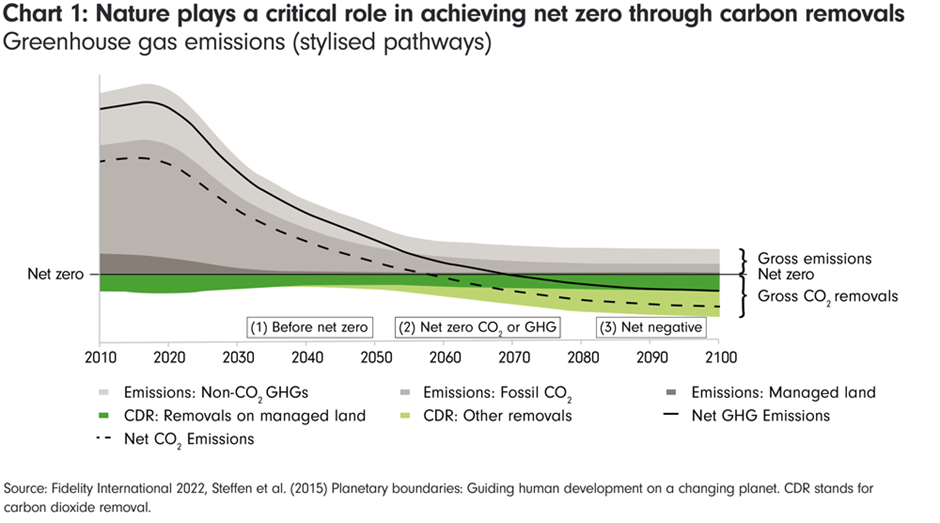

We believe ‘nature positive’ will be the new ‘net zero’ in the coming years as climate change increasingly becomes a subset of how we think about risks to biodiversity and natural capital.

Despite the huge geopolitical and inflationary challenges that beset economies in 2022, sustainable investing continues to evolve at pace, and our approach is evolving with it as systemic themes like nature take on greater prominence.

We seek to contribute to the health and preservation of critical systems by engaging with stakeholders on nature loss, as well as strong and effective governance, climate change and social disparities. These four systemic themes, which we have identified in 2022 (see page 30 of the report), are critical to our purpose of building more sustainable financial futures for our clients.

We have introduced an influence framework (see page 30 of the report) to identify opportunities to engage with a wider set of stakeholders to encourage change in a more holistic and effective manner that is beneficial to our investee companies and ultimately our clients. We aim to engage on these systemic themes over a multi-year timeframe, and within these address relevant sub-themes.

Many of our engagements are intended to address more than one systemic theme as they often interconnect. For example, biodiversity loss is a key driver of climate change, and vice versa. In 2022, we focused on developing a Deforestation Framework to address the risks of commodity-driven deforestation in our investment portfolios by 2025 and to support investee company efforts to achieve net zero targets.

The framework builds on previous engagements with those companies most exposed to deforestation caused by agricultural commodities like palm oil and forms a key part of our approach to a theme that is increasingly being discussed in 2023 - nature and biodiversity.

Nature positive

COP15 in late 2022 proved to be a turning point in recognising the importance of nature impacts if the world is to achieve net zero and avoid the worst effects of climate change. Several initiatives have sprung up to translate this concept into decision-useful factors for investors including the Finance for Biodiversity Foundation and the Natural Capital Investment Alliance, of which Fidelity is a member. But policymakers, regulators and investors have been coalescing around the work of the Taskforce on Nature-related Financial Disclosures (TNFD) which is building a framework around 10 core areas for nature-based disclosure.

While there is no easy way to capture risks and opportunities in relation to nature, unlike carbon emissions for climate, the push for greater corporate disclosure more generally through regulation such as the European Union’s (EU) Corporate Sustainability Reporting Directive (CSRD) is bringing this area into scope relatively quickly and it is being considered for inclusion by global standard setters such as the International Sustainability Standards Board (ISSB).

To explain why biodiversity is important from an investment perspective and the associated risks and opportunities, we have created a biodiversity primer. We believe ‘nature positive’ will be the new ‘net zero’ in the coming years as climate change increasingly becomes a subset of how we think about risks to biodiversity and natural capital.

