Biodiversity is a multi-faceted area that is considered integral to mitigating and adapting to climate change. We outline why we believe biodiversity matters to investors and how we are approaching this critical issue.

Biodiversity comprises the variety of living components of natural capital such as animals, plants, fungi, and micro-organisms. These components interact to provide us with the “ecosystem services”, such as pollination, food production, air circulation, medicines, and carbon sequestration, on which our very existence relies. Estimates suggest roughly half of global GDP is either moderately or highly dependent on nature1.

If we continue to damage these ecosystem services, we will not be able to keep to the 1.5°C ‘safe landing’ pathway, set out by the Intergovernmental Panel on Climate Change; climate change is also considered one of the major threats to biodiversity and is expected to become the dominant driver of biodiversity loss — acutely so in tropical regions — in coming decades, creating catastrophic feedback loops that will have a big impact on supply chains, livelihoods, and lives.

Global wildlife populations have fallen an estimated 70 per cent over the last 50 years and a further million animal and plant species (12 per cent of the current 8.1 million in total) are facing extinction. Biodiversity loss is also causing a decline in soil fertility which will make it challenging to meet the still growing global demand for food.

Investors therefore might need to consider the types of biodiversity-driven investment risks embedded in portfolios. These include physical, disintermediation, regulatory, legal, transition, and reputation risks.

How are policymakers responding to biodiversity risk?

Policymakers are increasingly focused on biodiversity risks and nature more broadly. COP15 in Montreal in December 2022 delivered agreement of the Global Biodiversity Framework, an overarching mission to halt and reverse biodiversity loss by 2030 with 23 underlying targets to work towards that goal.

There has also been a wave of deforestation-related legislative initiatives including in the UK and Europe, while reporting and disclosure standards are seeking ways in which to include nature. The Taskforce on Nature-related Financial Disclosure framework (TNFD) has been set up to drive consistency and comparability across biodiversity disclosure, in the same way that the Taskforce on Climate-related Financial Disclosure (TCFD) was. It is due to be finalised in September and the ISSB is considering whether to add biodiversity to its sustainability disclosure standards.

What kind of opportunities could nature investing offer?

Climate solutions such as wind and solar have become economically viable within a relatively short period, and we expect the right policy support for investing in nature could trigger uptake at an even greater rate despite it being a more complex area.

Industry estimates suggest we will need around US$8.8 trillion of cumulative investments in nature between now and 2050 to ensure our biodiversity risk is manageable2. Currently, that global annual investment number is only US$146 billion. That is a significant gap and an enormous addressable market for those companies that develop processes and solutions to halt or reverse nature loss and mitigate risks to natural capital. Given we need to spend an estimated US$100 trillion on tackling climate change between now and 2050, and climate change causes nature loss and vice versa, it is possible nature investments may need to be even greater.

What does it look like in practice?

Biodiversity is a nuanced and multi-faceted investment space and there are a range of approaches.

At Fidelity we seek to address biodiversity as an investment theme in the following ways:

- Identify key biodiversity risks and their potential impact on portfolios and engage with issuers on managing and mitigating those risks; this includes analysis of the highest impact and dependency sectors and key nature loss drivers

- Invest in companies we consider are leading the way on nature preservation and recovery through their operations

- Invest in companies building nature-based solutions to help mitigate impacts

We have developed our own proprietary tools designed to integrate sustainability into our fundamental investment research. Biodiversity is explicitly captured in our proprietary ESG ratings framework for those sectors where our investment teams deem it material, with 78 of the 127 sub-industries mapped to at least one biodiversity indicator.

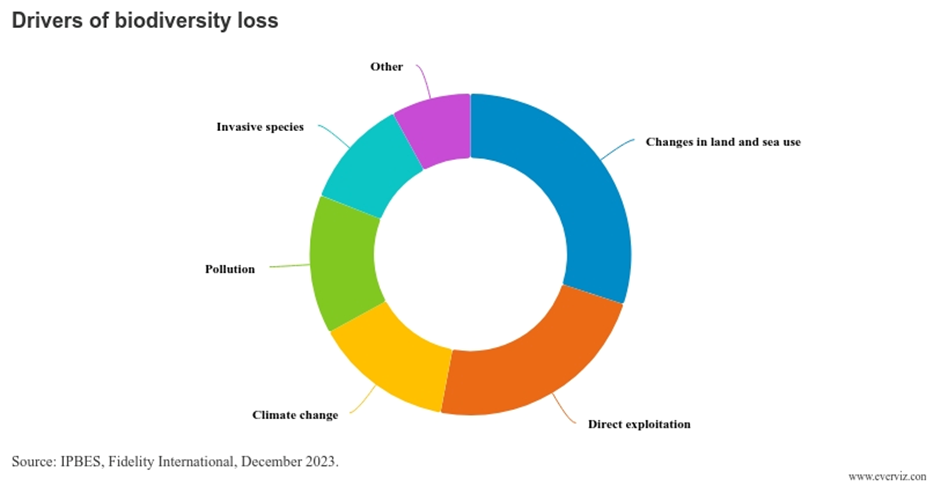

We have several ongoing thematic and collaborative biodiversity-related engagements, including around climate change, pollution, land and sea use change and direct exploitation (see page 45 of the report). Deforestation remains a flagship thematic engagement for Fidelity as more and better data (e.g., from satellites) helps issuers understand the risks to their supply chains.

Finally, we are a member of several industry initiatives including the Finance for Biodiversity Pledge. As a part of this pledge, we have several commitments which include assessing impact and setting targets to report on biodiversity matters before 2025. We are also contributing to discussions around what the TNFD should eventually contain.

Sources:

- World Economic Forum (2020) Nature Risk Rising: Why the Crisis Engulfing Nature Matters for Business and the Economy

- UN Environment Programme, State of Finance for Nature report, May 2021