Key takeaways:

- One of Europe’s key transition levers is demand reduction: Beyond renewables, upgrading existing energy-intensive buildings offers a fast, practical way to cut energy use and relieve pressure on constrained grids.

- Energy economics have fundamentally shifted: With higher and more volatile power prices, efficiency is now a competitiveness issue, particularly for energy-intensive occupiers like cold storage and automated logistics.

- Retrofits are proven, scalable and increasingly required: Mature technologies such as heat pumps, efficient HVAC, rooftop solar and batteries align with tightening EU regulation, making upgrades a question of timing rather than choice.

- Brown-to-green creates economic alignment: Lower operating costs can offset higher rents, supporting “green premiums” while improving income resilience for owners and delivering measurable emissions reductions.

If you trace where global climate investment is heading, a clear pattern emerges. In 2025, the world invested US$2.3 trillion1 into the low-carbon transition, with most of this capital flowing into areas we constantly hear about such as renewable power, electrified transport, grid upgrades, and energy storage. These remain crucial pillars of the transition, and they continue to attract both policymaker attention and investor enthusiasm.

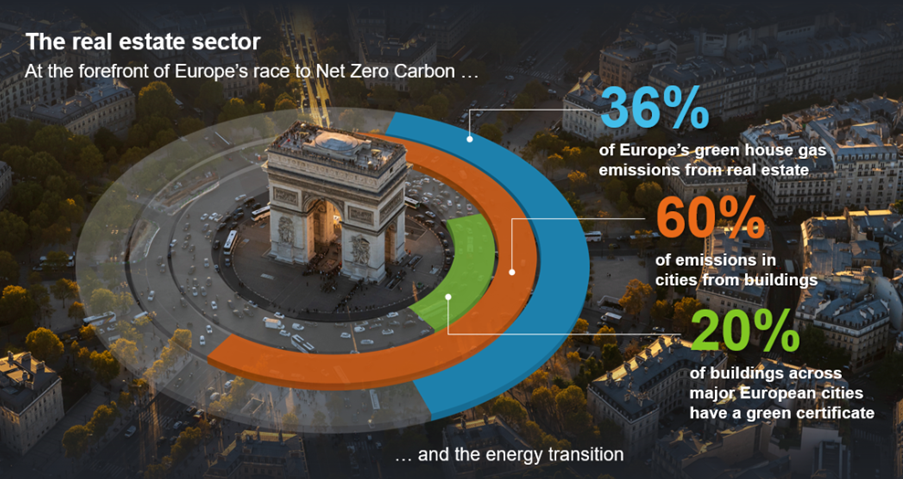

But underneath this headline story sits another one, much quieter but no less important. Many of the gains we need over the next decade will not only come from adding more clean energy supply, but also from using less energy in the first place and removing pressure from the grid bottleneck. And within that realm, energy efficiency in logistics assets in Europe stand out as they benefit from the perfect storm of rising energy prices, regulatory clarity, physical infrastructure constraints and the practical needs of occupiers. As illustrated below, real estate sits at the centre of Europe’s decarbonisation challenge.

Source: Fidelity International, 2025; European Commission, February 2020 (In focus: Energy efficiency in buildings (europa.eu)); JLL Research, May 2022; CBRE Research, The Value of Green Building Features, August 2022.

A shift in perspective: From making power to reducing demand

Across Europe, many logistics buildings were constructed long before today’s operational and energy demands emerged. Yet the activities now taking place inside them like automation, electrified fleets, temperature-controlled zones, and increasingly complex distribution patterns, are raising electricity needs at a time when grid capacity in many regions is already strained. The gap between how these buildings were originally designed and how they are used today is widening.

This is what makes the retrofit opportunity so compelling. Around 75% of Europe’s building stock is energy‑inefficient, yet more than 85% of those buildings are expected to still be in use by 2050. In other words, most facilities were never designed to meet today’s energy‑performance expectations, putting them at risk of becoming stranded assets unless they are made fit for the future. Upgrades such as removing gas and transitioning to heat pumps, improving HVAC efficiency, installing LED lighting, adding rooftop solar, and, where suitable, integrating battery storage offer relatively straightforward pathways to cut energy consumption and stabilise operating costs.

These are not emerging technologies, they are established, predictable interventions. In a market where energy prices remain volatile and regulatory expectations continue to rise, that predictability is becoming increasingly valuable.

Why now? Europe’s energy landscape has shifted

One of the reasons brown-to-green upgrades are drawing more attention today is that the economic reality for occupiers has fundamentally changed.

Since the Russia–Ukraine conflict, and now with the Iran conflict, Europe’s energy prices have not simply spiked, they have settled into a new normal: higher and more volatile. For energy intensive tenants like cold storage operators, automated logistics firms, light manufacturing, energy often represents 25–30% of total expenses. In that kind of cost structure, the volatility of the cost of energy becomes a business risk.

A warehouse that once looked merely dated can now threaten competitiveness and because tenants increasingly care about overall occupancy cost rather than just rent, energy efficient buildings with onsite power generation are more likely to retain demand through different market cycles.

