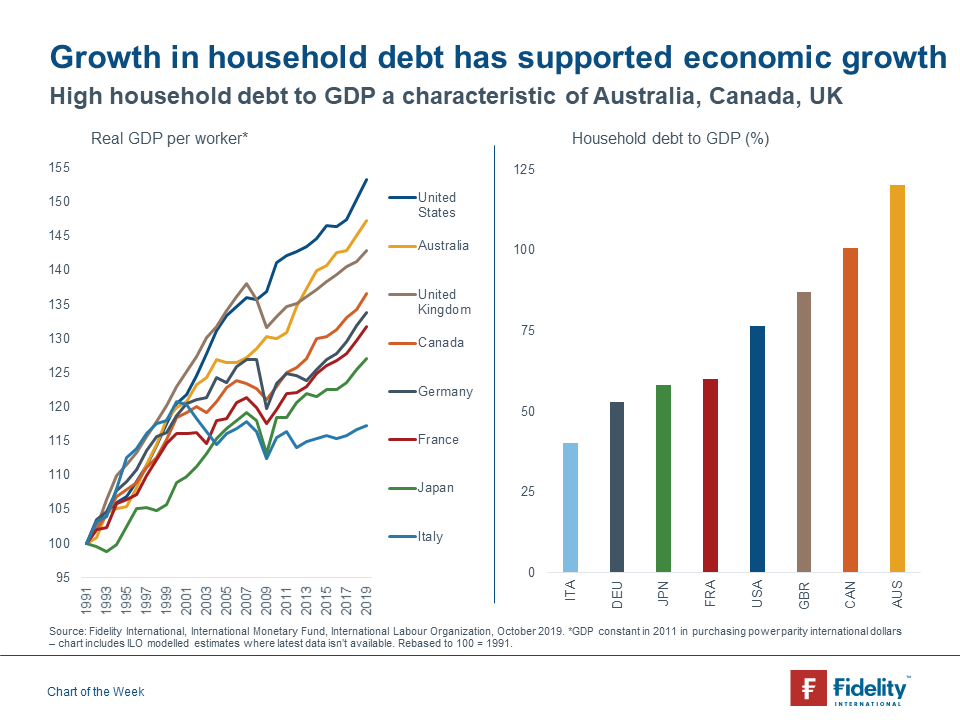

The Australian economy has famously avoided a recession since 1991. The economy’s performance has been remarkable - not only has Australia experienced a record run of economic growth, but on a Gross Domestic Product (GDP) per worker basis, Australia’s rate of economic growth has been higher than most of the major advanced economies including the UK, Canada, and Germany. Within the global economy, Australia punches well above its weight.

There is another economic statistic that Australia is associated with - household debt. The Australian economy has the second-highest level of household debt to GDP in the world, second only to Switzerland. Looking at the performance of the major advanced economies and their current levels of household debt to GDP suggests that there is a link between the two. This makes sense for a consumption and services-led economy like Australia, as households take on more debt to buy things like new homes and cars. Debt enables households to bring forward their consumption and investment plans, meaning economic growth is higher today than it would have been if households were forced to save to consume at some point in the future.

Whilst debt allows households to enjoy future consumption today, it must be repaid - with interest. And if households begin to cut back on spending to repay their loans, this will act as a drag on economic growth. This is currently the greatest danger to Australia’s uninterrupted run of economic growth, with consumer confidence, retail sales and wages growth currently lacklustre. Australian households have the capacity to relax their balance sheets and spend, but are currently wary following three interest rate cuts to a record low of just 0.75% from the Reserve Bank of Australia (RBA). In this type of environment, actions speak louder than words, and the RBA should consider whether a future rate cut could do more harm than good given the negative effect of low-interest rates on the income and confidence of savers.