Top convictions for 2025

- Defensive US dollar investment grade - to shelter from recession risks.

- Global short duration income - to lock in decent all-in yields.

- Asian high yield - to capture attractive carry and spreads compression.

A dominant theme for fixed income markets in 2025 will be where US interest rates find themselves at the end of this rate cycle.

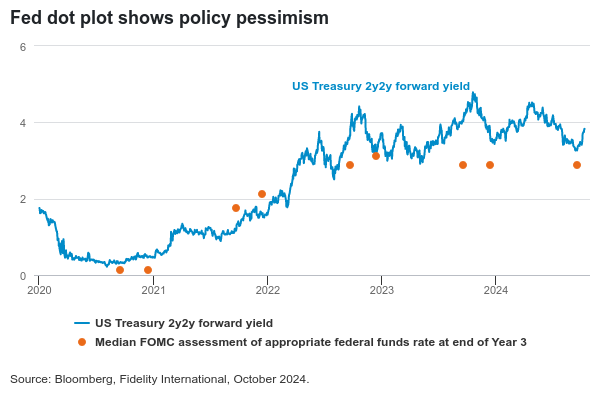

Investors’ estimates of where the terminal rate will trough have proven volatile. For example, when the US Federal Reserve (Fed) cut rates by 50 basis points (bps) in September to 5 per cent, surprising many who were expecting only 25 bps, the market’s assessment of the terminal rate went up rather than down. The logic was that by doing more to address growth risks sooner, the Fed wouldn’t need to reduce rates by as much overall.

As the chart shows, this put the market at odds with Fed policymakers’ more dovish outlook for rates over the next two years.

Source: Bloomberg, October 2024

Any new tariffs are likely to push inflation higher, making a case for the terminal rate ending up above what the market is pricing in at the time of writing (around 3.5 per cent), as does the expected increase in the US fiscal deficit next year.

There are, however, other forces in play.

US recession looks underpriced

Investors looking for value in fixed income should note that the market struggles to price things like geopolitical risks, which have clear potential to hurt economic growth.

The recent hiking cycle has also been unusually benign for credit issuers. Corporate net interest costs have actually gone down for those who locked in lower rates on their debt when yields were at multi-year lows and then benefitted from parking their cash balances in short-term deposits or money market funds, earning high interest rates.

Where issuers have felt pain, distressed exchanges have accounted for most defaults so far this year (54 per cent in the year to end-September1), lessening the impact on investors. But at some point, issuers who locked in lower rates will have to refinance, a fact that will weigh increasingly on investors’ and policymakers’ minds as 2025 progresses.

The US has also just had an election in which 68 per cent of voters told exit pollsters the economy is “Not so good/Poor”.2 Whatever economic indicators might imply, Americans clearly don’t feel well off.

If US growth does deteriorate over the next 12 months, the Fed may have to cut more aggressively than expected, meaning a lower terminal interest rate. With credit spreads currently tight, there is a risk-reward case for adding US duration with a bias towards holding higher quality credit.

China: waiting for more

A big focus heading into next year is the timing and extent of China’s stimulus measures, and their potential to boost growth domestically and across the wider region, but also to export inflation. As we wait for Beijing’s next move, and any response to US tariffs (if and when they happen), it’s worth considering the picture facing credit investors in 2025. For example:

- China’s property sector now makes up around 5 per cent of the JP Morgan Asia Credit Non-Investment Grade index, down from over 30 per cent at its peak. This is a stronger, more balanced index.

- The average rating of Asian high yield bonds is now BB, with rating upgrades likely to continue, particularly in frontier Asian economies and in the BB category, where some rising stars are emerging.

- Asian high yield spreads are attractive at over 500bps, above their 20-year average, leaving room for compression. With an average duration of just two years, they are also less sensitive to interest rate moves.

These factors create a favourable environment for Asian high yield credit, especially if we see continued Fed easing as well as more monetary easing and stimulus from China.

Investment grade Asian bonds also look good. The supply of Asian US dollar investment grade bonds has shrunk significantly, with issuers reluctant to borrow in dollars at high interest rates compared to local markets, while investor demand remains high. Expectations of a stronger dollar in 2025 would be unlikely to reverse this trend.

Monetary policy outlooks

The next 12 months should see a jump in fiscal spending from the US and China. Markets may have greeted this prospect with euphoria, but it’s a sign that all is not well with the underlying growth picture – one that is further threatened by increasing geopolitical tensions.

To address these concerns, we expect the Fed will want to be the most proactive about bringing rates down to a neutral level. This was evident when it followed up its bumper September cut in November with a further 25bps, although it may yet be constrained by resurgent inflation.

There is a strong possibility of stagflation in the US, in which case the Fed might have to prioritise growth. The European Central Bank also has an eye on stickier wage and services inflation, although structural economic weaknesses in the Eurozone, particularly in Germany, make a case for being overweight duration here.

Further Fed cuts would free central banks in China, Korea, and Indonesia, for example, to go further in cutting their interest rates, supporting Asian bonds. Alternatively, a less dovish Fed policy would give the Bank of Japan more room to normalise policy following its first hike in 17 years in March 2024.

In practice, central banks will all have to run their own race. Keeping pace with each one will be part of the challenge for fixed income investors in 2025.

Read more articles from our 2025 Outlook