Emerging market (EM) equities moved back into focus in 2025, marking their first year of outperformance versus developed markets (DM) and the US since 20171, fuelled by factors including rising caution around the idea of US exceptionalism, interest-rate cuts from the US Federal Reserve (Fed) and the tailwind from artificial intelligence (AI)-related demand. In this perspective, we explore some of the reasons we think EMs can continue to outperform, and why the backdrop for the asset class remains compelling in 2026.

Key takeaways:

- An opportune moment for EM: Attractive valuations, greater fiscal headroom vs. DM, scope for rate cuts, and a constructive outlook for AI-driven demand and certain commodities make it a compelling time to invest in EM equities.

- Benefits of an active approach: Wide dispersion in returns, valuations and corporate governance standards across EM creates a strong case for taking a selective approach to the market.

- Valuations remain attractive despite relative outperformance over 2025

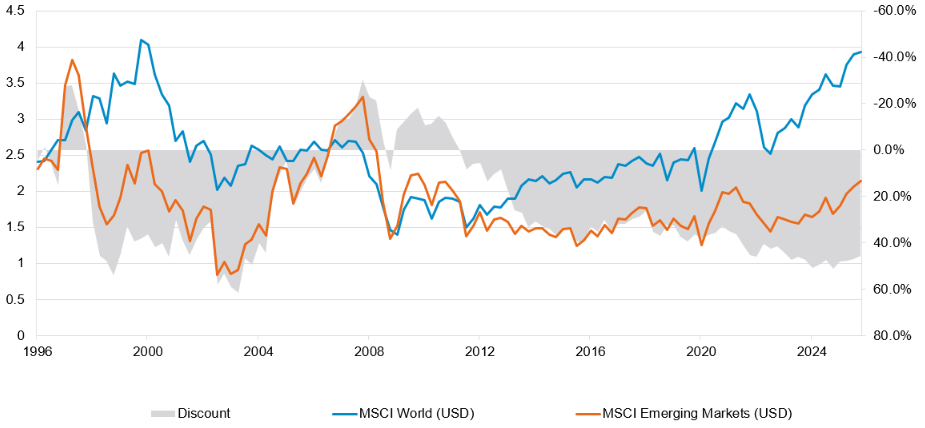

EM was among the best performing equity market in 2025, outperforming the US for the first time since 2017. Because of that, it’s easy to forget that the market continues to trade at a deep discount to the US and the rest of the world (see 'EM trades at a ~40% discount versus the rest of the world' above). Up until the end of 2024, weakness in China, and an environment of structurally higher interest rates and a strong USD had driven a de-rating in the market, leading to several decades of underperformance vs DMs.

However, 2025 saw several of these factors beginning to shift, with a weaker US dollar, falling interest rates, momentum in certain key commodities such as copper and gold, and signs of recovery in parts of the Chinese market supporting the asset class. Also supportive was the presence of a growing base of investors starting to look beyond the US for alternatives. And with the asset class still trading at a ~40% discount versus the rest of the world, there could be scope for continued re-rating in the market this year.

EM trades at a ~40% discount versus the rest of the world

Source: Fidelity International, Bloomberg, 31 December 2025.

