Despite US ruling, tariffs are part of the landscape now

The Supreme Court struck down US President Trump’s 2025 sweeping global tariffs in a 6-3 ruling on Friday, 20th of February. The decision covers all of the country-wide reciprocal tariffs in the International Emergency Economics Power Act (IEEPA), including the fentanyl tariffs on China, and the border emergency tariffs on Canada and Mexico. Other measures, including pre-existing tariffs on China and sectoral tariffs on the likes of steel, aluminium, and autos, remain in place.

As anticipated, the administration moved quickly to invoke Section 122, which allows a 10 per cent temporary tariff on all countries but which US President Trump has said on social media would be set at 15 per cent for all countries for up to 150 days. The untested law requires congressional approval for anything beyond that timeframe. The measure applies to goods shipped after tomorrow (24th February) or received by importers after Friday (28th February) and replaces nearly 80 per cent of the IEEPA tariffs. Based on prior guidance from US officials, the administration is likely to reconstruct the previous tariff architecture through alternative measures. In essence, and notwithstanding additional legal and administrative hurdles, the IEEPA ruling does little to disrupt the current trade policy. Tariffs are here to stay.

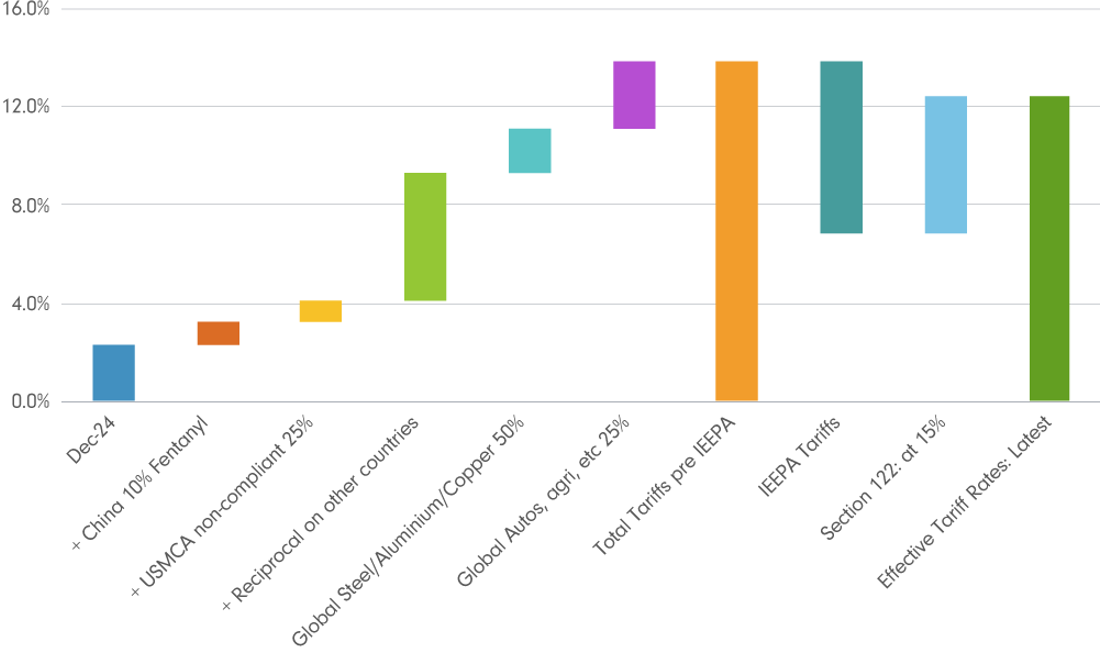

Chart 1: Changes in US tariffs

The change in effective tariff rates

Source: Fidelity International, US Census Bureau, US International Trade Commission, February 2025.

That said, there is a modest appeasement of the policies, at least in the near term until the prior structures get rebuilt. As per our estimates, the combination of the IEEPA ruling and the new 15 per cent Section 122 tariff lowers the effective tariff rate (ETR) by about 1.5 percentage points to 12.4 per cent. We are still reviewing the exemptions outlined in the executive order but currently assume they broadly mirror those under IEEPA.

This paints a relatively benign outcome in the near term. If sustained, these levels would lower our inflation forecast by roughly 10-15 basis points and cut customs revenues by around US$40-50 billion per annum. Consequently, the reduction in tariff drag should provide a modest lift to growth and a corresponding deterioration in fiscal deficit by around 0.1 per cent of GDP, all things being equal.

But Section 122 is only a temporary measure. After the 150-day window expires, there is considerable uncertainty around the rebuilding of the tariff wall (likely through new implementation of Sections 301 and 302 of the US Trade Act which relate to countries and sectors respectively). We expect the effective tariff rate to settle in the 12-14 per cent range although the composition is likely to remain in flux.

