The post-2020 investment landscape has been characterised by higher inflation, elevated yields, and a shift in policy regimes, all contrasting with the benign environment that dominated the 2010s. Shocks to markets then were largely demand-driven and occurred in a low-inflation, policy-supportive environment. For most investors, a 60/40 split between equities and bonds respectively worked in guiding them through any volatility.

That has changed. Our view is that we’re moving into an era of global fragmentation, characterised by lack of consensus around global trade and capital flows, elevated inflation and policy rates, fiscal expansion and debt accumulation, and higher geopolitical risk. The current energy-supply shock is both a symptom and driver of today’s macro fragmentation, adding structurally higher prices and dispersion across markets (between those energy-exposed regions which will suffer from the disruption in the Strait of Hormuz, and those exporters benefitting from higher energy prices).

Investors will now have to take many of these features into account when building defensive portfolios, none more so than higher inflation levels. A simple split between bonds and equities will not protect investors through all the different inflationary regimes to come in this new era of investing.

Instead, investors will want to consider:

- Looking across a broadened asset class universe, incorporating real assets and inflation-linked bonds which can hedge against inflation.

- The specific levels of their exposures, ensuring that there remains a steady buffer against inflation balanced with the risks they are willing to take on.

- Managing exposures more dynamically to suit a particular macro environment, reducing allocations to duration, for instance, when inflation looks set to rise.

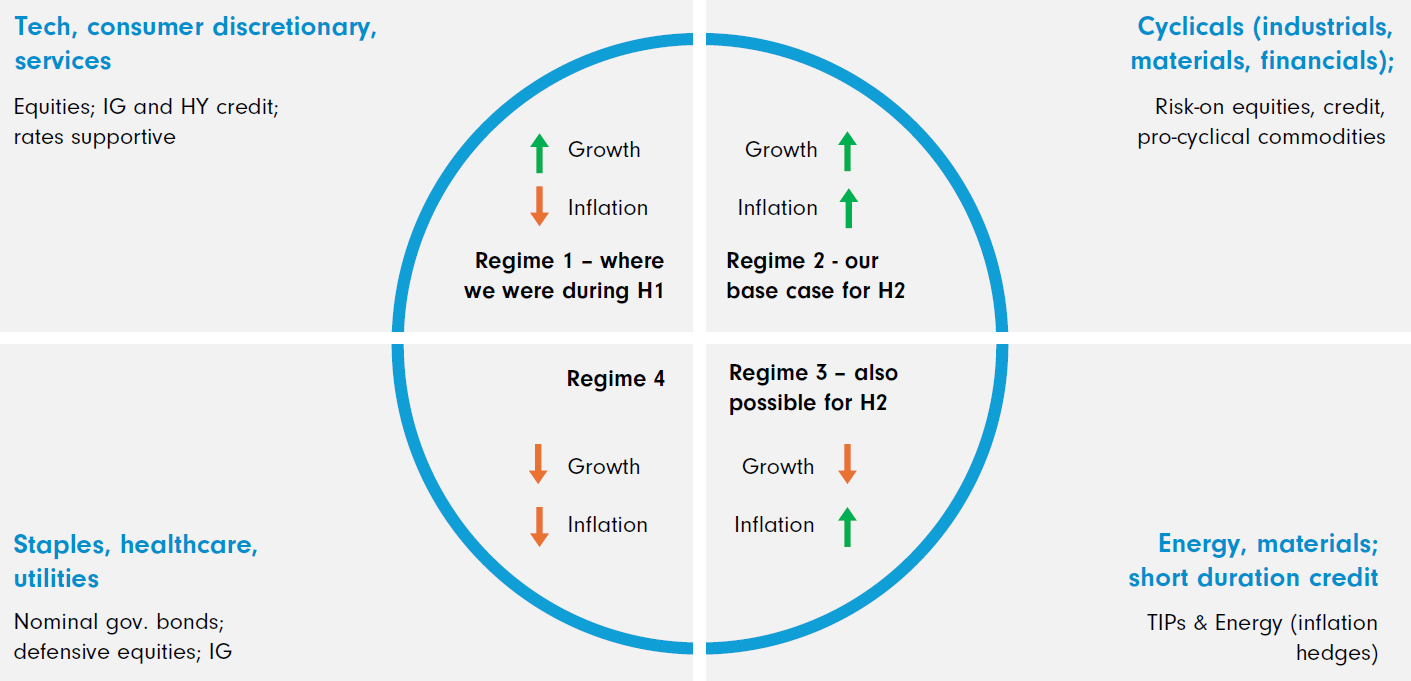

Defining inflation regimes

Inflation is a complex risk because it is variable. It offers no one ‘fix’. Instead, determining how to shelter portfolios relies on first establishing the particular inflation regime you are in, as well as the one you might be heading into. These regimes will be defined by questions of whether inflation is rising or falling, is high or low, and whether it is anchored or unanchored (i.e., are policymakers likely to bring it under control).

