Key takeaways:

- Chinese economic activity has shown significant divergence and new engines of growth are emerging.

- Given this divergence, the inflation trajectory will likely show modest recovery this year and the central bank will likely pursue a measured easing cycle.

- As strategic priorities become clearer and policy signals turn into concrete measures across key sectors, understanding China’s macroeconomic dynamics will be important for investors.

China enters the Year of the Horse with a more balanced and resilient economic footing. Amid domestic complexities and a dynamic external environment, we highlight six developments that investors should track closely – trends that could shape portfolio positioning in the months ahead.

The shape of economic growth

Controlled stabilisation remains the medium-term policy goal for China and the rebalancing continues in the background of the dual-circulation growth model. However, the composition of growth is undergoing a notable rotation.

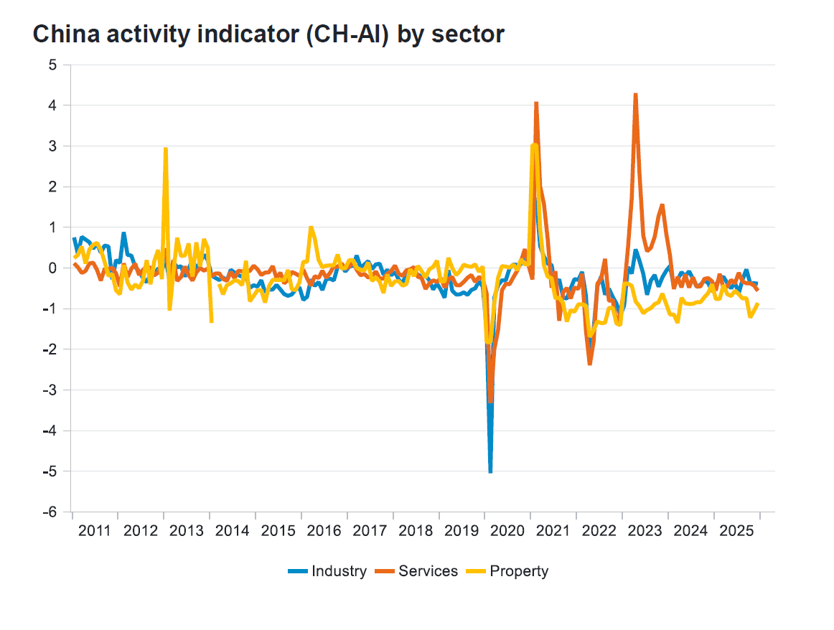

Activity data show divergence across sectors: the property market remains structurally weak, while services and industry have emerged as the primary growth engines. Industrial output outperformed last year, as reflected in record export figures. If these sectors continue to expand despite ongoing property sector drag, it signals that a new growth structure is taking shape.

Chart 1. China’s growth drivers are diverging

Source: Fidelity International, Macrobond, China National Bureau of Statistics (NBS), January 2026