At the same time, regulatory expectations are no longer abstract. The 2024 Energy Performance of Buildings Directive (EPBD) and the EU’s Renovation Wave are tightening minimum standards and effectively accelerating a continentwide retrofit programme. With threequarters of the EU building stock deemed energy inefficient, the question is no longer if buildings will need to be upgraded, but when and how.

A shortage of better buildings

Even with rising expectations, the supply of high performing logistics assets is not growing nearly fast enough to meet tenant needs. Core logistics corridors across Europe continue to experience strong demand but offer a surprisingly thin pipeline of sustainable stock.

That scarcity is important: it means that buildings retrofitted to modern performance levels are not simply greener, they are also more competitive within their own leasing markets. The economics become self-reinforcing. Lower energy bills help tenants manage costs during periods of uncertainty. In turn, landlords benefit from more predictable occupancy and stronger liquidity.

How this fits within the broader transition landscape

Compared with renewable generation or transmission infrastructure, which face long permitting processes, interconnection queues, and system congestion, logistics retrofits sit in a different category. They:

- Require shorter timelines

- Involve mature technologies

- Offer clearer cause and effect between investment and outcome

- Directly reduce demand on already congested grids

This does not diminish the importance of supply-side investment. It simply highlights that reducing consumption in existing buildings offers a complementary and often more immediate way to ease the transition’s bottlenecks.

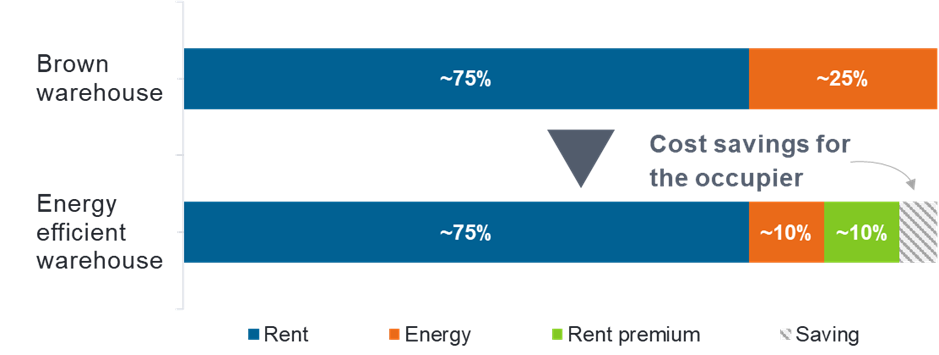

How brown-to-green upgrades translate economically

The economics of logistics buildings increasingly hinge on energy performance. In most facilities, rent accounts for roughly 75% of occupancy costs, while energy makes up much of the remainder. This means that even moderate improvements in efficiency and onsite power generation can meaningfully reduce the overall cost to the tenant. In many cases, total occupancy costs can fall even if rent rises to reflect the retrofit, this is what we call a “green premium”.

Decarbonised buildings are cheaper to occupy: Total occupancy costs breakdown

For illustrative purposes only, these can vary significantly from one building to another and could therefore reach values outside of the ranges mentioned above.

Recent occupier data suggests this trade-off is becoming more widely accepted. CBRE’s 2024–2025 European Logistics Occupier Survey shows a growing share of tenants are willing to pay a rent premium when it leads to lower or more predictable energy bills. The proportion willing to pay a premium equivalent to their expected operating cost savings increased year-on-year, indicating that many occupiers now see higher performing buildings as cost neutral over the lease term.

These dynamics create a practical alignment that has historically been difficult in a price sensitive sector:

- Occupiers gain operating certainty

- Owners improve income resilience and liquidity

- Policymakers see measurable emissions reductions

- The broader system benefits from reduced load given that these buildings become self- sufficient from an energy perspective.

In a market shaped by higher energy prices and rising regulatory expectations, this alignment is becoming central to how value is created in European logistics real estate.

Cold storage

Cold storage is an interesting adjacent story. It serves essential sectors like food distribution, pharmaceuticals and has stable, long-term demand. Because it is energy intensive and technically more complex, even small efficiency improvements can have outsized effects. The European market remains fragmented, but with some hubs like Rotterdam, Antwerp and Hamburg, leaving room for consolidation and professionalisation.

A sector that sits quietly at the intersection of policy, economics and system need

European logistics real estate is not the most visible part of the energy transition. But it is one of the places where the pieces align: rising energy prices, regulatory clarity, physical infrastructure constraints and the practical needs of occupiers.

Brown-to-green upgrades do not solve every system challenge, but they do something both immediate and useful: they reduce overall energy demand, remove pressure from the main bottleneck (the grid), lower emissions, and improve building performance, often within months rather than years. In addition, they extend the life of assets that otherwise would have risked becoming stranded with all the embodied carbon within them.

In a transition that is often defined by very large ambitions, logistics retrofits offer a reminder that some of the most meaningful progress happens quietly, in upgrading the buildings that keep Europe’s goods, food and essential services moving, all while creating strong returns for investors.

Source: 1 - BloombergNEF’s New Energy Outlook 2025