A project on Spain’s gusty southern coast puts hard numbers on how the replacement - or ‘repowering’ - of turbines will improve the efficiency of wind farms, both financially and in terms of generation, over the next decade.

It was high time. Jutting out into the Atlantic on the very southern tip of the Iberian peninsula, Tarifa is Spain’s windiest town and one of the earliest destinations for the country’s surge in wind farm construction in the 1990s. Its giant white windmills will be among the first to be replaced - or in industry speak, ‘repowered’ - by local renewables specialists Acciona Energy over the next year, in a project that will be duplicated across Europe many times in the next decade.

What’s most striking, however, are the numbers. In Tarifa, Acciona will replace 98 of its 1990s turbines with just 13 new towers. The farm’s production, however, will surge by 72 per cent, producing enough to power 73,000 homes versus the 42,000 it currently provides for1. The economics should also deliver: repowering wind farms carries few of the startup costs in land, leases and approvals that new locations require and the profit margins should be healthy.

It’s been a torrid couple of years for investment in the wind power revolution, but the nature of the troubles are also a sign of a maturing market. A shortfall in grid investment in Europe - in part the result of regulatory bottlenecks that governments have been working to fix - had slowed installations. The US market has suffered from uncertainty around subsidies. High interest rates have also hurt the economics of turbines at a time when manufacturers’ costs have risen.

Paths around these obstacles are emerging. In Germany, where new onshore installations were only 1.5 GW in 2022 (far below official targets), some 7 GW was tendered last year, helped by an easing of the permitting process. A new

Labour government in the UK, if elected, could further boost investment in the grid. The country’s energy regulator, Ofgem, whose charter previously was simply to protect the consumer and keep prices down, now is also tasked with enabling net zero, allowing bills to rise for the necessary investment.

From an investor’s perspective, the most interesting segment at the moment may be turbine manufacturers. Many had been struggling with a development cycle that continuously delivered new technology before they were able to make money from the previous generation - a problem they have now solved.

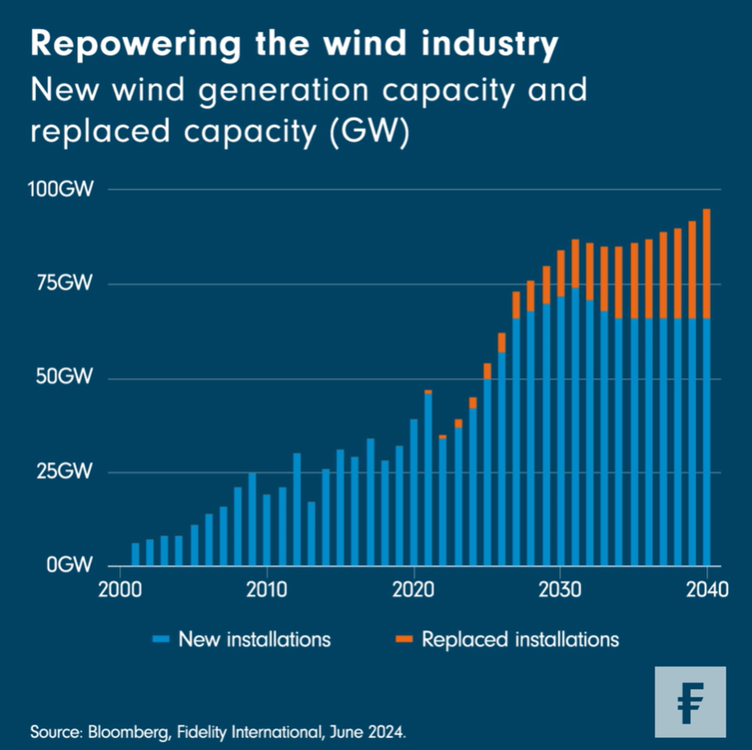

Repowering is one piece of the puzzle. As the chart shows, by the end of the next decade the replacement of existing turbines could make up more than a quarter of all sales. The power generation that’s possible with the new turbines provides an opportunity for manufacturers to cash in on the huge technological breakthroughs and improvements in efficiency of the past 20 years. Wind, hopefully, in their sails.