The US Federal Reserve (Fed) is clear that it will continue to tighten aggressively to bring inflation under control. The risks that it could go too far, however, are becoming more acute.

This is not the 1970s, it’s worse. And neither is Jerome Powell the new Paul Volcker. Both are eras characterised by high levels of inflation met by aggressive central bank action. But the leverage in today’s global economy means Powell’s hand is severely curtailed where Volcker’s wasn’t.

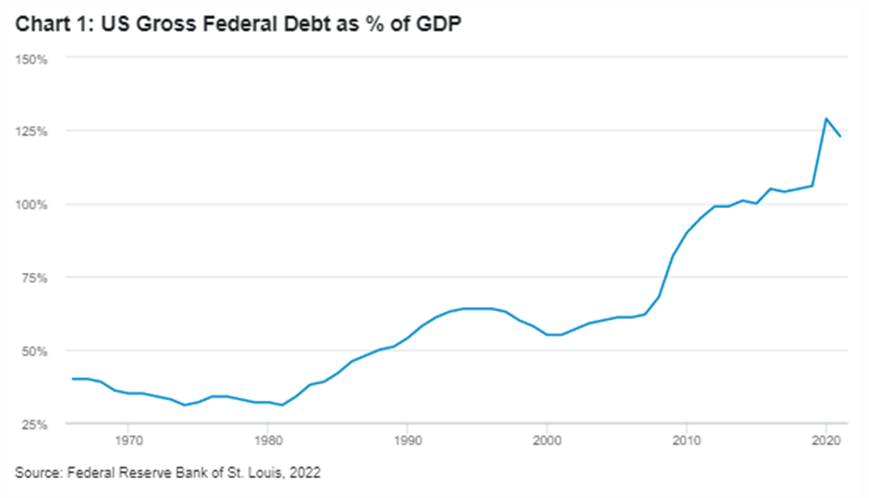

Chart 1 shows the extent to which US debt has grown as a percentage of GDP over the past 60 years. The huge levels of debt now in the system increase the stakes for the Fed as it tightens policy. It only takes a small hike today to have a profound effect on the economy.

Nevertheless, the Fed now appears fully committed to achieving a high level of demand destruction if that’s what it takes to bring inflation under control. The risk that they overshoot, and the US finds itself stuck in a deep recession, is higher now than it was four decades ago.

The leverage in today’s economy can in part be explained by a decade of ultra-low interest rates. World economies have grown used to cheap money, and most now require real yields to remain below zero if they’re to function properly. That is not what they’re getting - US 10yr real yields now sit above 1.1%. The Fed’s current reset could contribute to huge demand destruction.

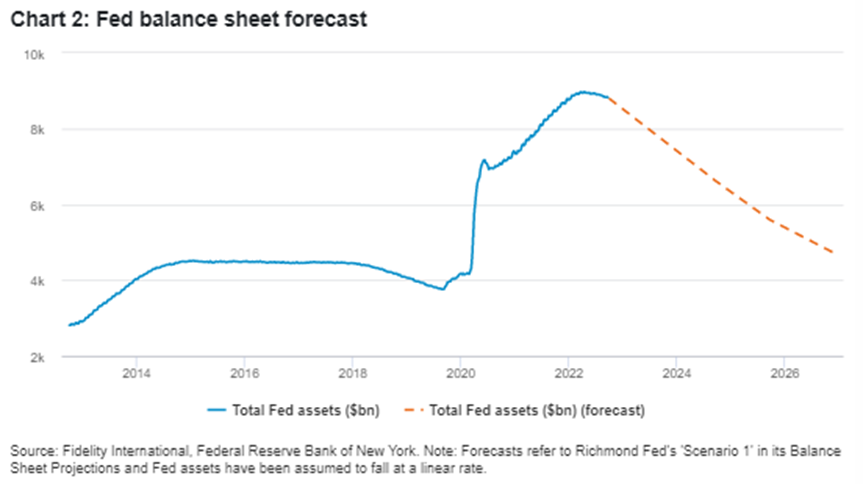

The other factor to consider here is the Fed’s new quantitative tightening programme, which will reduce its balance sheet by US$95 billion per month. There has already been a US$7 trillion reduction in the dollar value of world money supply. Given the trajectory of balance sheet reduction highlighted in Chart 2, coupled with continued rate hikes, we believe there could be a further US$5 trillion reduction in money supply yet to come. The resulting level of demand destruction heightens the risk of a hard landing. The Fed must ensure it does not go too far, too fast, in trying to correct the mistakes of the past two years.

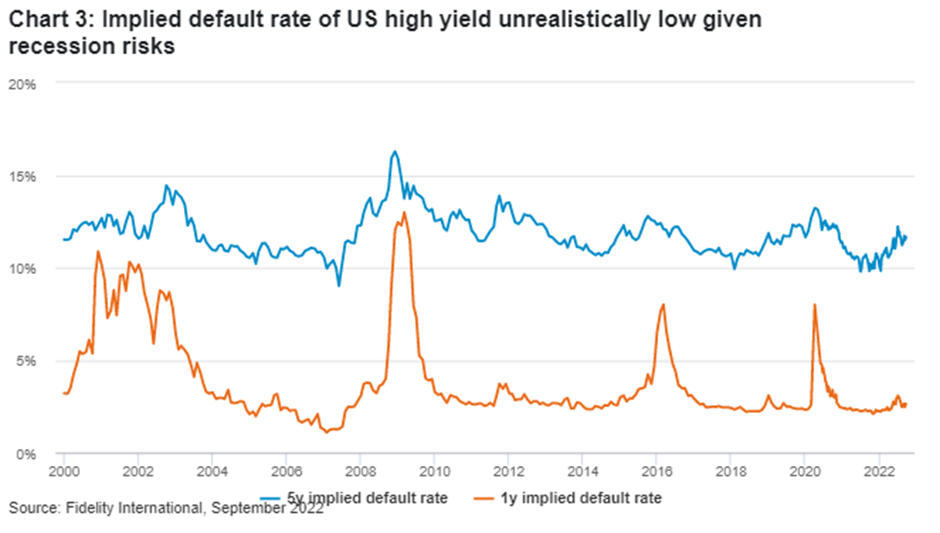

Against this backdrop, now is a time to be defensive. Were the US to head into recession, as looks likely, we should expect credit defaults to rise significantly. Yet, the market is yet to reflect these risks. This is evident in the implied default rate of US high yield. According to Fidelity International research, market implied default rates for the high yield segment currently stand at just 2.7 per cent in the US - roughly what might be expected in only a very shallow recession. By contrast, realised defaults peaked at around 14 per cent during the global financial crisis, according to research from Bank of America Merrill Lynch, with a market implied default rate of above 12 per cent. High yield is not offering investors enough cushion in a rising default environment.

Where current high yield spreads would leave investors more vulnerable in a rising default environment, investment grade is offering a positive “spread premium” - that is, current spreads minus an allowance for default losses - which would adequately compensate investors for potential losses in line with historically high defaults rates.