In the past 60 years, only two US presidential election years have brought with them a drop in Wall Street’s main index: in 2000, when the dotcom bubble had just burst, and in 2008, when sub-prime mortgages had done worse. Neither had much to do with politics.

There is some differentiation when you compare other years in the electoral cycle. Pound for pound, the strongest year of the four on average is year three, when midterm elections have often split control of the three arms of US government, leaving Washington tied in political battles and the business world free to get on with, well, business.

The first year of each new administration has also tended to deliver returns - some 8.3 per cent on average, while year two has the worst record - only 4.2 per cent on average.

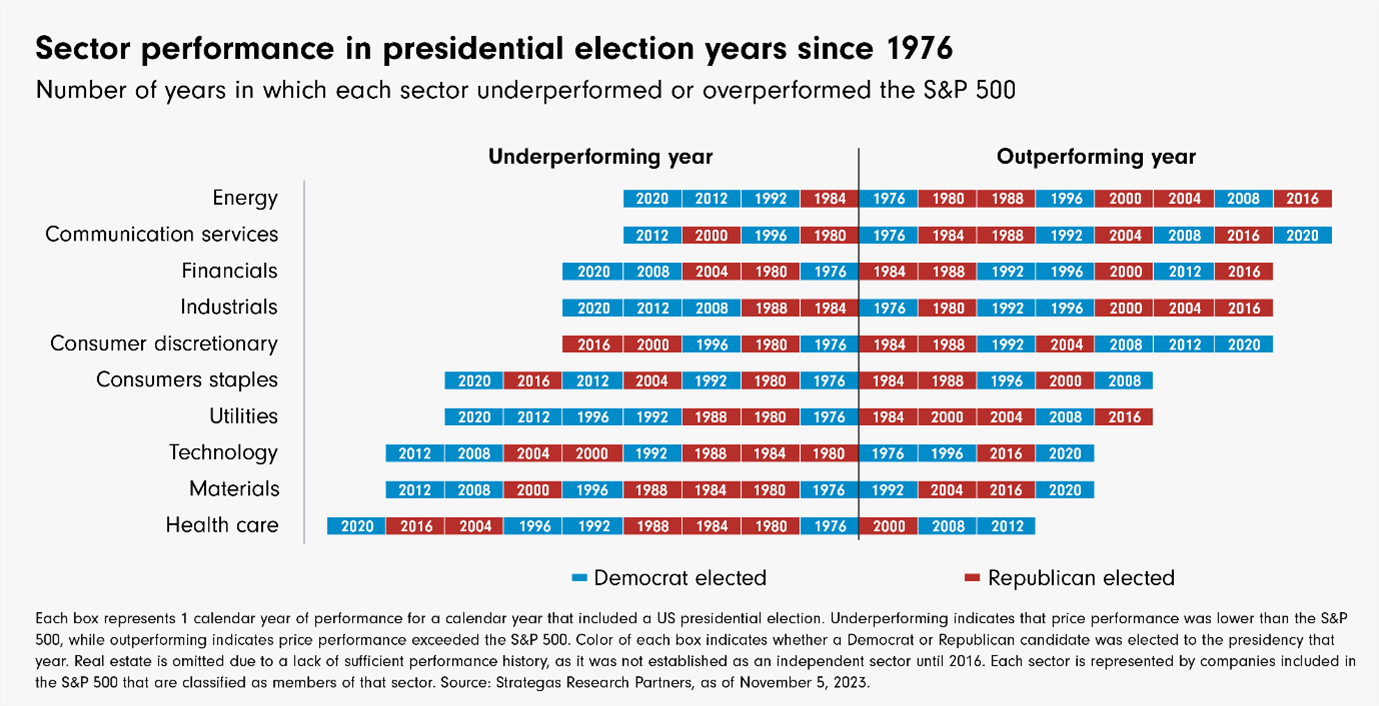

Making convincing predictions about the impact of one or other party winning the election, however, has proven perilously difficult. The data set from a quantitative point of view is small, but looking back to the mid-70s, the mix of sectors out- and under-performing the wider market varies widely prior to Democrat and Republican victories.

The exact mix of Democrat and Republican control of the White House and Capitol Hill gives us a little more to go on. A split Congress and Senate reliably delivers higher - and similar - returns, no matter who holds the presidency. “The big conclusion for me is that, over the long term, who is sitting in the White House doesn't matter for the economy,” says Fidelity portfolio manager Rosanna Burcheri.

Focus on fundamentals

So where to look instead?

Burcheri has a handful of strategic calls which are unlikely to be influenced by the outcome of the vote. One is the conviction that a steady tightening of trade controls and tariffs will deliver more reshoring in the United States and more reorganisation of global production to allow for restrictions on trade with China.

“For me, transport and automation are two big themes,” she says. “If there is a re-industrialisation in the US, those companies that have to move things around should benefit. Likewise, the companies who provide the equipment that you put in the factory.”

That may, however, have knock-on effects for prices and the monetary policy equation.

“Isolationism is going to make things more expensive by default,” she argues. “I know a number of companies that have announced their intention to invest in the US on the back of the Inflation Reduction Act legislation, but it is taking them a while to get up and running because they cannot find the qualified people they need and they are worried about the cost of energy.”

Fiscal reins

Another US-focused portfolio manager, Aditya Khowala, argues that a second theme is likely to be the reining in of the public spending that marked both the official response to the pandemic and the years since. A period of budget retrenchment is likely to follow the elections - and that may weigh on growth expectations, and markets, towards the end of this year, he believes.

“Stocks should continue to do well for the next few months but we may see more nerves come October or November,” he says. “Fiscal spending will have to slow down after the election as it will be irresponsible to run such high deficits on a structural basis,” he says, predicting a 2-3 percentage point cut in the fiscal deficit next year that will weaken overall growth.

Strong dollar risks

Both fund managers worry about the implications of those public spending choices for the macroeconomic balance next year. Higher US fiscal outlays adds up to higher interest rates - a narrative that has already been playing out in markets in 2024. Inflation is proving sticky and Burcheri argues that the swing towards protectionism and the green transition mean it’s not going away anytime soon. That leaves the Federal Reserve - and the economy - stuck with potentially painful high interest rates and the world stuck with a strong dollar.

Emerging markets in particular would be vulnerable to continually wide fiscal deficits leading to higher US yields, as these are highly sensitive to a stronger US dollar and global cost of capital.

Macro run in

The run in to the election comes at a time when monetary and fiscal policy have had a huge impact on US growth and markets. The next few months are also crucial in those areas. How far the Fed turns back the dial on interest rates, how fast inflation falls, and what verdict debt markets have on the outlook for public borrowing, may prove far more important than partisan political promises and the outcome in November. That’s what history tells us too.