This article first appeared in Livewire Markets on 13 February 2023

Reputation may precede it but you could be doing yourself a disserve by avoiding emerging markets.

When you think of emerging markets, what comes to mind?

Perhaps you think volatility and uncertain political situations. Or perhaps you just think of China, the biggest of the emerging market countries?

However you think about it, it’s a far bigger market than you might expect. You could be doing yourself a disservice by ignoring such investments.

What are emerging markets?

Traditionally, investors used to talk about “BRICS”. This referred to Brazil, Russia, India, China and South Africa. Aside from the obvious concerns over Russia at present, this is a fairly restrictive definition.

Both Dr Joseph Lai, Chief Investment Officer at Ox Capital, and Amit Goel, Portfolio Manager at Fidelity Asset Management, use the MSCI Emerging Markets Index to form their definition and universe.

MSCI defines emerging markets compared to developed markets based on position in three spaces: economic development (based on World Bank’s gross national income per capita), size and liquidity of its equity market, and accessibility for foreign investors. These are countries in the active process of becoming developed countries.

The countries currently included in the MSCI Emerging Markets Index includes Brazil, China, Chile, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, United Arab Emirates.

It’s quite an extensive list, and arguably, many of the countries included have vastly different political systems, economic drivers and systems.

“Emerging markets are home to geographies as diverse as a high-income Korea to a low-income Indonesia, from large domestic economies such as China, to an export-dependent Taiwan and from commodity exporters such as Saudi Arabia to importers such as India,” says Goel.

MSCI also ranks countries that are less ‘advanced’ in their progress to becoming developed nations as frontier markets. These are countries that may not have developed or accessible stock markets such as Croatia, Kenya or Vietnam.

Risky business…

One of the biggest detractors of investing in emerging markets is the view that they are volatile, poorly managed and heavily indebted.

Lai points out that while this is true of some (often as not from the frontier market category), it’s not universal.

“As a sign of their strong fundamentals, most emerging market countries are not suffering from huge inflationary pressures and their currencies have been resilient in the face of a strong US dollar,” he says.

Goel similarly adds that many improved their financial balance sheets in recent years and have been proactive about managing inflation.

“These countries are used to high inflation levels and there are robust mechanisms of inflation transmission into wages and other contracts, which prevent a standard of living crisis that we are seeing in some developed countries,” says Goel.

It’s also fair to say volatility is a problem for investors regardless of whether you invest in a developed economy or an emerging one. Lai argues that quality and diversification are critical in an investor’s toolkit for managing volatility in any market.