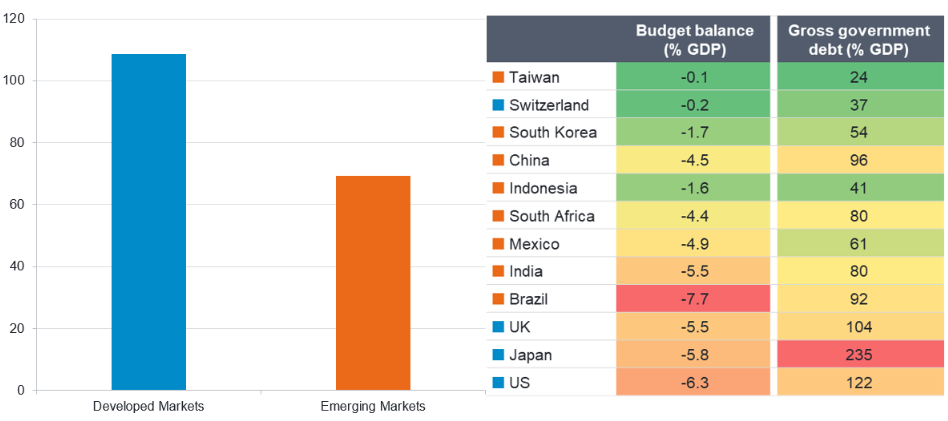

A robust fiscal and monetary policy backdrop

There are also several fundamental reasons why EM looks particularly well-placed as we move into 2026. Firstly, the fiscal backdrop continues to look supportive across much of the universe relative to the developed world. This in part reflects a hangover from Covid-19, when many DMs handed out fiscal stimulus packages to support the consumer, whilst we saw the opposite in many EMs, especially China, which tightened its belt and sought to deflate the property market. As a result, the fiscal backdrop looks much healthier for many EMs, with the exception of notable outliers like Brazil, leaving much of the asset class looking more resilient versus history. Whilst many DMs are less well-placed to carry out targeted fiscal support, greater fiscal headroom in most EMs also provides scope to shift towards expansionary fiscal policy where required, which could help cushion any downside risks to growth.

The fiscal backdrop looks superior in EM vs. DM

Source: LHS: Fidelity International, LSEG Datastream, IMF Fiscal Monitor, as of October 2024. RHS: JP Morgan, 2026 Outlook, Emerging Markets Equity Strategy, 2 December 2025.

In addition, the fiscal backdrop in the US has weighed on sentiment towards assets such as the US dollar, putting downward pressure on the currency, which pulled back significantly in 2025. Should the US dollar continue to weaken or even remain flat, this would prove supportive for EM, given a weaker dollar reduces debt servicing costs and imported inflation for EM and supports commodity prices, boosting local currencies and strengthening consumer purchasing power. However, it is worth noting that although US dollar weakness remains a tailwind for the asset class, it is not the only driver for EM outperformance. Many EM economies benefit from increasingly sophisticated capital markets and therefore carry less dollar-denominated debt than in the past, meaning EM outperformance is not reliant on continued US dollar weakness.

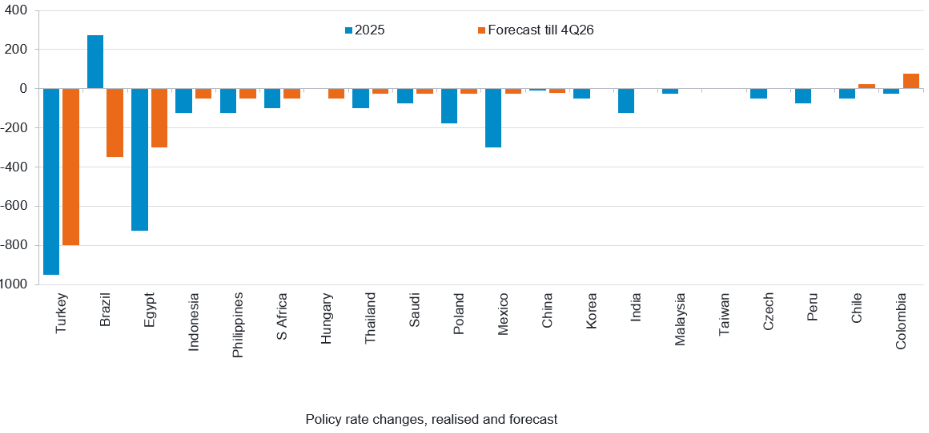

Finally, the monetary policy backdrop also looks supportive for much of the region. Many EMs raised rates early in 2021-22 to combat inflation, and real rates remain high, most notably in Brazil, but also in several EMEA markets too. As a result, many of these EMs have a long runway to further ease policy should the Fed continue to cut rates, which should create a supportive environment for equity valuations.

There is scope for rate cuts across many EMs in 2026

Source: Bloomberg Finance L.P., JP Morgan forecasts, as of 8 January 2025.