Moreover, inflation alone only tells you half the story. High levels of growth can support assets even through a high inflation regime, but if you combine rising prices with falling levels of growth then you have the sort of ‘stagflationary’ environment that makes policymakers sweat. So, to understand how different asset classes perform in an inflationary environment, we need to incorporate the growth picture.

Source: Fidelity International

The regimes outlined in the graphic above suggest broad patterns to inform allocation decisions based on the inflation trajectory. For instance, equities perform well when inflation is falling and growth rising, while nominal government bonds do well when growth and inflation are both falling.

But a more useful application is to start with individual assets, and match those against the regime you believe we are in. Past performance won’t tell you precisely how, for instance, emerging market hard currencies will perform through a particular regime. But it does suggest patterns of behaviour that can be useful for allocators constructing a portfolio to buffer against particular risks.

Our base case is that we are heading now into a more ‘reflationary’ regime, one in which growth and inflation are rising, driven today by policy support and strong fundamentals. This would be positive for stocks were growth to remain resilient. But there are risks that the macro environment fluctuates between regimes two and three over the medium term, as geopolitical and fragmentation challenges persist. Investors wishing to guard against these risks will both hedge against inflation and also manage their allocations dynamically when the macro environment changes.

How different regimes impact portfolios

The crucial variable that determines how inflation evolve is the room central banks must manoeuvre through a particular regime.

A high inflation regime renders central banks relatively impotent, since it diminishes policymakers’ capacity to combat inflation without affecting growth. It removes the central bank ‘put’. This environment is not conducive for risk assets, since inflation is eroding their value while the monetary environment is also less supportive.

On the other hand, real assets, like commodities, typically perform well in these environments.

“Exposure to commodities has historically helped protect investors through inflationary environments since these are real assets tied to rising input costs, and because of their lower correlations with other assets”, says James Richards, a Fidelity fund manager with a close eye on transition materials. “For investors concerned about concentration in consensus trades, such as AI capital expenditure (capex) winners, commodities introduce differentiated return drivers, enhancing portfolio diversification.”

Government bond performance, meanwhile, will vary according to the strength of the central bank put. Returns on certain government bonds have been strong through high inflation regimes, which appears counter-intuitive given expectations of rising inflation usually drive yields higher and bond prices lower.

But duration performance has depended on the specific type of inflation. Central bank targeting means inflation usually reverts to the mean, bringing bond yields down at the same time. In those instances, high inflation periods have often been followed by strong duration returns. So, if inflation appears mean‑reverting - typically because markets believe central banks can tighten appropriately - high inflation may precede favourable outcomes for duration.

But when inflation is persistent, it is more challenging. The near‑term outlook of structurally higher inflation, driven by global fragmentation and instability, suggests we are closer to the latter scenario.

There’s also potential in shorter-duration fixed income, which is less exposed to changes in interest rates, to offer stability for portfolios through its ‘carry’ - the steady income generated from holding a bond.

James Durance, a fixed income fund manager who focuses on short duration strategies, explains: “One of the key changes since 2022 is that fixed income once again offers meaningful income potential. In a structurally higher inflation environment, that carry can play a more important role in helping investors absorb market volatility and maintain real return potential over time.

“Within short duration credit markets, we continue to see opportunities to generate attractive income while maintaining a relatively defensive interest rate profile compared with longer-duration fixed income.”

Inflation-linked bonds, meanwhile, can be useful for portfolios if you expect inflation to rise.

“With inflation set to remain above central bank targets and expectations likely to prove sticky, traditional fixed income is at risk of leaving investors exposed,” says Ravin Seeneevassen, another fixed income fund manager.

“Inflation-linked bonds help close that gap by directly linking returns to realised inflation, providing a source of income that preserves purchasing power. Not only do inflation-linked bonds protect a fixed income allocation from erosion, but they also act as a superior diversifier to nominal bonds in a broader portfolio, exhibiting lower correlation to equities through the cycle.”

It will be useful to hold a baseline of these assets. Even if inflation at any moment looks relatively low, we live today in an environment of greater instability, in which prices may move suddenly. As the chart below shows, inflation historically has taken investors by surprise. It makes sense to hedge against that surprise before it arrives.

The new 60/40

The traditional 60/40 portfolio was well suited to a world of stable inflation and deepening global integration, but it may struggle to achieve similar outcomes in a more fragmented and uncertain environment, where inflation is less predictable and equity-bond correlations remain high. This new world invites investors to look beyond traditional equities and bonds to a broader range of asset classes and adopt a more dynamic approach to portfolio management. From there it is up to investors to decide how to implement these principles in line with their own objectives, risk tolerance, and views on the key risks ahead.

Whatever these might be, the direction of travel is clear: portfolio resilience is likely to require a wider toolkit than the traditional 60/40 allocation alone.