Doing the work on net zero

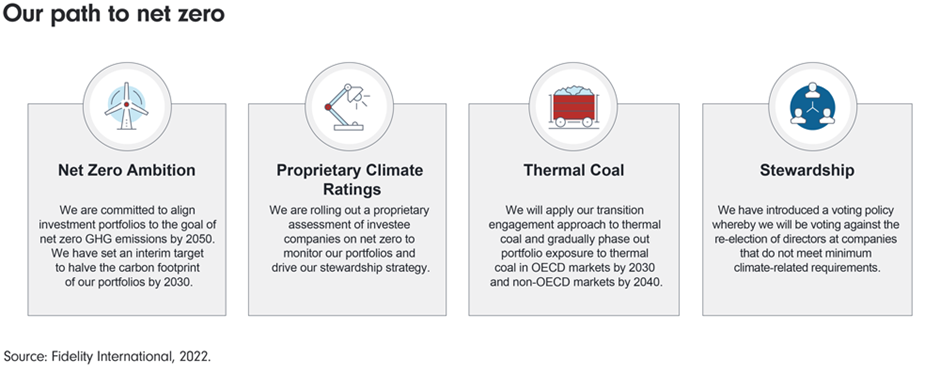

At the same time, we continue to work with investee companies to reach net zero through on-the-ground decarbonisation. Our Climate Investing Policy, published in 2021, sets out our net zero targets and how Fidelity plans to achieve them. At its core is our engagement strategy targeting the highest emitters in different ways.

For the thermal coal sector, for example, we have developed a specific policy to engage intensively with companies on their transition pathways to help them switch to different business models and gradually phase out their carbon-intensive activities.

We aim to end investment in thermal coal by 2030 in OECD countries and in the rest of the world by 2040. In 2022, we began engaging with firms who were more advanced on their journey towards net zero to explore their practices, specifically how they were enabling a just transition through retraining their workforces as they phase out coal.

In 2023, we are focusing on companies with higher risk of new coal development and divestment to private firms with no intention of phasing out coal. We continue to participate in the Asia Transition Platform, run by Asia Research and Engagement (ARE), engaging alongside other investors with over 50 Asian financial institutions and coal-exposed power companies to raise awareness and share best practice on accelerating the transition.

We use our proprietary Climate Rating to assess where a company is on its transition journey and to prompt engagement with laggards. We also develop strategies and building blocks for clients wishing to invest in the transition through climate leaders, solutions providers, or those with the greatest potential for transition and carbon reduction.

Next steps on the net zero pathway include using green revenue tools (e.g., EU Taxonomy or Sustainable Development Goals alignment) to identify climate opportunities. We also use carbon footprints and scenario alignment at asset and portfolio level, in addition to our climate and ESG ratings, to map climate risks. Setting net zero targets at fund level will help further integrate climate considerations into investment decision-making and drive the transition across our fund range.

Transition plans under construction

In 2022, more and more companies set net zero targets. In 2023, we are seeing much greater focus on how these will be achieved and the development of more granular transition plans. This is being driven by investors like Fidelity who require greater visibility on corporate plans and associated capex (to mitigate climate risks to portfolios and to enable our own corporate transition plan) and by regulators and policymakers at global, regional, and national level.

For example, the EU is expected to include transition plans in its corporate disclosure requirements for companies when conducting due diligence, while the UK has indicated it could make transition plans mandatory for large companies (see page 15 of the report), using a framework designed to complement not only the current Taskforce for Climate-related Financial Disclosure (TCFD) reporting framework, but also the emerging ISSB accounting standards.

Fidelity has contributed to these discussions through our engagements with regulators and standard setters, responding to consultations on the type of disclosure needed to make robust investment decisions and how to build capacity for sustainability reporting across economies. We have encouraged regulators to ensure as much global interoperability as possible and to integrate nature-related metrics as these emerge. The social aspects of the transition remain crucial.

Social matters

While energy prices had begun to fall as we entered 2023, the shock of high inflation to Western economies persists and interest rates continue to rise at the time of writing. As a result, many firms have been dealing with substantial and sustained price rises which have put pressure on other sustainability objectives in the short term.

We have engaged with companies on this topic specifically as it relates to differentials in pay for executives and staff and continued to engage on measures to improve diversity and inclusion across different sectors and geographies, including voting against boards which do not meet the minimum number of female directors required by our voting principles (see page 50 of the report).

Effective governance is key

Effective governance at multilateral, national, industry and corporate levels is a precondition of effective action on sustainability. Not only do signs of poor governance raise concerns about sustainability in other areas, we can use governance measures such as voting to encourage changes in corporate behaviour; they offer an opportunity to explain clearly why we have chosen to vote for or against a proposal, or abstain, and share our thinking directly with a company. We therefore consider strong governance to be an essential tool to drive change across our other systemic themes, helping us, our investee companies and our clients make progress towards net zero, while tackling nature loss and facilitating a just transition.