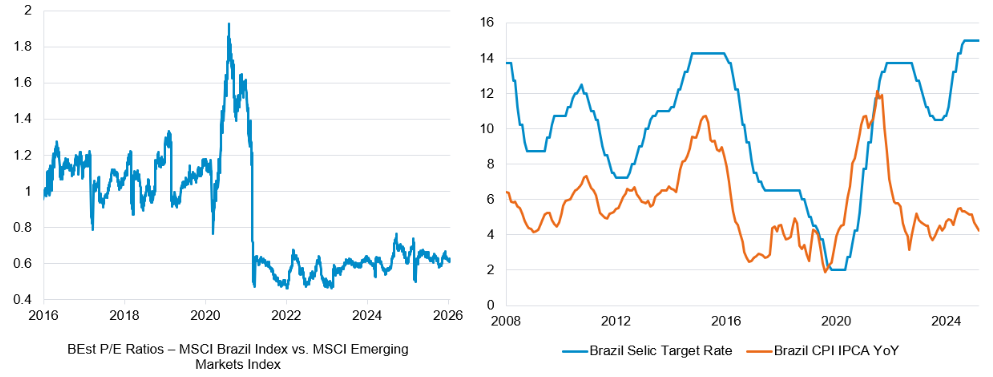

Brazil represents a particular area of opportunity with regards to rate cuts. The market remains cheap versus history and the rest of the EM asset class, in part driven by a deteriorating fiscal backdrop under President Lula, which has prompted the central bank to keep interest rates high (with real rates in double digits) to protect the currency. However, presidential elections in October signal potential light at the end of the tunnel, while a moderating inflation backdrop means the market is already anticipating a significant easing cycle this year. Although the election outcome remains uncertain, the risk-reward appears compelling, given the market already trades at a depressed multiple vs history, suggesting limited de-rating potential in the event of a continuation of the status quo, but significant upside should there be a market-friendly outcome.

Brazil is trading at a record discount (LHS), but an easing cycle could trigger re-rating (RHS)

Source: LHS: Bloomberg BEst estimates, as of 14 January 2025. RHS: Bloomberg, as of 31 December 2025.

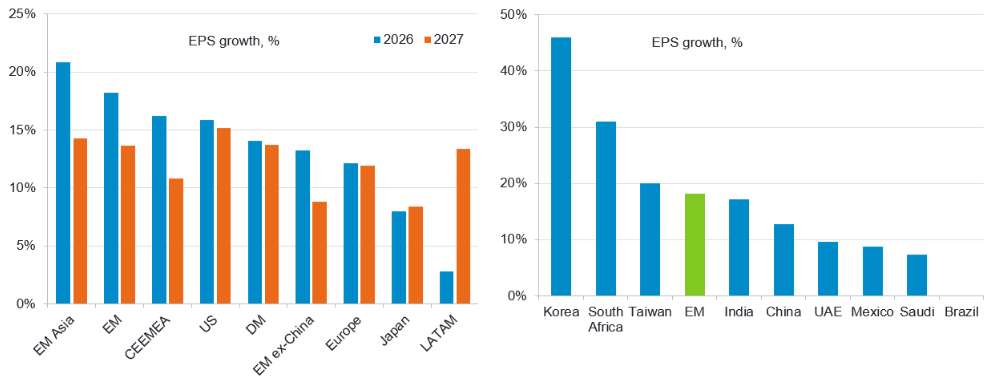

Strong earnings growth forecasts driven by tech and commodity-centric markets

The earnings growth outlook also looks positive for EM. Consensus estimates expect EM earnings growth to accelerate to 18.2% in 2026, a notable premium versus DMs and the US, which looks especially attractive considering EM’s valuation discount. Although the drivers of these earnings estimates are broad-based, as the country breakdown below shows, a key contributor is tech heavy markets such as Taiwan and Korea, and commodity-driven economies such as South Africa.

Better earnings growth forecasts vs. DM

Source: JP Morgan, IBES estimates, as of 8 January 2025

EM: The heart of the AI supply chain

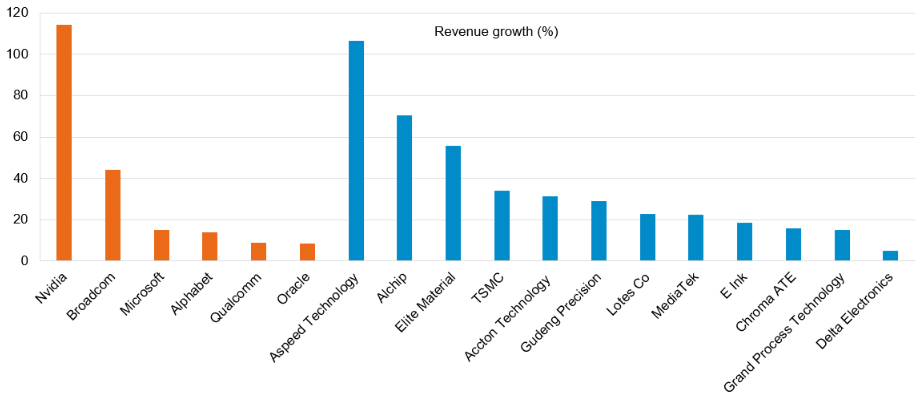

Another factor driving US markets higher in recent years has, of course, been optimism around AI. What has been overlooked, however, is the fact that the majority of the AI supply chain is located in EM markets like Taiwan, and to a lesser extent Korea. Nvidia, for example, has been explicit that it would not be the company it is today without Taiwanese semiconductor foundry TSMC, on which it relies on for the production of its GPUs, while Korea is home to two of the world’s three largest producers of memory (Samsung Electronics and SK Hynix), a type of hardware vital for AI chips and datacentres, that is seeing a strong supply/demand backdrop. It is likely that much of the of value accrual from AI and datacentres will go to EM companies, and we see significant opportunity to gain exposure to these tech companies vital to the AI supply chain, that often offer superior revenue growth to many US tech companies at much cheaper multiples.