A larger one-time macro effect may stem from refunds of previously collected IEEPA tariffs, which we estimate at more than US$150bn as of January 2026. The Supreme Court ruling did not explicitly address this issue, but the Court of International Trade (CIT) could begin adjudicating claims. Nearly 1000 companies have filed suit for refunds (comprising some 50-70 per cent of the tariff value) and this number could increase further in coming days. A full recoup of IEEPA tariff costs by corporates, assuming they absorbed the burden, would lift corporate cash flow and profits by around 0.5 per cent of GDP, with a corresponding one-off hit to government revenues and the fiscal deficit. Legal and bureaucratic delays are likely to make the process more protracted, however.

Winners and losers

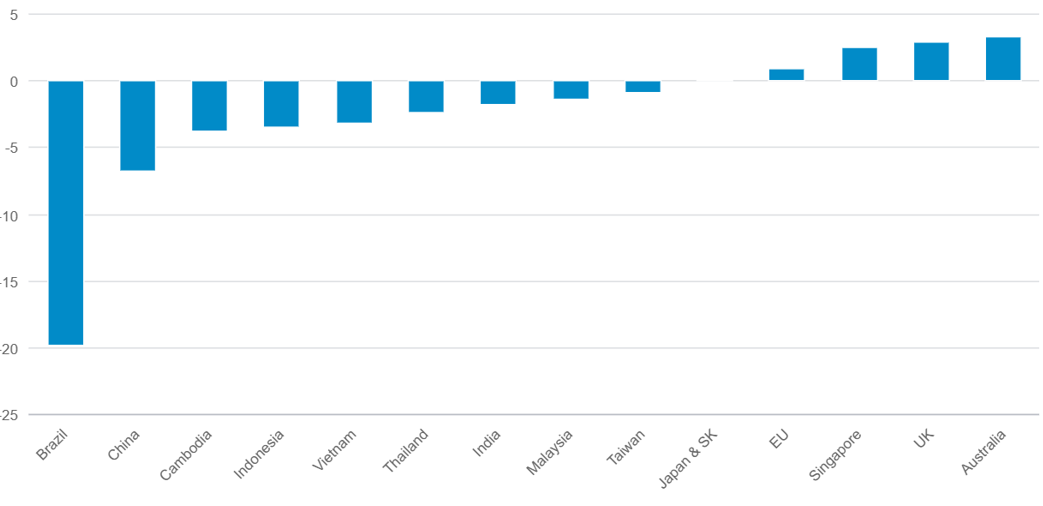

From a country level-perspective, the clear winners from the IEEPA ruling include Brazil, China, Cambodia, and Indonesia. Countries such as the EU, Australia, UK, and other smaller nations that had a 10 per cent existing tariff rate lose ground. Notably, there is not yet any formal documentation supporting US President Trump’s post about raising the Section 122 tariffs to 15 per cent. It should be straightforward for the administration to retain 10 per cent for smaller economies, particularly allies such as the UK and Australia that negotiated a deal, while applying 15 per cent more broadly elsewhere. This creates downside risk to our current effective tariff rate estimate of 12.5 per cent. If a revised order applies 15 per cent only to a subset of countries, the aggregate rate would move lower.

Chart 2: Country-level change in effective tariff versus previous

Source: Fidelity International, US Census Bureau, US International Trade Commission, February 2025.

Implications for Asia

China: China is a relative near-term beneficiary of the IEEPA rollback and shift to a temporary 15 per cent Section 122 regime, with estimates suggesting its average tariff burden declines by some 7 percentage points. This reduces immediate escalation risk ahead of the Trump-Xi meeting scheduled for the end of March. However, follow-up actions remain likely, and broader tensions over export controls, supply chains and technology persist.

Japan, Korea, Taiwan: The potential interim 15 per cent flat regime is broadly neutral although these countries have committed sizable US investment pledges (Japan US$550bn; Korea US$350bn; Taiwan US$250bn). Sectoral exposure - autos, semiconductors, steel, and aluminium - leaves them vulnerable to renewed policies. However, given their strategic alignment with the US, these countries are likely to be given exemptions and will stick with existing commitments.

Asean: Effects are mixed. Economies previously facing higher country-specific rates – Indonesia and Malaysia, for example - see relative relief under a uniform 15 per cent structure. Those closer to the prior baseline, such as Singapore, face a modest increase. The narrower tariff differential with China may reduce transshipment incentives and test export competitiveness.

Market outlook

Market reaction to the announcement was modest as the decision was widely expected. US equities edged higher on improved risk backdrop, while bonds sold off marginally, reflecting fiscal concerns. The dollar remains under pressure given the elevated policy uncertainty and we await more clarity on the rebuilding of tariff walls and IEEPA refunds process.

Asian equities were broadly in the green on Monday, 23rd February with relative outperformance in Hong Kong, Indonesian, and Indian equities. China markets remained shut for the Lunar New Year holidays, but we expect the tactical outperformance to continue once markets reopen. In the near term, the backdrop for Asian equities looks constructive. Tariff rates are easing at the margin and expectations of relative stability in the run-up to the Trump-Xi meeting are supportive. However, greater clarity is needed on the rebuilding of tariff walls and the IEEPA refund process before medium-term winners and losers emerge. We are also closely monitoring geopolitical risks, particularly around Iran, alongside the ongoing rotation within equity markets. In this environment, we continue to advocate diversification in portfolio construction.