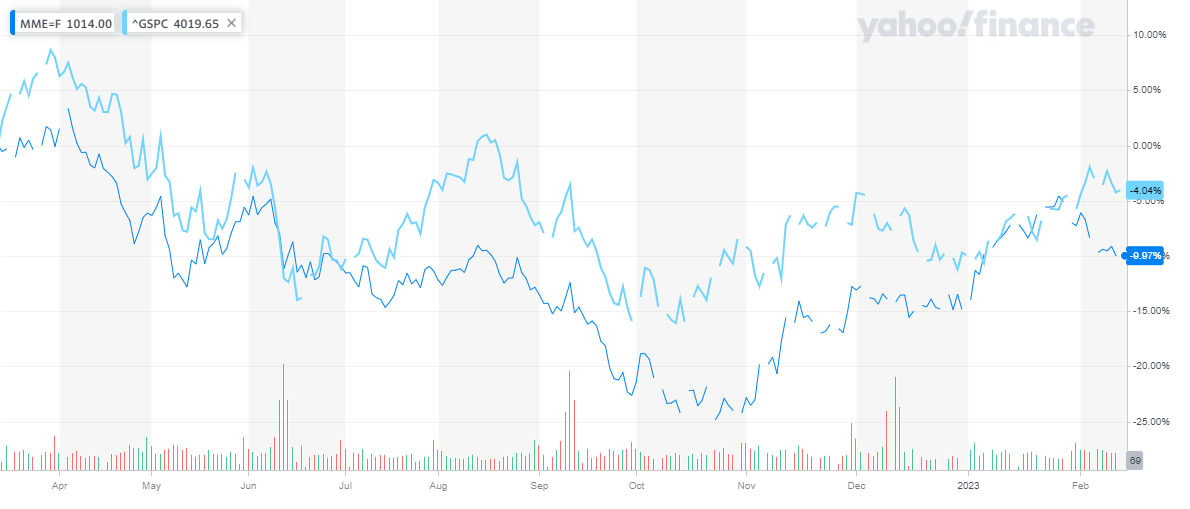

MSCI Emerging Markets Index v S&P 500

MSCI Emerging Markets Index (MME) v S&P500 (GSPC). Source: Yahoo!Finance

The untouchables

Investor concerns often extend beyond overall country volatility to a perception of a lack of “rule of law” in emerging market countries. That is, the view that you can’t rely on the rule of law to protect your assets and large businesses with government backing don’t have the interests of minority shareholders at their core.

Glen Finegan, Lead Portfolio Manager and Co-Managing Partner at Skerryvore Asset Management, notes that this can be a concern in certain countries but the key is careful stock selection and working closely with selected companies.

“Investing alongside managers and owners with good reputations that share a belief in a long-term approach to investment is an important way to align interests and to access emerging markets investment opportunities,” Finegan says.

The secret to investing in emerging markets

While investing in emerging markets may feel unfamiliar, exotic or intimidating, Goel, Lai and Finegan believe it is no different from investing in developed markets and comes down to solid stock selection of high-quality businesses. Each take a slightly different approach to their stock selection.

Goel looks for characteristics including high quality, sustainability, a competent management team and growth-at-a-reasonable-price.

“The rate of growth is typically higher than in a developed market and we can find good quality businesses in growing segments that meet our expected returns threshold of 10-15% CAGR,” Goel says.

While quality is also important to Lai, he looks for companies operating in under-appreciated industries at attractive valuations. He notes this often allows Ox Capital greater bargaining power on prices.

“For example, we were into energy, marquee Indonesian names and some Chinese domestic consumption-related businesses at extremely cheap prices over the last 12-18 months. We are confident these names will deliver great returns and become even greater businesses in the coming 3-5 years,” Lai says.

Finegan extends his search to companies that may be listed in developed markets but derive the bulk of their income from emerging market countries.

His process looks at good governance, track record, the strength of a company’s franchise and resilience in cycles, sustainability and financials. The companies Skerryvore invests in typically have a conservative approach to debt and risk.

Historical management and performance through crises is also a key measure.

“We believe the stress that crises put companies under is a good test of the quality of a business. These periods of stress allow us to see whether the business model is resilient, providing us with a clear view of the risks that the stewards of the business were taking at the time,” Finegan says.

Ways to access emerging market investments

Fund managers often take two approaches to exposure to emerging markets. These are not necessarily mutually exclusive – Finegan notes he uses both approaches in the Skerryvore portfolio.

Invest in companies domiciled in emerging markets countries. For example, Tencent Holdings (HKG: 0700).

Invest in companies domiciled in developed markets but generating the majority of their revenue from emerging market countries. For example, Heineken Holding NV (AMS: HEIO).

The first option can be more challenging for direct investors depending on the stock market access levels for foreigners. This is where using active fund managers or index funds accessing particular regions can be useful exposures for investors.

Finegan, Lai and Goel argue that stock selection is crucial when it comes to emerging markets, whether you do it yourself or via a manager. This may be something to be conscious of if considering a passive approach to these markets.

None of them recommend a top-down approach due to nuances of different countries.

A final tip to the wise with a quote from a country legend

Finegan believes you could do worse than listen to unexpected sage Dolly Parton.

“If you want the rainbow, you’ve got to put up with the rain.”

It applies equally to the cycles you see in investment markets and particularly for emerging markets. If you want the returns, you need to accept downturns are part and parcel of investing.

“We find investing in businesses with high levels of alignment, strong franchises and transparent financials offers the best chance of reaching your long-term investment goals,” says Finegan.

It applies regardless of market.