Many Taiwanese companies offer higher revenue growth but trade at cheaper multiples than US tech players

Source: Bloomberg, as at 15 September 2025.

One example of this phenomenon is among manufacturers of ethernet switches, an input in datacentres, where Taiwanese business Accton competes with a US peer, Celestica. Whilst the two companies have near identical operating models, Accton has superior fundamentals and revenue growth, and a closer relationship with the end customer (TSMC), reflected in a deeper integration into its supply chain. Despite that, it trades at around half the multiple to Celestica – showing the value opportunities which are on offer in the EM tech space.

Commodity tailwinds

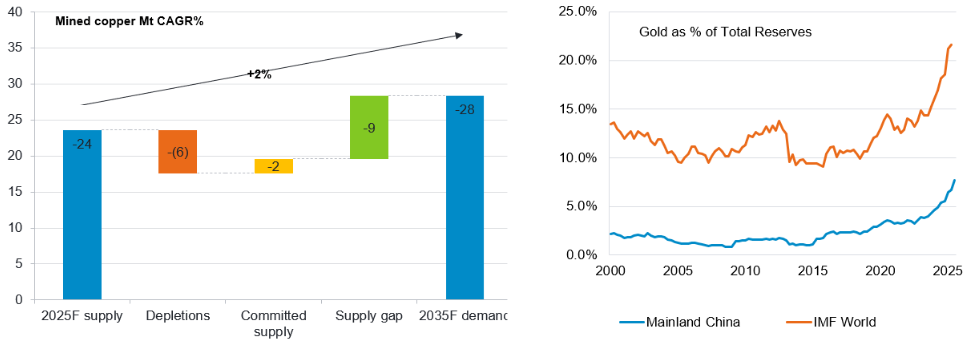

Another key driver for the EM asset class is the increasingly ‘goldilocks’ type backdrop for commodity prices, with what could be continued strength in key mined commodities such as copper and gold met with a muted backdrop for oil prices.

The backdrop for copper looks particularly favourable. Here, structurally stronger demand for the metal, driven by electric vehicle (EV)s, growing datacentre use and electrification, is coupled with falling supply, due to a lack of new greenfield projects and declining mine quality. For gold, whilst the market has moved a long way and price moves are much less easy to forecast than for a commodity like copper, it appears that many of the positive drivers for the precious metal remain intact, given the continued tailwind from central banks looking to diversify away from US Treasuries, with gold remaining a low proportion of total reserves in markets like China.

The supply-demand backdrop for copper looks positive (LHS), whilst potential for gold to increase further as a percentage of total reserves may continue to support gold prices (RHS)

Source: LHS: Rio Tinto Capital Markets Day, 4 December 2025. RHS: Fidelity International, Respective Central Banks, World Gold Council, as of 30 September 2025.

Strength in precious and industrial metals is positive for the terms of trade of commodity-exporting EMs, while miners make up a large proportion of equity markets like Peru and Chile (copper) and South Africa (gold). There should also be a positive knock-on effect for consumers in these markets, given miners are typically larger employers. At the same time, the bearish outlook for oil, underpinned by OPEC (Organization of the Petroleum Exporting Countries) excess capacity and supply growth from markets like Brazil, should be a further boost for the asset class, supporting the broad EM consumer via lower energy costs, given oil makes up a large proportion of the consumer-price basket in EM economies.