Sustainability of export growth

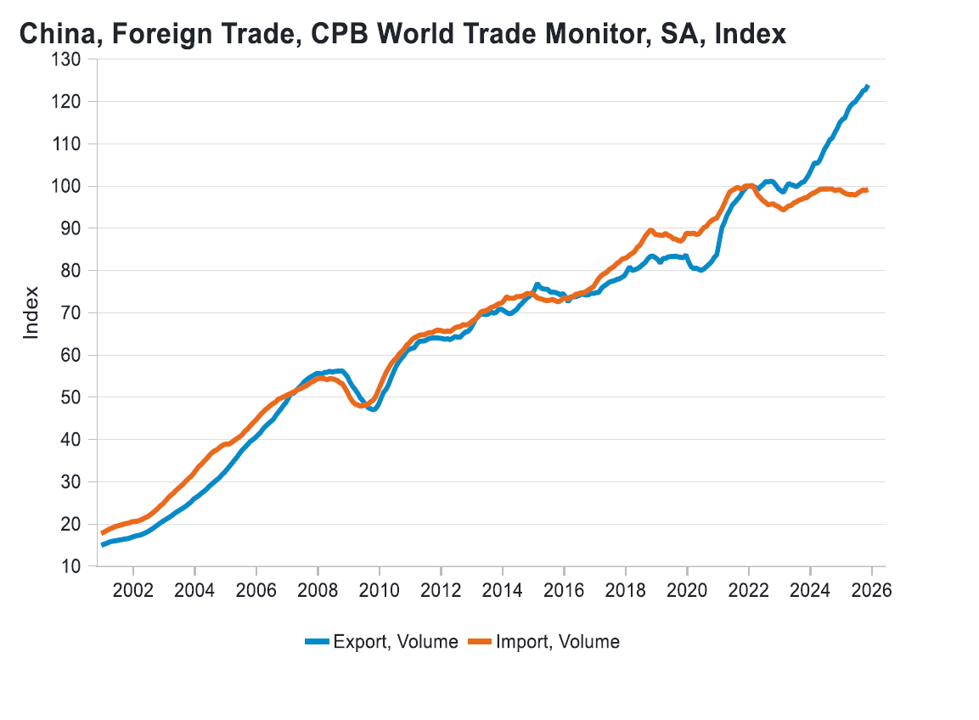

Despite ongoing trade tensions, Chinese exports surged in 2025. While shipments to the US have declined, China has significantly expanded trade with the rest of the world (for example, exports to Africa and Latin America have almost doubled since 2019). Chinese companies are now deeply embedded into the global supply chain, enabling them to capitalise on growth in key sectors of the global economy.

Meanwhile, imports have stabilised. This reflects another structural shift: China has increasingly built its own industrial supply chain, reducing its dependence on intermediate products and instead moving up the value chain by producing more final products.

Chart 2. Slower imports indicate a structural shift

Source: Fidelity International, Macrobond, Netherlands Bureau for Economic Policy Analysis, January 2026

The levelling off of imports also partly reflects the weaker domestic demand compared with global demand. This year, we expect China to focus on addressing this issue as the sustainability of such a large trade surplus is likely to draw greater scrutiny.

Stability of household income and employment

The growth of urban disposable incomes has fallen, but overall income growth remains above nominal growth, which suggests that wage gains continue to offer some support to households. That said, we have seen volatility in income, and if that persists, it is very unlikely that households will feel confident to spend. We expect policymakers to devote more resources into injecting certainty and predictability in incomes and that will likely restore confidence over time and reinforce consumption as a key pillar of China’s sustainable growth.

In terms of employment, jobs increased in sectors such as manufacturing, thanks to ramped up export activity. However, jobs added in these sectors have yet to compensate for the losses in the services and property sectors. We expect policymakers to emphasise job creation under the latest Five-Year Plan.

