Key points

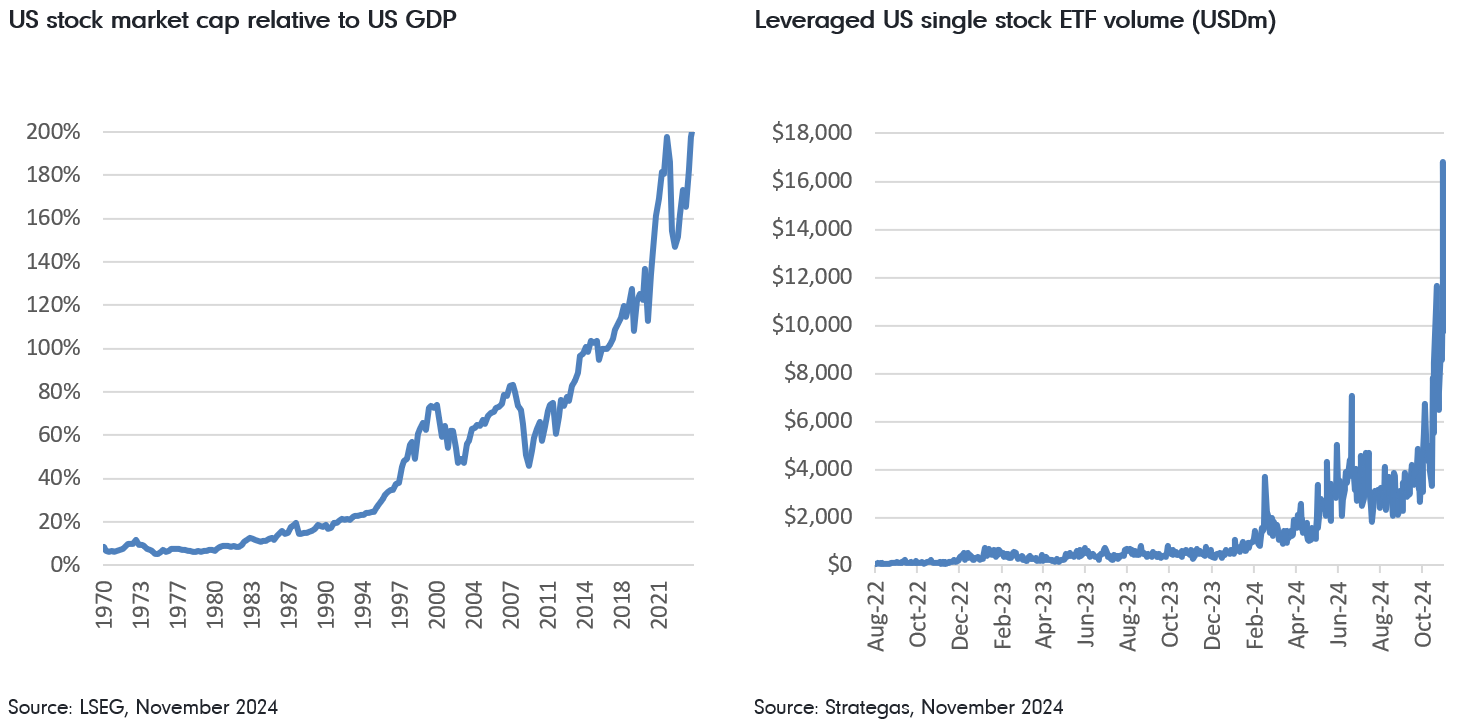

- Significant parts of the US equity market are in bubble territory; the scale far exceeds anything we have seen since I started in 2006. It is also arguably a lot bigger than the dot.com bubble of 1998-1999.

- The bullish market narrative has been driven by lower US interest rates, the artificial intelligence (AI) craze and more recently the ‘Trump trade’. In our view this Wall Street optimism is at odds with both the ‘main street’ reality and basic common sense.

- Our portfolio remains, on a bottom-up basis, overweight mid cap contrarian special situation stocks in Europe and China, and heavily underweight / short the US. Most of my long positions offer 15-20%+ annual free cash flow yield on normalised recovery numbers. A lot of them, particularly in China, have been aggressively returning capital to shareholders.

What is your outlook for your asset class?

The US part of the global universe looks very extended, both in absolute terms as well as relative to the rest of the world. This has been driven by the narrative around falling inflation as well as lower interest rates, the AI ‘theme’ and, more recently, the post-election ‘Trump trade’.

The decline of fundamental institutional participation and rise of passive flows, along with retail participation with extensive use of derivatives, has made the market far more vulnerable to periods of irrationality, as well as crowding into ‘hot’ themes. Many active managers are becoming forced buyers of the current index heavyweights, to manage benchmark risk. All of which means a highly distorted market environment in US equity.

