited lower volatility than the broader MSCI World Index, meaning investors have historically benefited not just from stronger returns, but from a smoother journey along the way.

That smoother path is largely a function of downside protection. During periods of market stress, whether the 1990/91 recession, the dotcom collapse, the GFC, or the sharp COVID sell-off in March 2020, quality businesses have tended to fall significantly less than the broader market.

This characteristic can be easy to overlook in long-term charts, particularly when using a standard linear scale. However, when viewed on a logarithmic basis, the resilience of quality during drawdowns becomes much more apparent. The chart below highlights the four bear market episodes I previously mentioned.

Four bear market episodes

Source: MSCI, FactSet, FIL

A note of caution however, not all businesses traditionally viewed as “high quality” are immune to disruption. More recently, we’ve seen parts of the market come under pressure as investors reassess the potential impact of AI on established business models. Some of those concerns will prove justified, while others will prove to be misplaced.

For me, this reinforces an important point — quality investing isn’t about blindly buying yesterday’s winners. It requires being selective and disciplined to ensure that the businesses we own can sustain their competitive advantages and remain high quality.

The price of quality

Of course, quality doesn’t outperform all the time. In fact, there are many episodes where quality underperforms.

Looking back over the period from March 1986 to March 2026, quality has outperformed in around 60% of calendar years (24 out of 40). On a rolling 12-month basis, that rises to closer to 65%. Put differently, quality underperforms roughly one-third of the time.

I think of this as the price you pay for long-term outperformance.

These periods of underperformance are not random. They tend to fall into two broad categories.

The first is early-cycle recoveries, when growth reaccelerates and credit conditions loosen following a recession. In these environments, it’s typically the most distressed and highly leveraged companies, the “junk”, that rebound the hardest as refinancing becomes easier.

The second is risk-on or speculative phases, where sentiment dominates fundamentals. In those periods, higher-beta stocks tend to lead, and the more defensive characteristics of quality can become a headwind.

Understanding this pattern is critical. It helps set expectations and, more importantly, reinforces why maintaining discipline through the cycle is so important.

Where we are today

The current environment has been particularly challenging for quality investing.

Based on MSCI data, the most recent cycle of quality outperformance peaked in June 2024. Since then, we’ve seen a sustained period of underperformance that is now approaching two years.

Looking back through time, I’ve identified nine previous episodes where quality underperformed by 10% or more, peak to trough. This current period is the tenth time. What stands out to me is both the depth and duration of this drawdown:

- Around 30% underperformance peak-to-trough

- Roughly 21 months (and counting!)

Only one prior episode saw quality underperform by a greater magnitude, which was the 2003-07 bull market in the run-up to the GFC, where quality underperformed the broader market by a total of 41%. And that was over a period of three and half years whilst the global equity market was raging hot.

From a macro perspective, this hasn’t happened in a vacuum. Rising growth expectations and higher bond yields, the dominant regime since mid-2024, have typically been unfavourable for quality.

However, with geopolitical risks rising due to the Middle East conflict and macro uncertainty increasing, it’s entirely plausible that we are approaching another regime shift.

Staying disciplined when it’s hardest

Periods like this are precisely when the case for quality is most severely tested. And, in my view, most compelling.

It’s tempting to rotate into what’s working, particularly when lower-quality or more speculative parts of the market are leading. But history suggests that chasing those rallies, especially after extended underperformance of quality, tends to be poorly timed.

I don’t pretend to know exactly when the turning point will come. Timing factor cycles is notoriously difficult. But what the data does tell me, consistently, is that over the long term, staying invested in high-quality businesses has been rewarded.

Sources:

1. Novy-Marx, Robert, “The other side of value: the gross profitability premium”, Journal of Financial Economics, 2013

2. Asness, Frazzini & Pedersen, “Quality Minus Junk”, Financial Analysts Journal, 2013

3. Fama & French, “A five-factor asset pricing model”, Journal of Financial Economics, 2014