Bright spots in China: industrial innovators

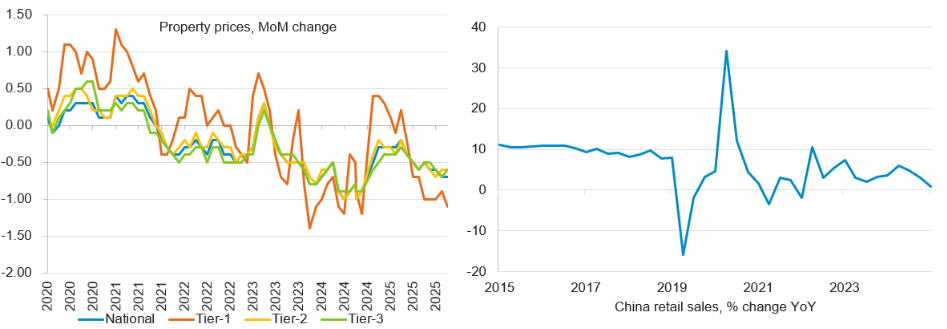

Finally, China warrants separate consideration given its considerable weight in the EM index. Here, the backdrop is complex, with the outlook for the consumer remaining challenged. Although we have seen the government shift towards expansionary policy, with rate cuts and targeted consumer stimulus packages aiming to support consumption, stimulus such as last year’s trade-in subsidies are now coming to an end, and the property market remains weak. House price growth continues to be in negative territory, and whilst excessive inventory levels within the market have stabilised, they have not yet fallen. Given that historically ~60% of household wealth in China has been tied up in the property market, it seems unlikely we will see a consumer recovery until the property market recovers.

Property prices are still in negative territory (LHS), underpinning weak consumer confidence (RHS)

Source: LHS: National Statistics Bureau, Fidelity International, 30 November 2025. RHS: Bloomberg, 19 January 2026.

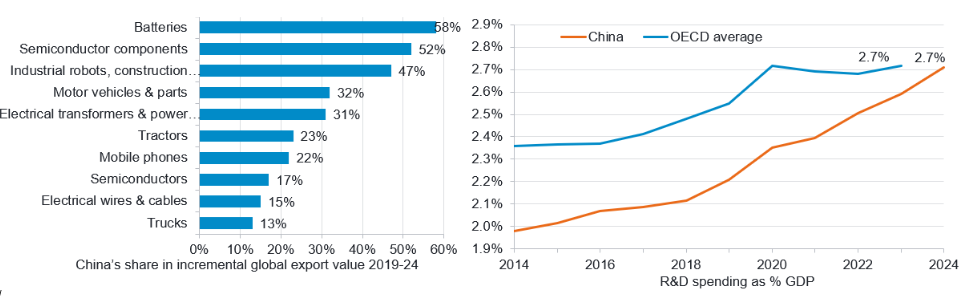

However, there are some bright spots in the market, particularly within several emerging industrial sectors, where we are seeing rapid innovation among Chinese companies. There are several key areas where China is moving up the value chain, including some of the world’s emerging and fastest growing export segments, such as batteries, semi components, and robots. Here, growing levels of Research & Development (R&D) spend, combined with a large, skilled talent pool - with China having the world’s highest proportion of tertiary graduates in a STEM (Science, Technology, Engineering, and Mathematics) field2 - are driving innovation and market share gains.

China is gaining share in fast-growing export segments, backed by R&D spending

Source: LHS: WITS, Morgan Stanley Research. January 2026. RHS: CEIC, OECD, Morgan Stanley Research, January 2026.

An opportune moment for EM equities

There are a confluence of factors making EM a particularly attractive asset class today. The valuation backdrop remains supportive, with potential for further re-rating in 2026 despite the rally in 2025. Similarly, the fundamental outlook looks attractive, supported by a superior fiscal backdrop, the potential for further rate cuts, and strong earnings growth potential across the region, underpinned by structural growth in tech, a constructive outlook for key commodities, and innovation in China.

Re-rating could also be supported by flows as investors increasingly look to diversify away from the US. Last year was the first of positive flows for EM equities since 2021, marking a notable turning point in investor sentiment towards the region. However, data from JP Morgan indicates these flows were entirely into passive products, and any uptick in flows into active funds – something JP Morgan argues typically occurs as the bull run matures and investors become cognisant of concentration risk and market rotation – could provide additional support to the asset class against a backdrop of depressed valuations and relatively light positioning3.

The dispersion on offer within EM also creates a particularly constructive environment for stock picking. We have seen a huge bifurcation in valuations at the country level, with the cheapest markets such as South Africa, Brazil and Mexico de-rating, whilst the most expensive, including India and Taiwan, have become more expensive. This offers considerable valuation opportunities among the broader index. Significant divergence in country-level returns, uneven corporate governance standards, and heightened sensitivity to headlines also mean there are plenty of segments of the market to avoid, pointing to the need for selectivity. As a result, we believe EM equities offer significant opportunity for investors willing to take an active approach to the market.

Sources:

1: Emerging Markets Equity Strategy, December and CY 2025 wrap, JP Morgan, 2 January 2026.

2: CEIC, OECD, Morgan Stanley Research, January 2026.

3: J.P. Morgan, Emerging Market Equity Strategy, EPFR Global, Bloomberg Finance L.P.