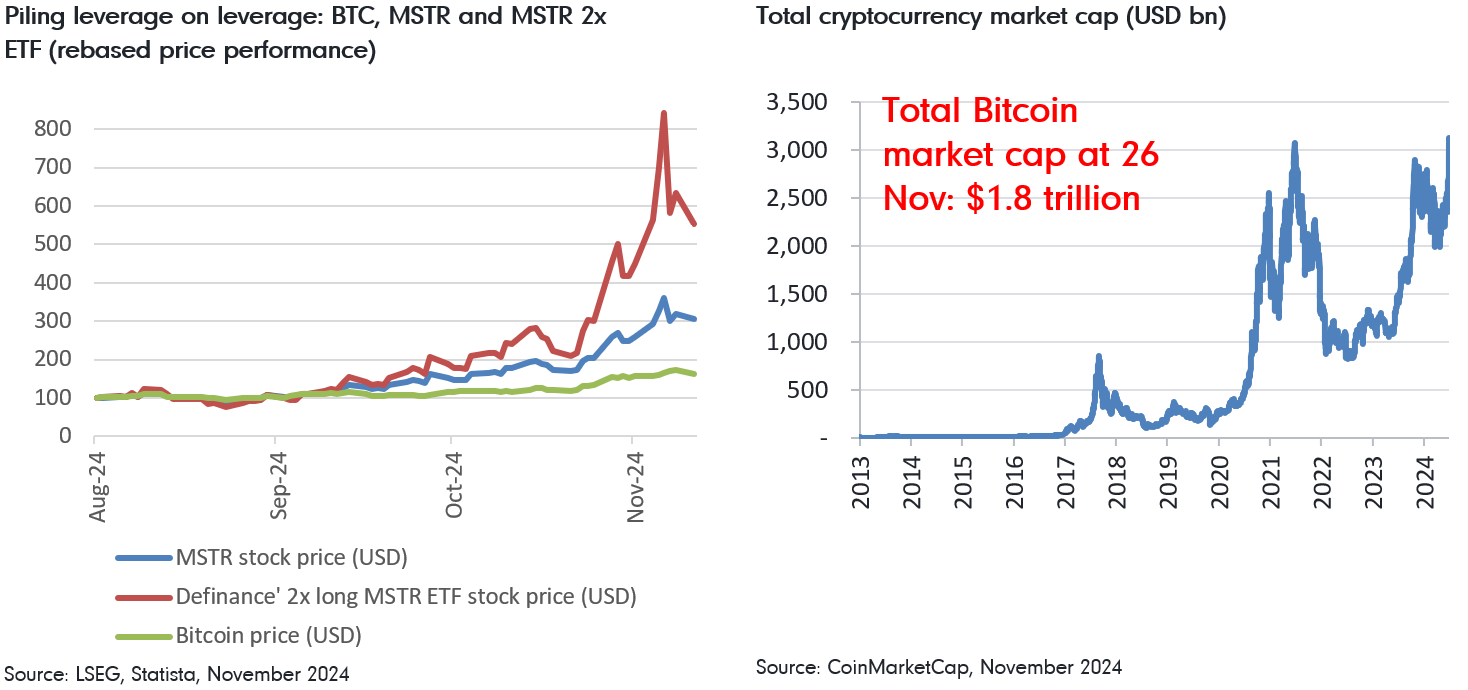

Certain asset classes have become highly speculative. For example, even if one argues that bitcoin can be viewed as a store of value (we disagree), it is still impossible to rationally explain such market phenomena as MicroStrategy stock as a levered play on bitcoin, and single stock double leverage ETFs as a levered play on MicroStrategy stock. Is it also very difficult to explain how other crypto coins can have combined value of hundreds of billions of dollars. These include such meme coins as Pepe the Frog, Shiba Inu as well as DOGE, to name just a few.

Just like in 2020, SPAC listings are back. Most of the 2020-21 SPAC vintages in the areas of renewable energy, electric vehicles, hydrogen, etc. have lost close to 100 percent of their market value. We now have new thematic SPACs around nuclear and space exploration. Most of these names will also end up being zeroes from the equity point of view. Whilst AI is certainly real, most of the investment that has gone into it won’t earn any meaningful returns and will end up being a write off. We expect the AI capex bubble to burst in 2025.

Finally, while the new US administration has growth orientated policies, we need to be mindful of the enormous US fiscal deficit. Some spending cuts may be possible, though this is unlikely to be positive for short term economic growth.

The broader US economy remains highly bifurcated. High-end consumers continue to do well, given the wealth effect from asset price gains. But low and mid end consumers are still struggling from the level of prices, if not the rate of change (though even this is again starting to creep up). Outside of the largest caps, profits are falling sharply, with weak readings from small company surveys and rising levels of consumer debt, auto loan delinquencies and credit card balances.

How are you looking to position your portfolio against this backdrop?

We expect highly speculative areas of the US market mentioned above to burst. Our short book is heavily exposed to US tech names, including AI plays and SPACs. Over US$200bn has already been invested in building out AI infrastructure. Recent evidence suggests the propensity to pay for Gen-AI tools remains low, while Large Language Models (LLMs) are becoming increasingly commoditised and starting to compete on price. AI startup funding looks likely to have peaked, and could end 2024 roughly flat year-on-year. Having an LLM in the proof-of-concept stage is very different from implementing it in a real-life environment for real use cases. This means that AI adoption might take even longer and be a lot more expensive than many believe. All of this implies we may be getting towards the later stages of the current AI market mania.

Our long book remains heavily overweight Europe and China and underweight the US. Our China positions, via Hong Kong and US-listed names, are paying very good dividends and making hefty buybacks; we are being paid a good amount to wait for a rerating. Our European holdings are generally ‘proper’ special situation/turnarounds; midcaps in ‘old economy’ areas which require significant restructuring and/or management changes to work. Most offer 15-20%+ annual free cash flow yield on normalised recovery numbers. The pessimism around some markets - notably Germany - is also presenting me with some interesting new contrarian ideas. We also continue to like opportunities in the energy services and energy transition space - be these traditional energy services, LNG, or nuclear.

When the current bubble bursts, we could see strong outperformance from one or more of these areas.