Inflation outlook

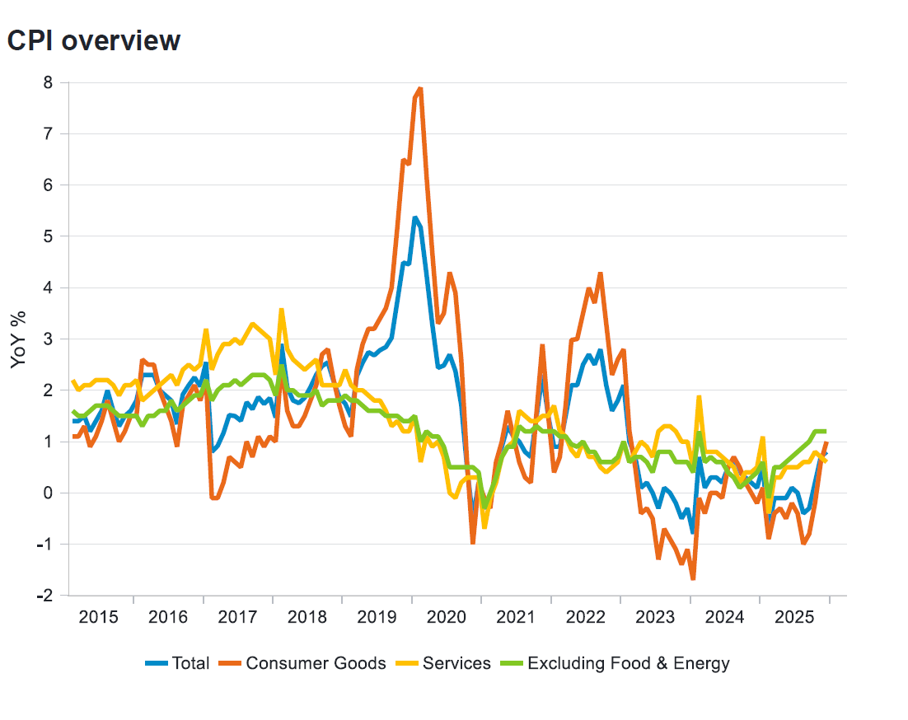

Given the divergence in economic activity, the inflation trajectory will likely show modest recovery this year. We see room for reflation in the producer price index (PPI) driven by supply-side factors such as the ‘anti-involution’ campaign and demand side factors such as improving demand. The consumer price index (CPI) reflation will likely be uneven, with services starting to pick up while prices of goods may stabilise or even fall. Technical factors, such as rebasing the index according to new weights which takes into account the rising services share, could marginally push up core CPI.

Chart 3. CPI recovery will likely be uneven across sectors

Source: Fidelity International, Macrobond, China National Bureau of Statistics (NBS), January 2026

Fiscal and monetary policy outlook

Fiscal policy in China is expected to remain supportive but measured in 2026, with the official budget deficit target remaining around 4 per cent. Local government special bond quotas may rise modestly to sustain infrastructure investment. While the precise composition of the fiscal mix is evolving, a shift toward greater direct support for households would be a constructive development for domestic demand.

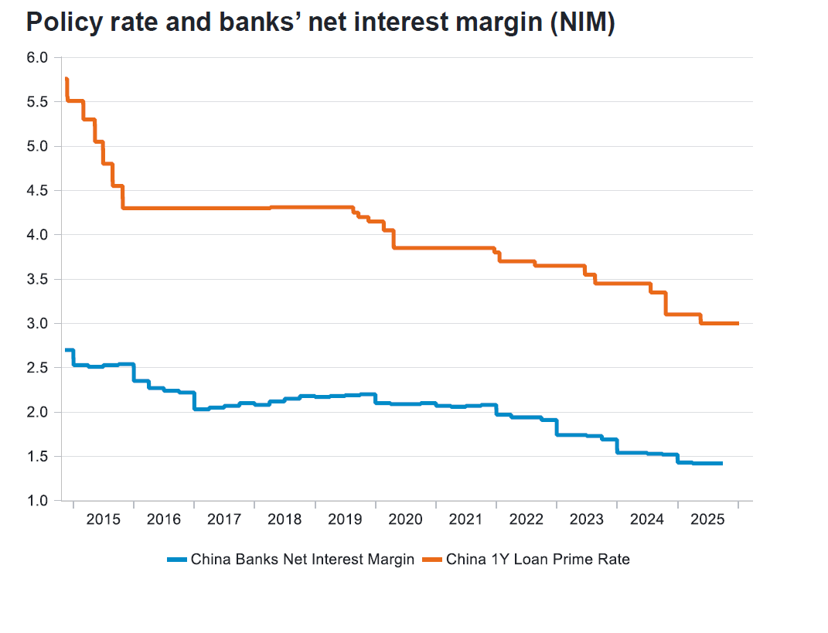

With inflation pressures subdued and growth indicators still soft, the People’s Bank of China will likely pursue a measured easing cycle, balancing growth support with currency stability, employment objectives, and the banking system’s net interest margins. We expect around 10 basis points of policy rate cuts and approximately 50 basis points of reserve requirement ratio (RRR) cuts over the year.

Chart 4. Monetary policy will focus on credit expansion

Source: Fidelity International, Bloomberg, Macrobond, PBoC, January 2026

Implementation of the new five-year plan

This year marks the start of China’s 15th Five-Year Plan, a pivotal policy blueprint that will guide the country’s next stage of development. Over the past five years, policy emphasis has leaned toward the external component of the dual‑circulation strategy. The new plan, however, signals a shift toward strengthening domestic demand, focusing both on deepening China’s industrial capabilities and boosting household consumption. One practical opportunity for policymakers lies in accelerating the development of the services sector, which could deliver gains in employment and productivity.

Against this backdrop, we believe that China’s outlook will become increasingly important for investors, particularly as its strategic priorities come into sharper focus and policy signals turn into concrete measures across key sectors.